Submitted:

01 May 2023

Posted:

02 May 2023

You are already at the latest version

Abstract

The textile and clothing (T&C) industry is not usually viewed as an exemplar of sustainable de-velopment and the circular economy, as the industry has hitherto made its products in linear fashion, with relatively little recycling of the finished goods. This article examines the industry’s approach to the core sustainability concept and the circular economy in particular, through a re-view of the available academic literature, evidence from corporate sustainability reports and websites, and feedback from an online survey of industry professionals. The role of digital technology deployment in engendering sustainability and the circular economy in the industry is also explored. The study finds that whilst sustainability is now firmly embedded at the strategic level in the vast majority of companies studied, attitudes towards the circular economy remain fickle. The use of digital technologies in support of sustainability objectives is also limited at present, but the article concludes that the need to meet compliance requirements and new cus-tomer perceptions of sustainability will speed the transition to circular economy activities, facili-tated by greater exploitation of digital technologies. Building upon the research findings, existing models and an initial conceptual framework, a simple operational model for initiating such a transition for small-to-medium sized enterprises in the T&C industry is put forward.

Keywords:

textile industry

; clothing industry

; sustainable development

; circular economy

; CE

; digital technology

; digitalisation

; corporate social responsibility

; CSR.

1. Introduction

The global textile and clothing (T&C) industry is the fourth largest consumer of primary raw materials and water after the food, housing and transport industries, and the fifth largest producer of greenhouse gas emissions [1]. Less than 1% of all textiles worldwide are recycled into new textiles, and it is thus appropriate that the industry has a pivotal role in the European Commission's Action Plan for the Circular Economy. The Action Plan aims to change the way products are designed, produced and consumed by focusing on several key sectors such as textiles for the promotion of the circular economy (CE) which has been defined by the European Union [2] as an “economy where the value of products, materials and resources is maintained in the economy for as long as possible, and the generation of waste minimized“ (p. 2). According to some authors, this contrasts with the traditional linear economy, which leads to pollution and depletion of natural resources. Alonso-Muñoz et al. [3], for example, conclude that “the circular economy represents a further step forward in the field of sustainability by breaking with the linear production model, with substantial modifications in both operations and relationships”(p. 2).

A number of factors have contributed to the growing focus on the importance of adopting CE practices and business models: the continuing depletion of scarce natural resources, the unpredictable events associated with climate change, and the increasing introduction of national and international legislation designed to reduce environmental problems, are all important drivers of the CE. Indeed, the Action Plan referred to above is one of the key building blocks of the European Green Deal, the new European agenda for sustainable growth, and as part of this, the EU intends to rely on “innovative models based on a closer relationship with customers, mass customisation, the sharing and collaborative economy, and powered by digital technologies, such as the internet of things, big data, blockchain and artificial intelligence” [4] (p. 2). The strategies and measures of the Action Plan will challenge the European T&C industry, which is dominated by small to medium-sized enterprises (SMEs), to adapt processes and products to support a transition to a CE [5].

The overall aim of this article is thus to examine how the industry views sustainability and what measures it is taking to move towards the CE. The links between the CE and the transition to a sustainable future are complex, with several sources suggesting that digital technologies may play a key role in this transition [6,7]. The World Economic Forum [8] (para. 1) claimed “we must accelerate the transformation to a circular economy in order to meet global climate goals by 2050”, and that “this can only be achieved through focused and responsible digitalization”, and Kottmeyer [9] (p. 17) argued that “digital technologies have the potential to close the realisation gap between theory and practice of the circular economy concept”. Ranta et al. [10] (para. 1) point out the limitations of relevant research to date, claiming it mainly concerns “conceptual and review studies”, and that there remains “a lack of understanding of how digital technologies enable individual firms in real-life settings to improve their resource flows and value creation and capture, and thereby enable business model innovation to emerge”. This article has six main sections. Following this introduction, relevant literature is reviewed, a top line conceptual framework is set out and three research questions are posed. The research methodology is then discussed. This is followed by the main research results and a discussion of the key emergent themes, in which a simple model for initiating a transition to the CE for SMEs in the T&C industry is presented. The concluding section provides a research summary and offers some thoughts on possible areas for future research in this field.

2. Literature Review

2.1. The European Textile and Clothing Industry

The demand for textiles has grown exponentially over the last few decades, which has led to a globally interconnected and complex T&C industry, in which the EU has taken a central role as an importer and end-user [11]. Rising demand and international competition have accelerated the pace of new fashion collections, and value chains have become more efficient by using low-tech systems and low-cost materials, and by outsourcing production processes to low-wage countries. This has made textile products increasingly affordable, further fueling demand. While value creation within the EU is mainly concentrated in product development, marketing and supply chain management [12,13], globally interconnected production processes create wider implications for both humans and the environment, including the intensive use of land and water, greenhouse gas emissions, and air, soil and water pollution [13]. This has made the T&C industry a key focus of the EU's new Industrial Strategy for Europe and the European Circular Economy Action Plan [4,14].

In its “Strategy for Sustainable and Circular Textiles” [15], the European Commission sets ambitious targets for the T&C industry. For example, by 2030, all textile products on the European market should be durable and recyclable, consist largely of recycled fibres and be manufactured in compliance with environmentally and socially sustainable conditions. In addition, the European textile sector should remain economically competitive, resilient and innovative, while assuming responsibility for its products along the entire value chain, which also includes use and disposal of these products. Within the textile sector, the fashion industry represents the largest sub-sector, being one of the most globalised linear value chains [16]. The EU strategy for sustainable and circular textiles suggests a range of measures for transforming the existing linear model into a circular one. These measures include mandatory eco-design requirements, preventing the destruction of unsold or returned textiles, tackling microplastics pollution, and extended producer responsibility for reuse and recycling of textile waste.

It is evident that such a transformation requires a fundamental cultural and structural reorientation of the entire linear value chain from product development to manufacturing, use and disposal, through the development of new business models and the use of innovative technologies, involving all relevant internal and external stakeholder groups [15,17,18,19,20,21]. This will inevitably be a complex process, interweaved with other corporate strategic objectives. However, many companies remain uncertain as to how to initiate and implement such a transformation, which is increasingly required by new European laws and standards. The challenge for the industry, which contains many SMEs, is to transition to sustainable and circular business practices, whilst remaining profitable in an increasingly competitive sector.

2.2. Sustainability and the Circular Economy

The most widely used definition of “sustainability” is development "that meets the needs of the present without compromising the ability of future generations to meet their own needs" [22] (p. 16), where such development is in harmony with the natural environment. In recent years, the concept has also been steadily gaining importance in the corporate context [23]. Based on the triple bottom line, as put forward by Elkington [24], the view has prevailed that to be fundamentally sustainable in the long term, an organisation must consider all the contexts in which it operates. This includes the three dimensions of sustainability: social, ecological and economic, often also referred to as people, planet, and profit [25]. The economic dimension considers the efficient use of tangible and intangible resources to ensure the long-term survival, competitiveness, and resultant benefits to a company; the ecological dimension focuses on the natural environment and concerns the availability, use, and treatment of natural resources; and the social dimension focuses on human well-being, society, inter-societal relations, and fairness. Sustainability