Submitted:

19 March 2024

Posted:

20 March 2024

You are already at the latest version

Abstract

External audit reliance issues on the internal audit function (IAF) are increasingly important in financial auditing, yet its application in audit engagements lags behind other applications. Despite the belief that audit reliance will shape auditing in the future, limited and intervalley publications explore this transformative potential. This paper investigates the increasing importance of external audit reliance issues in financial auditing. It investigates the use of the IAF in external audit reliance decisions and its potential to enhance audit quality, process transparency, and stakeholders' credibility. Through a systematic literature review of 68 scientific articles from 1984 to 2022, factors influencing external auditors' dependence on the IAF are analyzed, including IAF work quality, assistance type, organizational factors, customer pressure, and business risk. The review highlights the IAF's crucial role in improving financial reporting integrity and external audit effectiveness. However, the challenges that allowed external auditors to decide whether to rely on the works of IAF like limited disclosures and accessible data hinder assessing IAF reliance effects, leading to information asymmetry that may impact stakeholder confidence. The paper discusses implications, limitations, and future research directions to explore technology adoption and optimize audit practices, promoting transparency in the audit process.

Keywords:

external audit

; reliance decision

; internal audit function

; financial audits

; systematic literature review.

1. Introduction

Audits’ reliance has been debated for decades. The competence of the IAF is critical for stakeholders’ decision-making. Evaluating the efficiency of the IAF is necessary due to its consultative responsibility (Alzeban & Gwilliam, 2014). Internal auditing is vital for an institution’s accounting system and protects against hazards. However, it hasn’t received as much attention in the literature as external audits and the audit committee (Christ et al., 2021). Whereas, external auditors (EAs) and internal auditors (IAs) share common interests and can mutually benefit from effective cooperation (Brody, 2012; Morrill & Morrill, 2003; Suwaidan & Qasim, 2010). EAs can enhance their efficiency by utilizing the work of IAs, reducing the extent of their audit tasks. A competent and objective IAF can significantly contribute to an efficient external audit process (Al-Twaijry et al., 2004).

Cooperation between EAs and IAs is a double-edged sword. EAs can enhance efficiency by using IAs’ work, reducing redundancy and costs (Morrill & Morrill, 2003; Suwaidan and Qasim, 2010; Chen et al., 2017). However, if IAs are deemed unprofessional and lacking independence by EAs (Al-Twaijry et al., 2004), it hinders cooperation and risks external audit quality. EAs must balance the pressure to cooperate with the IAF while fulfilling their core purpose of providing accurate and timely information to stakeholders and society (Duska, 2005; Tagesson & Eriksson, 2011). The external auditor’s reliance on internal auditors has received increased attention (Desai et al., 2017; Pike et al., 2016). Collaboration opportunities have grown due to the involvement of internal audits (Mihret, 2014). Relying on internal auditors’ work has financial and performance implications for external audits (Pizzini et al., 2015).

External auditors can rely on internal auditors’ work as per ISA 610, reducing duplication. Factors like competency, independence, and due care impact the quality of internal audit work (ISA 610; SAS No. 65). IAFs’ shift towards advisory services enhances their importance in corporate governance (Chen et al. 2017; Soh & Martinov-Bennie, 2015; Speklé et al., 2007; Ismael & Roberts, 2018).

While recognizing the existing gaps and limitations in the literature regarding the external auditor reliance decision. On one hand, there is recognition of the empirical dilemma, suggesting that there is an existing issue or challenge (Swanger & Chewning, 2001), further research is needed to explore the extent to which External Auditors (EAs) rely on Internal Auditors (IAs) (Desai et al., 2017). Additionally, there is a lack of publications regarding the external auditor reliance decision and its impact on external audit quality (Bame-Aldred et al., 2013, p. 253). This paper aims to address this gap by examining how EAs perceive their decision to rely on the work of IAs. The focus is specifically on the perspective of EAs, as this decision falls under their formal responsibility (ISA 610, 2013). By establishing a framework to investigate various aspects of external auditor reliance, this research contributes to the existing body of literature. Although previous literature reviews have been conducted, the uniqueness of this paper lies in its assessment of the knowledge base surrounding the external auditor reliance decision and its identification of potential areas for further investigation (Christ et al., 2021; Roussy & Perron, 2018).

To our knowledge, this is one of the first studies to adopt a Systematic Literature Review (SLR) approach, which encompasses a broad perspective and includes a wide variety of study outcomes. To address this knowledge gap, the current research utilizes the PRISMA approach for a systematic literature review (Page et al., 2021). The review aims to determine the external audit reliance issues, through a comprehensive analysis of existing research, we explore the factors influencing external auditors’ dependence on the IAF, including IAF work quality, assistance type, organizational factors, customer pressure, and business risk.

In conclusion, this SLR contributes to the existing body of literature by providing a comprehensive understanding of external audit reliance on the IAF and its effects on financial statement quality. The identified challenges and implications guide auditors, organizations, and stakeholders in optimizing audit practices and promoting transparency in the audit process. This research serves as a foundation for future studies, exploring technology adoption, regulatory changes, and the interplay of auditors’ perceptions and decision-making to advance knowledge and understanding in this field.

The remainder of this paper is organized as follows: the methodology section provides the detailed plan of SLR procedures, then the key involvements regarding the external auditor reliance issues with detailed analysis, and after that the summary of results. Finally, the conclusion provides an overview of our achievements and outlines future research directions.

2. Analysis and Literature Review Results

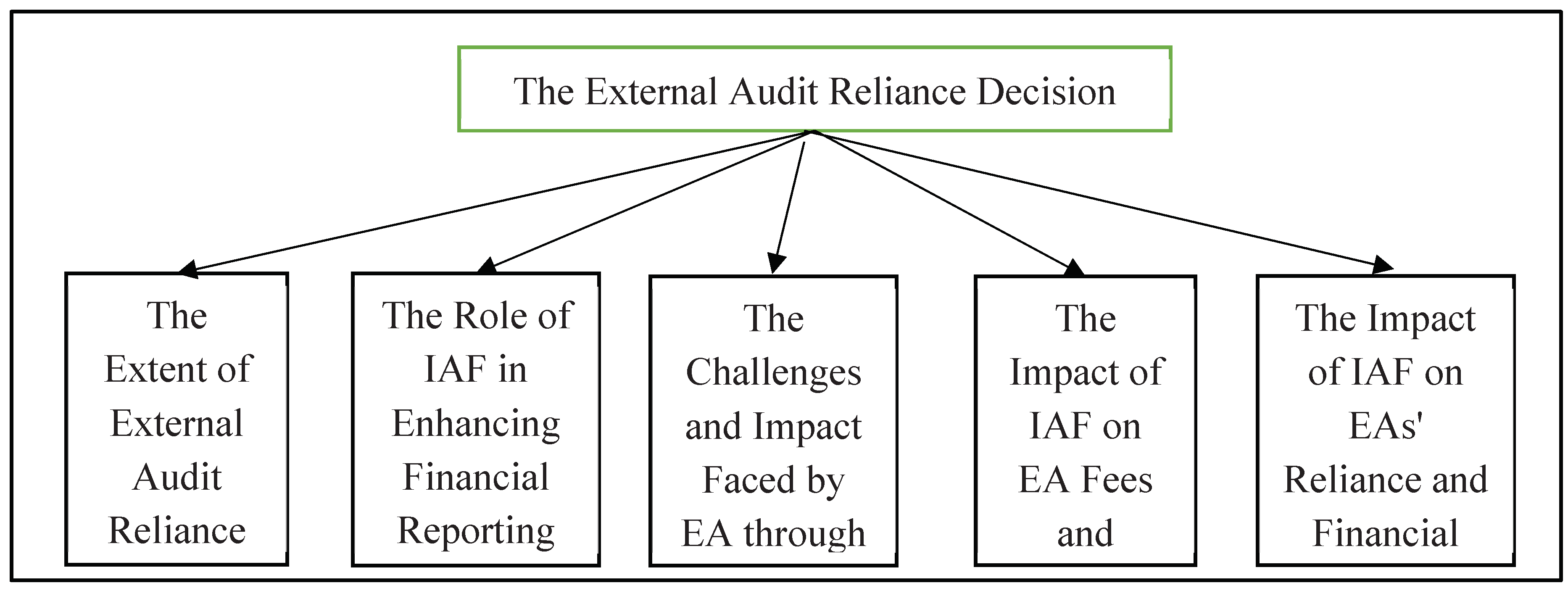

This paper’s focus is evolving the external audit reliance issues. Furthermore, five main audit reliance issues: the extent of external audit reliance, the role of IAF in enhancing financial reporting integrity and EA Effectiveness, the challenges and impact faced by EA through their reliance on IAF, the impact of IAF on EA fees and quality, and the impact of IAF on EAs’ reliance and financial statement quality, which represented in Figure 1 given framework, also key themes, gaps, and suggestion for future research which identified from the review were presented in Table 3.

2.1. External Audit Reliance Decision Issues

External auditors follow three standards—PCAOB, ASB, and IAASB—when relying on internal auditing. To address the internal audit task for public corporations, the PCAOB introduced AS 2605 (PCAOB, 2013). This research is anchored in ISA 610, which guides external auditors in utilizing the work of internal auditors for evidence collection and support (ISA, 610). The study investigates how external auditors enhance their performance by adopting the practices of internal auditors, aligning with ISA 315 and 610 in 2016. The presence of more internal auditors correlates with increased dedication to auditing financial statements, ultimately improving audit performance (Lee & Park, 2016). Additionally, we examine studies on the reliance of External Auditors (EAs) on IAFs, influencing variables such as litigation risk, audit efficiency, fees, financial statements, and internal control quality (Bame-Aldred et al., 2013).

2.1.1. The Extent of External Audit Reliance

In this section, we delve into the intricate dynamics of External Auditors’ (EAs) decision-making regarding their reliance on IAFs. This decision involves a nuanced assessment of the IAF’s work quality and their role, whether as evaluators or as assistants. Our examination begins by exploring the ramifications of customer pressure on the reliance on IAF, an aspect that has received limited attention in prior research (Gramling et al., 2004). Organizational factors such as board connections, business risks, and client demands emerge as influential determinants in shaping EAs’ utilization of IAFs. To tackle concerns about subpar IAF performance and low reliance, our analysis suggests that while automated remediation is partially effective, less frequent and more targeted remediation procedures prove superior to continuous strategies (Farkas and Hirsch, 2016).

Munro and Stewart (2011) contribute to this discourse by conducting an experimental study, investigating how business risk and reporting arrangements with the board impact EAs’ reliance on IAF work and their use of internal auditors. Reporting relationships and business risks surface as pivotal factors influencing these decisions. Abbott et al.’s (2007) survey of chief internal auditors further augments our understanding, focusing on audit committee effectiveness in determining independence and the nature of outsourced services. The study emphasizes the importance of efficient audit committees in monitoring internal audit activities to safeguard external auditors’ independence, aligning with previous research on effective governance and audit committee effectiveness.

The utilization of internal auditors’ work by external auditors introduces risks to their objectivity and professionalism, raising concerns about potential uncritical assessments (Argento et al., 2018). ISA510 and ISA620 provide different perspectives on auditors relying on third-party work, with ISA620 particularly valuable in convincing internal reviewers and regulators about the evidence for complex items (Kok & Maroun, 2021). The adoption of data analytics in external auditing emerges as a key theme influenced by factors such as the audit profession, technology, organization, quality control, and audit clients. Our analysis reveals that employing IT professionals, auditor skills, data storage, and quality controls significantly impact the use of data analytics in audit practice (Jacky & Sulaiman, 2022).

The regulatory landscape, especially since the Sarbanes–Oxley Act (2002), has elevated the significance of the internal audit role (Desai et al., 2011). However, the extent to which external auditors rely on the quality of internal audit tasks remains a subject of mixed and inconclusive results, necessitating further exploration (Bame-Aldred et al., 2013; Weisner & Sutton, 2015). Internal audit’s inverse impact on organizations’ willingness to consent to audit judgments about ongoing concerns introduces another layer of complexity (Dzikrullah et al., 2020).

Various aspects of internal auditing competence, work done, objectivity, and non-internal audit factors intricately influence the decision-making process of internal auditing reliance (Schneider, 2010). Desai et al. (2017) shed light on the measurement of power for external auditors, revealing their susceptibility to negative evidence and struggles with consistent integration of data on three variables in their overall assessment of strength. The study further explores how internal auditors’ involvement in non-audit functions impacts external auditors’ assessment and reliance on their performance. The supply of non-audit functions negatively impacts the credibility of externally hired internal auditors, while the use of multiple persons for consultancy services moderates impressions of impartiality but does not significantly affect competency perceptions (Brandon, 2010).

Our systematic literature review (SLR) provides a comprehensive understanding of the factors influencing EA’s dependence on IAF, considering both the quality of work and the nature of assistance provided. It underscores the intricate interplay of organizational factors, customer pressures, and business risks. Automated remediation’s limited impact prompts a nuanced exploration of remediation procedures. Insights into data analytics adoption and the evolving regulatory landscape contribute to the richness of our analysis. Despite advances, the literature highlights the need for continued exploration, particularly in understanding the complex relationship between external and internal auditors. This synthesis not only enriches the knowledge base for auditors and organizations but also serves as a guide for effective audit practices.

In this section, key themes in the realm of external audit reliance on IAF are explored. Factors influencing this reliance, such as customer pressure and organizational factors, are scrutinized. The effectiveness of automated remediation, reporting relationships, and business risks in influencing EA’s reliance on IAF work are discussed. Notably, audit committee effectiveness and the risks to objectivity and professionalism faced by external auditors are highlighted, especially in the context of stricter regulations post the Sarbanes–Oxley Act. The quality of internal audit tasks, their impact on audit judgments, and the struggles external auditors face in evidence integration are thoroughly examined. Despite these insights, research gaps emerge, including the need for more exploration of EAs’ use of internal auditors and their previous work, understanding the impact of internal auditor performance on external auditor reliance, and resolving mixed results on external auditors’ dependence on internal auditor performance. Future research suggestions encompass investigating the impact of customer pressure, exploring strategies for addressing subpar internal audit performance, assessing the role of reporting relationships and business risks, and delving into innovative approaches to safeguard external auditor independence and address risks to objectivity and professionalism. Furthermore, there’s a call for in-depth studies on the impact of stricter regulations on the internal audit role, exploring new methods to enhance the quality of internal audit tasks, investigating factors influencing external auditors’ struggle with evidence integration, and assessing the impact of internal auditors’ involvement in non-audit functions on external auditor assessment and reliance.

2.1.2. The Role of IAF in Enhancing Financial Reporting Integrity and EA Effectiveness

The interplay between IAFs and external auditors is pivotal in shaping financial reporting integrity and enhancing the effectiveness of external audits. Internal control deficiencies have far-reaching implications, affecting financial estimates and the extent of reliance external auditors place on IAFs, thereby influencing audit efficacy and fiscal outcomes.

Guided by the PCAOB’s advocacy for increased reliance on internal audit outcomes to augment audit quality, auditors operating in a comprehensive audit environment exhibit a preference for leaning on internal audit findings, especially when previous reports confirm the effectiveness of controls (Malaescu & Sutton, 2015). The collaboration between external auditors, upper management capacity, and the autonomy of internal auditors contribute positively to internal audit outcomes (Alqudah et al., 2019). Notably, diminished efficiency is observed when dependent auditors maintain strong connections with observer errors, a trend that is mitigated when the main auditor is affiliated with a Big Four firm or a specialized business (Noh et al., 2017).

Research exploring the impact of IAF on management reporting of external audit (EA) quality reveals intriguing insights. Abbott et al. (2012a) demonstrate that engaging IAF workers as assistants reduces audit delays, especially in situations of poor control reliance. Furthermore, higher IAF quality and cooperation with external auditors enhance audit efficiency when IAFs are utilized as assistants. On the other hand, Pizzini et al. (2015) highlight that IAF quality decreases audit latency. However, unlike Abbott et al. (2012a), audit latency decreases only when EAs rely on the IAF’s work, not when they act as assistants. Lin et al. (2011) affirm that strong cooperation between IAFs and EAs positively correlates with material weakness disclosures, indicating an overall improvement in EA quality through collaborative efforts. Collectively, this evidence suggests that employing IAFs improves audit efficiency and reduces delays.

Grey and Hunton’s (2011) findings shed light on the nuanced factors influencing EAs’ reliance on IAFs. Notably, the reporting structure, where the IAF reports to the CFO instead of the audit committee, could impact auditors’ reliance due to variations in how they evaluate the IAF’s competence and objectivity. Early studies underscore the importance of IAF quality parameters, emphasizing that compliance with Internal Auditors (IIA) standards and a lack of conflicting tasks enhance the perception of IAF competence and objectivity (Breger et al., 2020; Schneider 1984, 1985; Margheim 1986; Messier & Schneider 1988). Auditing Standard No. 5’s recommendation for external auditors to rely on internal auditors’ work emerges as a guiding principle for enhancing audit efficiency and effectiveness (Stefaniak et al., 2011).

In addition, the nature of internal audit tasks in non-family organizations, serving as a managerial training base, influences the degree of reliance on external audits due to perceived impartiality. Conversely, under a managerial training base system, external auditors’ reliance on internal auditing in family companies and their perception of impartiality remain largely unchanged (Suh et al., 2020; Čular et al., 2020). The degree of trust external auditors place in the internal audit department is influenced by factors such as the delivery of risk management counseling, the strength of the audit committee, and the provision of assurances (Čular et al., 2020).

Jordanian auditors highlight the value of collaboration between internal and external auditors in enhancing financial reporting quality, with impartiality playing a pivotal role. Moreover, the technical proficiency of internal audit practice is identified as a contributing factor to financial reporting efficacy (Azzam et al., 2020).

The analysis of SLR about the role of IAF in enhancing financial reporting integrity and EA effectiveness emphasizes the crucial role of IAF in enhancing financial reporting integrity and external audit effectiveness. Internal control shortcomings influence financial estimation and external auditors’ reliance, impacting audit efficacy and fiscal consequences. The PCAOB promotes increased reliance on internal audit outcomes for better audit quality. Engaging IAF workers as assistants reduces audit delays, and collaboration with external auditors enhances audit efficiency. Reporting to the CFO increases auditors’ reliance on the IAF, guided by evaluations of objectivity and competence. Non-family organizations’ internal audit tasks reduce reliance on external audits due to perceived impartiality. Collaboration between internal and external auditors improves financial disclosure quality, with impartiality playing a critical role. The research offers valuable insights for auditors, organizations, and stakeholders, suggesting areas for future research to enhance audit practices and effectiveness.

This part delves into crucial themes surrounding the collaboration between IAFs and external auditors, emphasizing its pivotal role in shaping financial reporting integrity and enhancing external audit effectiveness. Internal control deficiencies emerge as influential factors with far-reaching implications, impacting financial estimates and determining the extent of external auditor reliance on IAFs. The study notes increased reliance on internal audit outcomes, guided by the Public Company Accounting Oversight Board’s (PCAOB) advocacy for augmenting overall audit quality. Collaborative dynamics, reporting structures, and the impact of IAF quality parameters are explored, highlighting the nuanced factors affecting auditors’ reliance. Identified gaps call for further exploration of reporting structure nuances, a comprehensive understanding of IAF impact, a detailed examination of the effects of internal control deficiencies, and a deeper exploration of the nature of internal audit tasks in non-family organizations serving as managerial training bases. Future research suggestions include comprehensive evaluations of reporting structures in varied organizational contexts, in-depth analyses of collaboration dynamics, quantitative studies on the impact of IAF quality parameters, longitudinal examinations of internal control deficiencies, exploration of cross-cultural perspectives on collaboration, and investigations into the influence of technological advancements on audit efficacy.

2.1.3. The Challenges and Impact Faced by EA Through Their Reliance on IAF

The landscape of external auditors (EAs) relying on IAFs is complex and influenced by a multitude of factors. This section delves into the challenges faced and the ensuing impact on audit practices and outcomes.

Audit standards (ISA 610, SAS 65, Auditing Standard No. 5—PCAOB 2007) provide leeway for EAs to rely on IAF work, but this permission is underscored by the necessity to ensure its effectiveness. Auditors engage expert judgment during planning, evaluating the reliability of internal auditors’ tasks and emphasizing the critical assessment of the internal audit division’s competency and integrity (AICPA, 1991).

The intricacies of reliance decisions involve simultaneous evaluations of multiple aspects. Changing audit standards introduce intermediary judgments, and Bame-Aldred et al. (2013) highlight the need for a deeper understanding of how EAs assess the quality of internal audit activities. Lee and Park’s (2016) discovery of a positive connection between the number of internal auditors and external audit hours suggests a tangible contribution to financial statement audits and enhanced audit efficiency.

EAs’ reliance on internal audit in clients receiving non-audit services is more influenced by client demands than internal audit competence (Felix et al., 2005). Interaction challenges, encompassing internal audit engagement, fiscal challenges, and perceived risk, influence reliance decisions and are notable considerations (Brody, 2012).

EAs encounter obstacles to their professional independence, but adopting internal control features helps mitigate challenges, particularly in the context of bank audits (Kamil & Ahmed, 2020). Impact of Outsourcing: Outsourcing internal auditors correlates with increased reliance, particularly when intrinsic risk is high (Glover et al., 2008). EAs are urged to assess the qualifications of outsourced internal auditors to ensure competency in evaluating risks and controls within the user organization.

Liability judgments, as explored by Arel et al. (2013) and Munro & Stewart (2011), unveil nuanced patterns where EAs relying on internal IAF face more liability. While auditors do not heavily depend on non-financial measures, a nuanced approach is observed, with an increased reliance on these measures when assessing revenue estimates and challenging client balances, especially in high fraud-risk scenarios (Brazel et al., 2014).

The credibility of management experts is rooted in accounting competency, reputation, and validated credentials. Concerns around documentation and transitioning to a checklist approach are highlighted (Agrawal et al., 2020). Heavy reliance on private auditing by banks poses challenges, particularly when government loans are scarce, impacting collateral and societal welfare (Tuluk, 2021).

Notably, dissatisfaction surfaces among external auditors concerning internal audit personnel, education services, and organizational conditions (Alktani & Ghareeb, 2014). Surprisingly, a PCAOB examination’s impact on reliance remains limited, with efficiency-focused testing showing a paradoxical result—greater dependence when engagement risk is low (Petherbridge & Messier, 2015). In navigating deficiencies in company management, auditors turn to the compensatory power of robust internal control, a strategic move that contributes to enhancing auditors’ overall credibility in the audit process. Audit method type and intrinsic risk emerge as pivotal influencers shaping auditors’ preferences for relying on internal auditing. Moreover, auditors’ reliance decisions are significantly swayed by their prior professional experiences (Quick & Henrici, 2019).

The limited interactions between internal and external auditors pose a challenge, hindering the comprehensive utilization of the internal audit role (Mubako & Muzorewa, 2019). Strained interactions and inadequate management activities further compound the challenge, impacting positive engagement in the audit process. Trust in internal audit findings is nuanced, with a distinct preference for factual over subjective information, particularly when risks are involved. This trust dynamic plays a crucial role in shaping auditors’ reliance decisions on internal audit outputs. Externalization or co-sourcing of IAFs becomes a factor influencing the final dependence decision (Desai et al., 2011; Lowe et al., 1999). Complementing roles between external and IAFs are increasingly observed, indicating a trend toward collaborative and synergistic audit practices.

Foreign internal auditors from Big Four firms significantly interact with external audits (Baatwah et al., 2019). The degree of internal auditors’ adherence to professional standards is identified as a critical factor shaping external auditors’ reliance on them (Mustapha & Lee, 2020). External auditors are urged to meticulously assess the qualifications of outsourced internal auditors, ensuring their competence in evaluating risks and controls within the user organization. This assessment, however, often does not consider the qualities of service auditors. While adopting the IAF for management training proves beneficial in enhancing operational performance, it introduces a caveat by raising accounting risk, necessitating cautious consideration (Christ et al., 2012).

External auditors should assess the qualifications of outsourced internal auditors to ensure their competency in evaluating risks and controls within the user organization. Service auditor qualities are not considered in this assessment. Internal auditors do not provide financial statement services, so the user auditor must independently test or vet internal audit processes before relying on an external internal auditor (Bierstaker et al., 2013). Also, internal audit unit usage impacts audit adequacy (Messier et al., 2011). Complementing roles between external and internal audits have been observed (Rabóczki, 2018).

In conclusion, this analysis unearths the intricate challenges and impacts faced by EAs through their reliance on IAF. From navigating audit standards to addressing client demands, ensuring internal audit quality, and balancing reliance considerations, auditors are confronted with multifaceted decisions. The significance of enhanced communication and collaboration between auditors is emphasized for effective reliance, improved practices, and ultimately, ensuring the integrity of the audit process.

This classification navigates through key themes related to the complexity of reliance decisions and professional judgment, highlighting factors such as client demands, outsourcing impacts, trust dynamics, collaborative practices, and liability judgments. Gaps in the literature include a limited understanding of how external auditors assess internal audit quality, the predominant influence of client demands on reliance decisions, and the need for comprehensive insights into the impact of outsourcing, trust dynamics, and auditors’ preference for factual information. Suggestions for future research propose in-depth assessments of internal audit quality, exploration of client-centric reliance and interaction dynamics, comprehensive understanding of outsourcing impacts, exploration of trust dynamics and information preference, strategies for enhancing interactions for collaboration, exploration of regulatory compliance and global trends, investigation into qualification assessment and risk evaluation, and cautious exploration of adopting IAF for management training.

2.1.4. The Impact of IAF on EA Fees and Quality

Previous research highlights multifaceted connections between the IAF and External Audit (EA) fees and quality, unveiling nuances in their interactions. Carcello et al. (2018) reveal a negative impact on external audit fees, financial reporting quality, and internal auditing effectiveness when the IAF is utilized for management training. In contrast, Abbott et al. (2012b) suggest that a stronger influence of the audit committee on the IAF results in lower external audit fees. This reflects heightened external auditor reliance on the IAF, translating to improved audit effectiveness.

Conversely, the mere presence of an IAF is linked to higher external audit charges. Larger internal audit departments exhibit positive correlations with elevated external auditor fees, improved audit quality, and an increased likelihood of engaging Big Four firms (Axén, 2018). Surprisingly, while reliance on internal audits does not necessarily reduce external audit charges or tasks for local governments in Great Britain, higher external audit fees can lead to a decrease in reliance on internal audits (Saidin, 2014). Meta-analyses, such as those conducted by Hay , underscore a connection between investments in both external and internal audits in financial audit contexts.

There is an underlying assumption in many studies that audit fees are representative of EA efforts. Using completed IAF work or relying on the IAF is expected to yield cost savings. Prawitt et al. (2011) find that IAF hours supporting EAs result in lower audit fees, yet there is no conclusive evidence that the time spent on such activities impacts fees or reliance, nor does it determine IAF quality.

Echoing these findings, Abbott et al. (2012a) report similar results, emphasizing that IAF hours supporting EAs can lead to reduced audit fees. However, this reduction is particularly prominent with increased IAF funding and audit committee control. Intriguingly, utilizing the IAF as a training ground for management is associated with increased audit fees (Messier et al., 2011), potentially due to elevated accounting risk. Notably, relying on previously completed IAF work, rather than seeking direct assistance, results in more substantial reductions in audit fees (Albawwat, 2022).

The study by Abdul Wahab et al. (2021) introduces the concept that high audit quality achieved through outsourced IAFs may prompt auditors to accept lower fees for providing non-audit services to clients. The correlation between IAF quality and audit fees, coupled with increased reliance on external auditors’ work, suggests that higher-quality IAFs foster greater dependence on external audit work, thereby reducing external audit costs (Mat Zain et al., 2015).

In summary, this analysis delves into the intricate dynamics of the IAF’s impact on EA fees and quality. It is evident that training use lowers fees, while audit committee influence decreases fees and enhances effectiveness. A competent IAF may raise charges but simultaneously enhances quality and attracts prestigious firms. Direct reliance on internal audits might not directly impact charges, but higher fees reduce reliance. The integration of internal and external audits emerges as a strategy to improve efficiency and outcomes. Effective collaboration with the IAF has the potential to reduce costs, highlighting the need for further research and the development of strategies for fostering enhanced auditor collaboration.

This section examines the nuanced impact of IAF on EA fees and quality, showcasing both positive and negative influences. Noteworthy findings reveal contrasting effects, with internal audit department size emerging as a pivotal factor influencing external auditor fees and audit quality. The assumption that audit fees reflect EA efforts is acknowledged, with studies exploring the relationship between IAF hours and resulting audit fees. The association between using IAF for management training and increased audit fees is indicated. Outsourcing IAF functions is linked to high audit quality and reduced external audit costs. The potential benefits of integrating internal and external audits for improved efficiency are implied but not explicitly outlined. Research gaps include the need for a more profound quantitative exploration of the impact of IAF utilization for management training on audit fees, elucidation of the causal relationship between IAF funding and fee reduction, and a comprehensive exploration of IAF outsourcing. Future research suggestions involve conducting quantitative analyses on the training impact of IAF, in-depth investigation of IAF funding impact, nuanced exploration of IAF outsourcing, validation of integration strategies, and comprehensive exploration of collaboration strategies with the IAF to reduce costs.

2.1.5. The Impact of IAF on EAs’ Reliance and Financial Statement Quality

Kaplan and Schultz’s (2006) survey, revealed that 88 percent of Chief Audit Executives (CAEs) reported External Auditor (EA) reliance on their IAF, signifies a pivotal relationship. While the impact of IAF reliance on audit effectiveness is acknowledged, its varied effects on the value of external audits are recognized. However, challenges arise due to limited public disclosures in standard audit reports, challenging assessing IAF reliance effects. This lack of accessible open data further complicates the measurement of IAF performance. Archambeault et al. (2008) highlight a critical issue—external stakeholders lack detailed IAF information, leading to information asymmetry that may reduce stakeholder confidence. Governance disclosures typically concentrate on management, the audit committee, and the External Auditor (EA), neglecting essential IAF details for external stakeholders.

Despite the acknowledged challenges of limited disclosure (Archambeault et al., 2008), our investigation into the impact of EAs’ reliance on IAFs on audit quality follows two key avenues: (1) extrapolating indirect effects from IAF’s influence on financial reporting and (2) reviewing limited research on the direct influence of IAF reliance on audit quality. Prawitt et al. (2009) posit that IAFs contribute to enhancing financial reporting quality by addressing incentive system flaws, as evidenced by confidential archive data. Lin et al. (2011) uncovered negative correlations between material weakness disclosures and IAF attributes such as staff education, the use of quality assurance techniques, auditing activities related to financial reporting, and monitoring remediation, based on archived data from 214 firms.

Stefaniak et al. (2012) add a nuanced layer by revealing that internal auditors identify more strongly with their employers than EAs do with clients. This heightened internal auditor employer identification leads to stricter control deficiency evaluations, while greater EAs’ client identification results in more lenient evaluations. This dynamic suggests that increased reliance on the IAF by EAs may improve audit quality with less lenient internal control deficiency judgments, influenced by employer and client identities. However, Bedard and Graham (2011) present differing results, indicating that EAs frequently override IAF assessments of control flaws, with IAFs considering them less severe. Bedard and Graham (2011) also emphasize that IAFs are less effective in detecting severe and extensive control flaws compared to EAs. This underscores the significance of EAs’ Section 404 control testing to identify weaknesses and cautions against excessive reliance on IAF without proper oversight, potentially impacting audit quality. Further research is essential to determine if the IAF can impartially assess internal control problems, as suggested by Stefaniak et al. (2012). Additionally, highlighting the significance of collaboration, improved cooperation between internal and external auditors has been identified as a factor crucial for enhancing the timeliness of financial reporting (Oussii & Boulila Taktak, 2018).

3. Discussion

In summary, the analysis underscores the paramount importance of the IAF in the context of EAs, acknowledging its varied impacts on effectiveness and value. Despite these insights, the prevailing limited disclosures and data pose challenges in assessing the effects of IAF reliance, contributing to information asymmetry. The potential impact of IAF on audit quality unfolds through both direct and indirect avenues. Furthermore, the imperative of effective collaboration between auditors is highlighted as a means to enhance the timeliness of financial reporting. Despite these insights, further research is indispensable to unravel the complexities of IAF reliance and its nuanced effects on audit quality.

This analysis underscores the pivotal relationship between EAs and IAFs, emphasizing the centrality of the EA-IAF dynamic in ensuring audit effectiveness. However, challenges arise in assessing IAF reliance due to limited public disclosures, hindering a thorough understanding of its effects on audit quality. The lack of accessible open data further complicates the measurement of IAF performance. Information asymmetry is highlighted as external stakeholders lack detailed IAF information, potentially reducing confidence, and governance disclosures traditionally overlook crucial IAF details. Research into the impact of EAs’ reliance on IAFs reveals diverse effects on audit quality, with indirect influences on financial reporting and direct impacts. Nuanced findings on internal auditors’ identification with employers suggest potential improvements in audit quality with increased EA reliance on the IAF, but caution is needed due to conflicting results. The role of collaboration between internal and external auditors is recognized as significant for enhancing financial reporting timeliness. Research gaps include limited disclosures, data accessibility issues, the need for clarity on identity dynamics, and the impartiality of IAF assessments of internal control problems. Suggestions for future research involve encouraging enhanced disclosure practices, further exploration of identity dynamics, a comprehensive understanding of IAF impacts on financial reporting and audit quality, and continued exploration of collaboration strategies between internal and external auditors for improved financial reporting.

Table 1.

Key themes, gaps, and suggestions for future research demonstrated in the systematic review.

Table 1.

Key themes, gaps, and suggestions for future research demonstrated in the systematic review.

| Section | Key themes | Gaps | Suggestions for future research |

|---|---|---|---|

| 2.1.1 | Factors Influencing External Auditor Reliance. Automated Remediation vs. Human Efforts. Reporting Relationships and Business Risks. Audit Committee Effectiveness. Risk to Objectivity and Professionalism. Regulations and Internal Audit Role. Quality of Internal Audit Task. Impact of Internal Audit on Audit Judgments. Internal Auditing Competence and Objectivity. And, external Auditors’ Struggle with Evidence Integration. |

|

|

| 2.1.2 | Interplay Between IAFs and External Auditors. Impact of Internal Control Deficiencies. Advocacy for Increased Reliance. Collaboration Dynamics. Reporting Structure Impact. And the impact of IAF Quality Parameters. |

|

|

| 2.1.3 | Decision-making complexity and Professional Judgment. Influential Factors and Interaction Dynamics. Client Demands and Interaction Challenges. Outsourcing and Intrinsic Risk. Trust Dynamics and Information Preference. Collaborative Practices and Regulatory Considerations. Liability Judgments and Nuanced Patterns. Limited Interactions and Strained Dynamics. Globalization, Compliance, and Collaboration. Qualification Assessment and Risk Evaluation. And, cautious Adoption of IAF for Management Training. |

|

|

| 2.1.4 | Duality of IAF Impact. The multifaceted impact of the IAF on EA fees and quality is highlighted, showcasing both positive and negative influences. Internal Audit Department Size and Auditing Dynamics. The size of internal audit departments is identified as a key factor influencing external auditor fees, audit quality, and the likelihood of engaging prestigious audit firms. And, outsourcing IAF functions is linked to high audit quality, prompting auditors to accept lower fees for non-audit services. |

|

|

| 2.1.5 | Significance of EA-IAF Relationship. Challenges in Assessing IAF Reliance. Information Asymmetry and Governance Disclosures. Diverse Effects on Audit Quality. Identity Dynamics and Control Deficiency Evaluations. Role of Collaboration in Reporting Timeliness. |

|

|

In conclusion, synthesizing the insights gleaned from the systematic literature review presents a comprehensive understanding of the complex relationship between External Auditors (EAs) and IAFs. Addressing the identified gaps and heeding the suggestions for future research would significantly contribute to advancing this understanding. The multifaceted connections explored, including the impact on financial reporting integrity, audit fees, and audit effectiveness, underscore the intricate dynamics at play. Enhanced disclosure practices, further exploration of identity dynamics, and a nuanced examination of the impacts of IAF reliance emerge as pivotal areas for future research. By delving into these aspects, researchers can bridge existing gaps, provide clarity, and contribute to a more sophisticated comprehension of the nuanced interplay between EAs and IAFs in the realms of audit quality and financial reporting practices.

Summary of findings: The study extensively explores the intricate dynamics governing external auditors’ decisions regarding their reliance on IAFs. It uncovers that pivotal factors such as customer pressure, board connections, and business risks exert significant influence on these decisions. Notably, the research indicates that while automated remediation has limited impact, adopting less frequent and targeted remediation procedures proves superior. Collaborative efforts between external and internal auditors are identified as positively influencing financial reporting integrity and enhancing overall audit effectiveness. The challenges inherent in reliance decisions are unveiled, encompassing considerations of audit standards, client demands, and the potential impacts on professional independence. The study reveals multifaceted connections between IAF and external audit fees and quality, emphasizing the potential for effective collaboration to reduce costs. Despite recognizing the importance of IAF, the research underscores the need for further exploration to fully comprehend the complexities of IAF reliance and its nuanced effects on audit quality.

4. Materials and Methods

This study embraced a systematic strategy to carry out a literature review to reduce prejudice and provide its findings with scientific validity. To reduce bias and ensure scientific validity, this study used a methodological strategy to conduct a literature review. We drew from previous literature on auditing (Bellucci et al., 2022; Massaro et al., 2016; Denyer & Tranfield, 2009) obvious, comprehensive, informative, and intuitive essentials to maintain the integrity of our approach. In order to help authors improve the systematic review documentation, we disclose our analytic processes using the Ms. Office package in the Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA). PRISMA is a reporting process for systematic reviews that was created through the life sciences sector to improve the translucence and precision of the literature reviews. It consists of a checklist and a flow chart (Page et al., 2021). PRISMA was chosen over the other current protocols because of its generalizability, widespread usage across many fields (e.g., medicine and health), and capability to boost the uniformity of reviews (Pahlevan-Sharif et al., 2019).

4.1. Design of the Plan

Throughout the study, we adhered to the guidelines set forth by Jesson et al. (2011), which include the following steps: Defining the research question; Designing a plan; Conducting a Literature Search; Using exclusion and inclusion criteria; Undertaking the quality estimation; and Discussion of the Findings.

Accordingly, to gather pertinent literature from multiple sources, a thorough study was conducted with the following aims and objectives.

- To assess the extent and nature of external audit reliance on the IAF in organizations.

- To recognize the role of IAF in enhancing financial reporting integrity and EA effectiveness.

- To identify and analyze the challenges and impact faced by EA through their reliance on IAF.

- To evaluate the impact of IAF on EA fees and quality.

- To explore the impact of IAF on EAs’ reliance and financial statement quality.

4.2. Defining the Research Questions

Research questions that specify the title, aim, and context of the paper guide the systematic review process (Booth et al., 2012). Consequently, we determined the subsequent research inquiries:

Q1. What is the extent of external audit reliance on the IAF in organizations?

Q2. What is the role of IAF in enhancing financial reporting integrity and EA effectiveness?

Q3. What are the challenges and impacts faced by EA through their reliance on IAF?

Q4. What is the impact of IAF on EA fees and quality?

Q5. What is the Impact of IAF on EAs’ reliance and financial statement quality?

These questions make clear our aim to look into practical and academic aspects and the primary objectives of the systematic review procedures connected to the article.

4.3. Doing a Literature Search

After defining the research questions, the systematic literature review went through sequential procedures used to guide the conduct of research, as shown in Table 2.

4.4. Using the Criteria of Exclusion and Inclusion

The three components of the search approach are keyword identification, screening, and eligibility. The research topic served as the foundation for the selection of keywords: External auditing reliance, reliance decision, and IAF, which were the keywords chosen for this review. The study drew articles from multiple databases, primarily Scopus and Web of Science, supplemented by Google Scholar. This study searched Google Scholar, Scopus, and Web of Science for studies on the external audit reliance decision. The databases were chosen based on access rights, availability, and references listed in papers published during the specified interval that dealt with external audit reliance and IAF. Additionally, the chosen databases made a significant number of peer-reviewed articles available in the research field. The search criteria are listed in Table 2. The inclusion criteria were as follows.

- Research regarding external audit reliance on the IAF.

- Research released in 1984 and 2022.

- Research released in English.

- This research has been reported in one of the most reputable and referenced publications.

4.5. Undertaking the Quality Estimation

In a systematic literature review, the initial abstract of each study was investigated, and the details of each study were analyzed to acquire a greater understanding of the review’s goal. The major findings from each research were then documented and utilized in the creation of a systematic literature review (Page et al., 2021). Since external audit reliance is a relatively contemporary research issue, we decided to include conference proceedings and book chapters in addition to the publications. The exploration and mining of the study data were performed in one of the four stages:

- Publications can be found by researching online databases for the terms “external auditing reliance”, “reliance decision”, and “internal audit function”, additionally, duplicate entries were deleted.

- We carefully examined the headlines, abstracts, keywords, and, if needed, the content of the publications to identify those that should be deleted due to irrelevance (Booth et al., 2012).

- Exclusions were made with good justification after eligibility was determined by a full-text evaluation of the papers.

- For a thorough analysis, publications with cross-references were screened, and the ultimate choice of publications to be considered for the systematic review was determined.

The redundant publications were excluded from the analysis. The abstracts and titles of the study papers were carefully examined for their appropriateness. Additionally, the reference lists of publications that had already been chosen were searched for additional pertinent research. The selected publications were investigated. According to the justifications and conclusions employed in each study, the selected publications are categorized into five groups according to the research objectives.

4.6. The Diagram of PRISMA

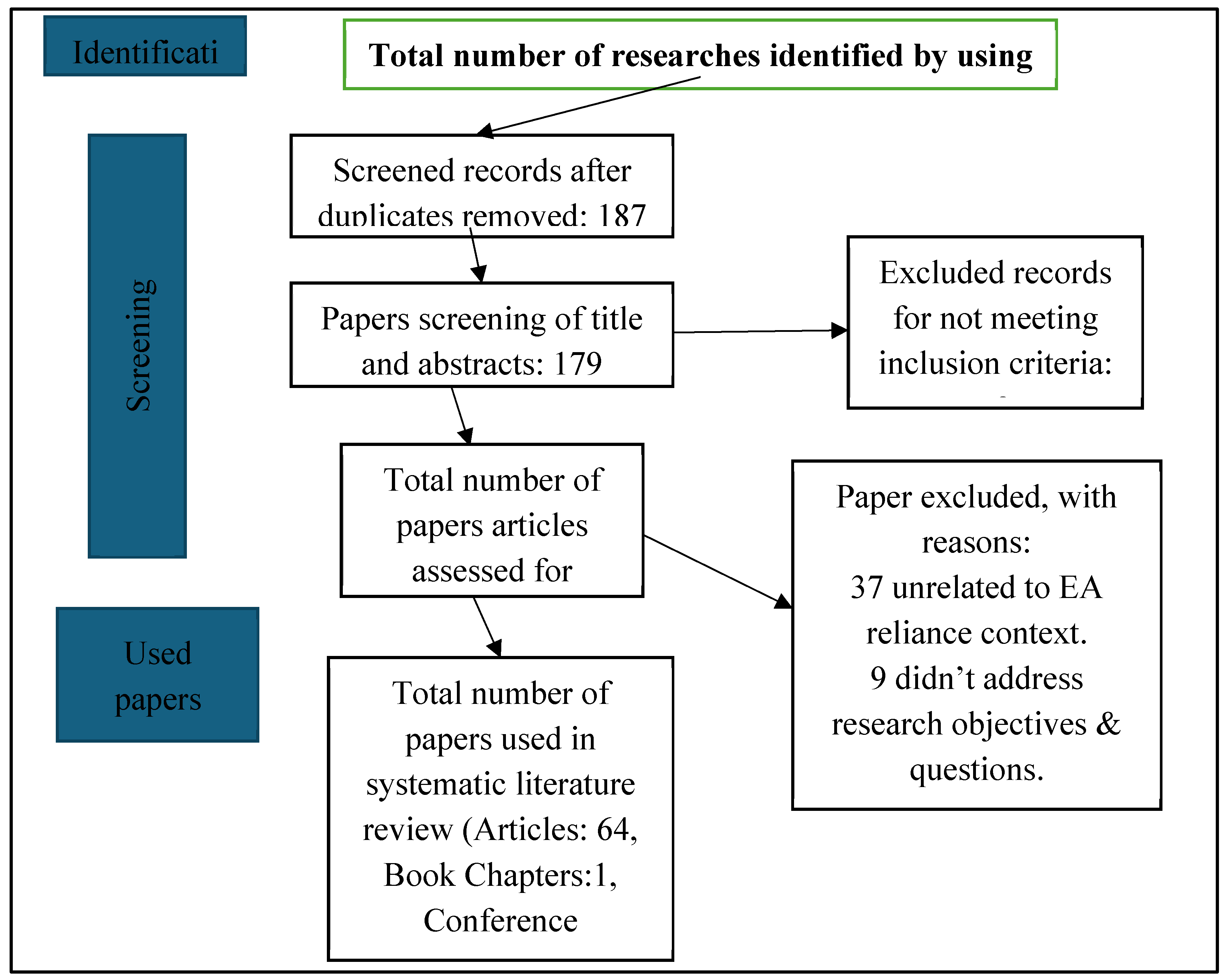

The importance of external audit reliance in the audit process was highlighted by the systematic review. Figure 2 illustrates the procedures we took when utilizing a PRISMA diagram that we modified to better match a qualitative systematic review (Page et al., 2021). The movement of information via the multiple phases for a systematic review is pictorial in the PRISMA diagram. It is pictorial the quantity of documents that were found, included, excluded, and the explanations for exclusions.

4.7. Details of the Presented Publications

Lastly, chosen publications were evaluated in light of the systematic review’s scope. A sum of 68 publications was chosen and used to gain a better understanding of the goals. There were 64 publication research reports, 1 book chapter, 1 conference proceeding, and 2 working papers. In a systematic literature review, the initial abstract of each study is investigated, and then the details of each research are analyzed to acquire an in-depth understanding of the review’s objectives. The major findings from each research are then documented and utilized in the creation of a systematic literature review (Page et al., 2021). The overall number of pertinent articles is presented according to the sources in Table 3.

Table 3.

Articles illustrated in the systematic review.

| Source | A number of concerning studies |

|---|---|

| Scopus and Web of Science | 56 |

| Google Scholar | 12 |

| Total publications | 68 |

The search resulted in a total of 193 publications (from 1984 to 2022) from March 2022 to July 2023 as a work period. Scopus and Web of Science findings included fifty-six articles and the rest of the twelve articles were from Google Scholar.

5. Conclusions

The conclusions drawn from the comprehensive analysis of the article are intricately tied to the research objectives, shedding light on the multifaceted relationships between external audit reliance on IAFs and various organizational dynamics. Firstly, in line with the first objective, the study effectively assesses the extent and nature of external audit reliance on IAFs, revealing that factors such as customer pressure, organizational connections, and business risks significantly shape these reliance decisions. The outcomes provide a nuanced understanding of the complex interplay involved in these decisions. Secondly, the research supports the recognition of the vital role of IAFs in enhancing financial reporting integrity and external audit effectiveness, showcasing those collaborative efforts positively impact financial disclosure quality and overall audit efficiency. Thirdly, concerning the challenges and impact faced by external auditors through their reliance on IAFs (objective three), the study brings to light various obstacles, including client demands, changing audit standards, and issues related to professional independence, effectively addressing the research objective. Fourthly, concerning evaluating the impact of IAF on external audit fees and quality (objective four), the article uncovers multifaceted connections, indicating that while certain factors may raise charges, they simultaneously enhance audit quality, contributing to a nuanced understanding of these relationships. Lastly, the exploration of the impact of IAF on external auditors’ reliance and financial statement quality (objective five) unveils the paramount importance of IAF in influencing audit quality through both direct and indirect avenues. The study, in its conclusions, underscores the significance of continued exploration in understanding the intricate relationships between external and internal auditors, emphasizing the need for effective collaboration to enhance audit practices and effectiveness. Overall, the conclusions are well-supported by the detailed results, offering valuable insights for auditors, organizations, and stakeholders.

However, the research also indicates some limitations and areas for further investigation. The mixed results concerning auditors’ reliance on internal auditor performance call for more comprehensive research to better understand the dynamics of this aspect. The impact of automated remediation on IAF performance and reliance also warrants further exploration, as does the influence of data analytics adoption on external auditing. Additionally, understanding the implications of stricter regulations on the importance of the internal audit role could provide valuable insights into audit practices.

In conclusion, this systematic literature review has made a significant contribution to the existing body of literature on external audit reliance on the IAF. It has highlighted the factors influencing this relationship and emphasized the importance of effective collaboration between internal and external auditors for enhancing audit quality and financial reporting integrity. The identified limitations and gaps in the research present opportunities for future studies in this field. Investigating the influence of technology adoption, regulatory changes, and the interplay of auditors’ perceptions and decision-making could further expand knowledge and understanding in this area. The implications of this research extend to auditors, organizations, and stakeholders, providing guidance for optimizing audit practices and promoting transparency in the audit process.

Author Contributions

For research articles with several authors, a short paragraph specifying their individual contributions must be provided. The following statements should be used “Conceptualization, X.X. and Y.Y.; methodology, X.X.; software, X.X.; validation, X.X., Y.Y. and Z.Z.; formal analysis, X.X.; investigation, X.X.; resources, X.X.; data curation, X.X.; writing—original draft preparation, X.X.; writing—review and editing, X.X.; visualization, X.X.; supervision, X.X.; project administration, X.X.; funding acquisition, Y.Y. All authors have read and agreed to the published version of the manuscript.” Please turn to the CRediT taxonomy for the term explanation. Authorship must be limited to those who have contributed substantially to the work reported.

Funding

This research received no external funding.

Acknowledgments

Thanks to Middle East University for Continuous Support.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Abbott, L.J.; Parker, S.; Peters, G.F. Internal audit assistance and external audit timeliness. Auditing: A Journal of Practice & Theory 2012a, 31, 3–20. [Google Scholar] [CrossRef]

- Abbott, L.J.; Parker, S.; Peters, G.F.; Rama, D.V. Corporate governance, audit quality, and the Sarbanes-Oxley Act: Evidence from internal audit outsourcing. The Accounting Review 2007, 82, 803–835. [Google Scholar] [CrossRef]

- Abbott, L.; Parker, S.; Peters, G.F. Audit fee reductions from internal audit-provided assistance: the incremental impact of internal audit characteristics. Contemporary Accounting Research 2012b, 29, 94–118. [Google Scholar] [CrossRef]

- Abdul Wahab, E.A.; Gist, W.E.; Gul, F.A.; Mat Zain, M. Internal auditing outsourcing, non-audit services, and audit fees. Auditing: A Journal of Practice & Theory 2021, 40, 23–48. [Google Scholar] [CrossRef]

- Agrawal, P.; Tarca, A.; Woodliff, D. External auditors’ evaluation of a management’s expert’s credibility: Evidence from Australia. International Journal of Auditing 2020, 24, 90–109. [Google Scholar] [CrossRef]

- AICPA. Statement on Auditing Standards No, 65: The auditors’ consideration of the internal audit function in an audit of financial statements; AICPA: New York, NY, 1991. [Google Scholar]

- Albawwat, I.E. External auditors’ reliance on the internal audit functions and audit fees. Global Business and Economics Review 2022, 26, 436–456. [Google Scholar] [CrossRef]

- Alktani, S.; Ghareeb, A. Evaluation of the Quality of the Internal Auditing Position in the Public Sector in Saudi Arabia: An Applied Study. Global Review of Accounting and Finance 2014, 5, 93–106. [Google Scholar] [CrossRef]

- Alqudah, H.M.; Amran, N.A.; Hassan, H. Factors affecting the internal auditors’ effectiveness in the Jordanian public sector: The moderating effect of task complexity. EuroMed Journal of Business 2019, 14, 251–273. [Google Scholar] [CrossRef]

- Al-Twaijry AA, M.; Brierley, J.A.; Gwilliam, D.R. An examination of the relationship between internal and external audit in the Saudi Arabian corporate sector. Managerial Auditing Journal 2004, 19, 929–944. [Google Scholar] [CrossRef]

- Alzeban, A.; Gwilliam, D. Factors affecting the internal audit effectiveness: A survey of the Saudi public sector. Journal of International Accounting, Auditing and Taxation 2014, 23, 74–86. [Google Scholar] [CrossRef]

- Archambeault, D.S.; DeZoort, F.T.; Holt, T.P. The need for an internal auditor report to external stakeholders to improve governance transparency. Accounting Horizons 2008, 22, 375–388. [Google Scholar] [CrossRef]

- Arel, B.; Jennings, M.M.; Pany, K.; Reckers, P.M. Auditor liability: A comparison of judge and juror verdicts. Journal of Accounting and Public Policy 2013, 31, 516–532. [Google Scholar] [CrossRef]

- Argento, D.; Umans, T.; Håkansson, P.; Johansson, A. Reliance on the internal auditors’ work: experiences of Swedish external auditors. Journal of Management Control 2018, 29, 295–325. [Google Scholar] [CrossRef]

- Axén, L. Exploring the association between the content of internal audit disclosures and external audit fees: Evidence from Sweden. International Journal of Auditing 2018, 22, pp. 285–297. [Google Scholar] [CrossRef]

- Azzam, M.J.; Alrabba, H.M.; AlQudah, A.M.; Mansur HM, A. A study on the relationship between internal and external audits on financial reporting quality. Management Science Letters 2020, 10, 937–942. [Google Scholar] [CrossRef]

- Baatwah, S.R.; Al-Ebel, A.M.; Amrah, M.R. Is the type of outsourced internal audit function provider associated with audit efficiency? Empirical evidence from Oman. International Journal of Auditing 2019, 23, 424–443. [Google Scholar] [CrossRef]

- Bame-Aldred, Charles and Brandon, Duane M. and Messier Jr, William F. and Rittenberg, Larry and Stefaniak, Chad M. (2013). A Summary of Research on External Auditor Reliance on the Internal Audit Function. Auditing: A Journal of Practice and Theory, Forthcoming, Northeastern U. D’Amore-McKim School of Business Research Paper No. 2013-11, 32(SUPPL.1), pp. 251–286.

- Bedard, J.C.; Graham, L. Detection and severity classifications of Sarbanes-Oxley Section 404 internal control deficiencies. The Accounting Review 2011, 86, 825–855. [Google Scholar] [CrossRef]

- Bellucci, M.; Cesa Bianchi, D.; Manetti, G. Blockchain in accounting practice and research: systematic literature review. Meditari Accountancy Research 2022, 30, 121–146. [Google Scholar] [CrossRef]

- Bierstaker, J.; Chen, L.; Christ, M.H.; Ege, M.; Mintchik, N. Obtaining assurance for financial statement audits and control audits when aspects of the financial reporting process are outsourced. Auditing: A Journal of Practice & Theory 2013, 32 (Suppl. 1), 209–250. [Google Scholar] [CrossRef]

- Booth, A.; Papaioannou, D.; Sutton, A. Systematic Approaches to a Successful Literature Review; Sage: London, 2012. [Google Scholar]

- Brandon, D.M. External auditor evaluations of outsourced internal auditors. Auditing 2010, 29, 159–173. [Google Scholar] [CrossRef]

- Brazel, J.F.; Jones, K.L.; Prawitt, D.F. Auditors’ reactions to inconsistencies between financial and nonfinancial measures: The interactive effects of fraud risk assessment and a decision prompt. Behavioral Research in Accounting 2014, 26, 131–156. [Google Scholar] [CrossRef]

- Breger, D.; Edmonds, M.; Ortegren, M. Internal audit standard compliance, potentially competing duties, and external auditors’ reliance decision. Journal of Corporate Accounting & Finance 2020, 31, 112–124. [Google Scholar] [CrossRef]

- Brody, R.G. External auditor’s willingness to rely on the work of internal auditors: The influence of work style and barriers to cooperation. Advances in Accounting. 28 2012, 11–21. [Google Scholar] [CrossRef]

- Carcello, J.V.; Eulerich, M.; Masli, A.; Wood, D.A. The value to management of using the internal audit function as a management training ground. Accounting Horizons 2018, 32, 121–140. [Google Scholar] [CrossRef]

- Chen, L.H.; Chung, H.H.; Peters, G.F.; Wynn, J.P. Does Incentive-based Compensation for Chief Internal Auditors Impact Objectivity? An External Audit Risk Perspective. Auditing: A Journal of Practice & Theory 2017, 36, 21–43. [Google Scholar] [CrossRef]

- Christ, M.H.; Eulerich, M.; Krane, R.; Wood, D.A. New Frontiers for Internal Audit Research. Accounting Perspectives 2021, 20. [Google Scholar] [CrossRef]

- Christ, M. H.; Masli, A.; Sharp, N. Y.; Wood, D. A. Using the internal audit function as a management training ground: Is the monitoring effectiveness of internal auditors compromised. SSRN Electronic Journal, Working Paper. University of Georgia. 2012. [Google Scholar] [CrossRef]

- Čular, M.; Slapničar, S.; Vuko, T. The Effect of Internal Auditors’ Engagement in Risk Management Consulting on External Auditors’ Reliance Decision. European Accounting Review 2020, 29, 999–1020. [Google Scholar] [CrossRef]

- Denyer, D.; Tranfield, D. Producing a systematic review, The Sage Handbook of Organizational Research Methods; Sage Publications: London, 2009; pp. 671–689. [Google Scholar]

- Desai, N.; Gerard, G.J.; Tripathy, A. Internal audit sourcing arrangements and reliance by external auditors. Audit. J. Pract. Theory. 30 2011, 149–171. [Google Scholar] [CrossRef]

- Desai, R.; Desai, V.; Libby, T.; Srivastava, R.P. External Auditor’s Evaluation of the Internal Audit Function: An Empirical Investigation. International Journal of Accounting Information Systems 2017, 24, 1–14. [Google Scholar] [CrossRef]

- Desai, V.; Roberts, R.W.; Srivastava, R. An analytical model for external auditor evaluation of the internal audit function using belief functions. Contemporary Accounting Research 2010, 27, 537–575. [Google Scholar] [CrossRef]

- Duska, R. The Good Auditor—Skeptic or wealth accumulator? Ethical lessons learned from the Arthur Andersen debacle. Journal of Business Ethics 2005, 57, 17–29. [Google Scholar] [CrossRef]

- Dzikrullah, A.D.; Harymawan, I.; Ratri, M.C. Internal audit functions and audit outcomes: Evidence from Indonesia. Cogent Business & Management 2020, 7, 1750331. [Google Scholar] [CrossRef]

- Farkas, M. J.; Hirsch, R. M. The Effect of Frequency and Automation of Internal Control Testing on External Auditor Reliance on the Internal Audit Function. Journal of Information Systems 2016, 30, 21–40. [Google Scholar] [CrossRef]

- Felix Jr, W.L.; Gramling, A.A.; Maletta, M.J. The influence of non-audit service revenues and client pressure on external auditors’ decisions to rely on internal audit. Contemporary Accounting Research 2005, 22, 31–53. [Google Scholar] [CrossRef]

- Glover, S.M.; Prawitt, D.F.; Wood, D.A. Internal audit sourcing arrangement and the external auditor’s reliance decision. Contemporary Accounting Research 2008, 25, 193–213. [Google Scholar] [CrossRef]

- Gramling, A.A.; Maletta, M.J.; Schneider, A.; Church, B.K. The role of the internal audit function in corporate governance: A synthesis of the extant internal auditing literature and directions for future research. Journal of Accounting Literature 2004, 23, 194. [Google Scholar]

- Gray, J.; Hunton, J.E. External auditors’ reliance on the internal audit function: The role of second-order belief attribution. Unpublished working paper discussed at Bentley University 2011, 1–49. [Google Scholar]

- Hay, D. Further evidence from meta-analysis of audit fee research. International Journal of Auditing 2013, 17, 162–176. [Google Scholar] [CrossRef]

- International Federation of Accountants (IFAC). ISA 610 (revised). Using the Work of the Internal Audit Function and Internal Auditors to Provide Direct Assistance. 2013. [Google Scholar]

- Ismael, H.R.; Roberts, C. Factors affecting the voluntary use of internal audit: evidence from the UK. Managerial Auditing Journal 2018, 33, 288–317. [Google Scholar] [CrossRef]

- Jacky, Y.; Sulaiman, N.A. Factors Affecting the Use of Data Analytics in External Auditing. Management & Accounting Review 2022, 21. [Google Scholar]

- Jesson, J.; Matheson, L.; Lacey, F.M. Doing your literature review: Traditional and systematic techniques, FIRST EDITION; SAGE Publications Ltd., 2011; pp. 1–192. ISBN 9781446242391. [Google Scholar]

- Kamil, O.A.; Ahmed, E.A. Extent of Adoption of External Auditor on Internal Control in Bank Auditing. International Journal of Innovation, Creativity and Change 2020, 10, 612–624. [Google Scholar]

- Kaplan, S.; Schultz, J. The role of internal audit in sensitive communications.Altamonte Springs, FL: The Institute of Internal Auditors Research Foundation. 2006. [Google Scholar]

- Kok, M.; Maroun, W. Not all experts are equal in the eyes of the International Auditing and Assurance Standards Board: On the application of ISA510 and ISA620 by South African registered auditors. South African Journal of Economic and Management Sciences 2021, 24, 1–13. [Google Scholar] [CrossRef]

- Lee, H.Y.; Park, H.Y. Characteristics of the internal audit and external audit hours: evidence from S. Korea. Managerial Auditing Journal 2016, 31, 629–654. [Google Scholar] [CrossRef]

- Lin, S.; Pizzini, M.; Vargus, M.; Bardhan, I.R. The role of the internal audit function in the disclosure of material weaknesses. The Accounting Review 2011, 86, 287–323. [Google Scholar] [CrossRef]

- Lowe, D.J.; Geiger, M.A.; Pany, K. The effects of internal audit outsourcing on perceived external auditor independence. Auditing: A Journal of Practice & Theory 1999, 18, 7–26. [Google Scholar] [CrossRef]

- Malaescu, I.; Sutton, S. G. The reliance of external auditors on internal audit’s use of continuous audit. Journal of Information Systems 2015, 29, 95–114. [Google Scholar] [CrossRef]

- Margheim, L. L. Further evidence of external auditors’ reliance on internal auditors. Journal of Accounting Research 1986, 24, 194–205. [Google Scholar] [CrossRef]

- Massaro, M.; Dumay, J.; Guthrie, J. On the shoulders of giants: undertaking a structured literature review in accounting. Accounting, Auditing and Accountability Journal 2016, 29, 767–801. [Google Scholar] [CrossRef]

- Mat Zain, M.; Zaman, M.; Mohamed, Z. The effect of internal audit function quality and internal audit contribution to external audit on audit fees. International journal of auditing 2015, 19, 134–147. [Google Scholar] [CrossRef]

- Messier Jr, W.F.; Schneider, A. A hierarchical approach to the external auditor’s evaluation of the internal auditing function. Contemporary Accounting Research 1988, 4, 337–353. [Google Scholar] [CrossRef]

- Messier Jr, W.F.; Reynolds, J.K.; Simon, C.A.; Wood, D.A. The effect of using the internal audit function as a management training ground on the external auditor’s reliance decision. The accounting review 2011, 86, 2131–2154. [Google Scholar] [CrossRef]

- Mihret, D.G. How Can We Explain Internal Auditing? The Inadequacy of Agency Theory and A Labor Process Alternative. Critical Perspectives on Accounting 2014, 25, 771–782. [Google Scholar] [CrossRef]

- Morrill, C.; Morrill, J. Internal auditors and the external audit: A transaction cost perspective. Managerial Auditing Journal 2003, 18, 490–504. [Google Scholar] [CrossRef]

- Mubako, G.; Muzorewa, S.C. Interaction between internal and external auditors—insights from a developing country. Meditari Accountancy Research 2019, 27, 840–861. [Google Scholar] [CrossRef]

- Munro, L.; Stewart, J. External auditors’ reliance on internal auditing: further evidence. Managerial Auditing Journal 2011, 26, 464–481. [Google Scholar] [CrossRef]

- Mustapha, M.; Lee, Y.K. Sourcing arrangement of internal audit services: does it matter to the external auditors. International Journal of Business Continuity and Risk Management 2020, 10, 99–111. [Google Scholar] [CrossRef]

- Noh, M.; Park, H.; Cho, M. The effect of the dependence on the work of other auditors on error in analysts’ earnings forecasts. International Journal of Accounting and Information Management 2017, 25, 110–136. [Google Scholar] [CrossRef]

- Oussii, A.A.; Boulila Taktak, N. Audit report timeliness: Does internal audit function coordination with external auditors’ matter? Empirical evidence from Tunisia. EuroMed Journal of Business 2018, 13, 60–74. [Google Scholar] [CrossRef]

- Page, M.J.; McKenzie, J.E.; Bossuyt, P.M.; Boutron, I.; Hoffmann, T.C.; Mulrow, C.D.; Shamseer, L.; Tetzlaff, J.M.; Akl, E.A.; Brennan, S.E.; et al. The PRISMA 2020 statement: an updated guideline for reporting systematic reviews. BMJ 2021, 372, 1–9. [Google Scholar] [CrossRef]

- Pahlevan-Sharif, S.; Mura, P.; Wijesinghe, S.N. A systematic review of systematic reviews in tourism. Journal of Hospitality and Tourism Management 2019, 39, 158–165. [Google Scholar] [CrossRef]

- Petherbridge, J.; Messier, W.F. The impact of PCAOB regulatory actions and engagement risk on auditors’ internal audit reliance decisions. Journal of Accounting and Public Policy 2015, 35, 3–18. [Google Scholar] [CrossRef]

- Pike, B.J.; Chui, L.; Martin, K.A.; Olvera, R.M. External Auditor’s Involvement in the Internal Audit Function’s Work Plan and Subsequent Reliance Before and After A Negative Audit Discovery. Auditing: A Journal of Practice & Theory 2016, 35, 159–173. [Google Scholar] [CrossRef]

- Pizzini, M.; Lin, S.; Ziegenfuss, D.E. The Impact of Internal Audit Function Quality and Contribution on Audit Delay. Auditing: A Journal of Practice and Theory 2015, 34, 25–58. [Google Scholar] [CrossRef]

- Prawitt, D.F.; Sharp, N.Y.; Wood, D.A. Reconciling archival and experimental research: Does internal audit contribution affect the external audit fee? Behavioral Research in Accounting 2011, 23, 187–206. [Google Scholar] [CrossRef]

- Prawitt, D.F.; Smith, J.L.; Wood, D.A. Internal audit quality and earnings management. The Accounting Review 2009, 84, 1255–1280. [Google Scholar] [CrossRef]

- Public Company Accounting Oversight Board (PCAOB). An audit of internal control over financial reporting that is integrated with an audit of financial statements. PCAOB Release No. 2007–005, Washington, DC. 2007. [Google Scholar]

- Public Company Accounting Oversight Board (PCAOB). AS 2605: Consideration of the Internal Audit Function. PCAOB Alert No. 11, Washington, DC. 2013. [Google Scholar]

- Quick, R.; Henrizi, P. Experimental evidence on external auditor reliance on the internal audit. Review of Managerial Science 2019, 13, 1143–1176. [Google Scholar] [CrossRef]

- Rabóczki, M. B. “Internal audit functions and corporate governance: Evidence from Hungary”. Society and Economy 2018, 40, 289–314. [Google Scholar] [CrossRef]

- Roussy, M. , & Perron, A., New Perspectives in Internal Audit Research: A Structured Literature Review. Accounting Perspectives 2018, 17, 345–385. [Google Scholar] [CrossRef]

- Saidin, S.Z. Does Reliance on Internal Auditor’s Work Reduced the External Audit Cost and External Audit Work? Procedia - Social and Behavioral Sciences 2014, 164, 641–646. [Google Scholar] [CrossRef]

- Schneider, A. Modeling external auditors’ evaluations of internal auditing. Journal of Accounting Research 1984, 657–678. [Google Scholar] [CrossRef]

- Schneider, A. The reliance of external auditors on the internal audit function. Journal of Accounting Research 1985, 23, 911–919. [Google Scholar] [CrossRef]

- Schneider, A. Analysis of professional standards and research findings to develop decision aids for reliance on internal auditing. Research in Accounting Regulation. 22 2010, 96–106. [Google Scholar] [CrossRef]

- Soh, D.; Martinov-Bennie, N. Internal auditors’ perceptions of their role in environmental, social, and governance assurance and consulting. Managerial Auditing Journal 2015, 30, 80–111. [Google Scholar] [CrossRef]

- Speklé, R. F.; van Elten, H. J.; Kruis, A. M. Sourcing of internal auditing: An empirical study. Management Accounting Research 2007, 18, 102–124. [Google Scholar] [CrossRef]

- Stefaniak, C.M.; Cornell, R.M. Social identification and differences in external and internal auditor objectivity. Current issues in auditing 2011, 5, 9–14. [Google Scholar] [CrossRef]

- Stefaniak, C.M.; Houston, R.W.; Cornell, R.M. The effects of employer and client identification on internal and external auditors’ evaluations of internal control deficiencies. Auditing: A Journal of Practice & Theory 2012, 31, 39–56. [Google Scholar] [CrossRef]

- Suh, I.; Masli, A.; Sweeney, J.T. Do Management Training Grounds Reduce Internal Auditor Objectivity and External Auditor Reliance? The Influence of Family Firms. Journal of Business Ethics 2020, 173, 205–227. [Google Scholar] [CrossRef]

- Suwaidan, M.S.; Qasim, A. External auditors’ reliance on internal auditors and its impact on audit fees: An empirical investigation. Managerial Auditing Journal 2010, 25, 509–525. [Google Scholar] [CrossRef]

- Swanger, S. L.; Chewning, E. G., Jr. The effect of internal audit outsourcing on financial analysts’ perceptions of external auditor independence. Auditing A Journal of Practice & Theory 2001, 20, 115–129. [Google Scholar] [CrossRef]

- Tagesson, T.; Eriksson, O. What do auditors do? Obviously, they do not scrutinize the accounting and reporting. Financial Accounting & Management 2011, 27, 272–285. [Google Scholar] [CrossRef]

- Tuluk, F. Collateral Misrepresentation, External Auditing, and Optimal Supervisory Policy. Open Economies Review 2021, 32, 975–1016. [Google Scholar] [CrossRef]

- Weisner, M.; Sutton, S. When the World isn’t always Flat: The Impact of Psychological Distance on auditors’ Reliance on Specialists. International Journal of Accounting Information Systems 2015, 16, 23–41. [Google Scholar] [CrossRef]

Figure 1.

Conceptual Framework. Source: The authors adapted the framework from the literature.

Figure 2.

PRISMA chart of systematic review procedure .

Table 2.

SLR Procedures using PRISMA schedule.

| No. | Procedure | Papers regarding “External Auditing Reliance and IAF” published between 1984 and 2022 |

|---|---|---|

| 1. | Searching criteria with “keywords” | External auditing reliance, reliance decision, internal audit function. |

| 2. | Choose databases and conduct searches | Google Scholar, Scopus, and Web of Science. |

| 3. | Selected documents | English-language publications, in trustworthy sources, and included big data analysis and financial auditing. |

| 4. | Combine resources | Evaluation of the listed publications thoughtfully. |

| 5. | Advertise review outcomes | Results are based on the compilation of information or the most recent evidence from the results of multiple independent studies, which can help with practices based on proof. |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.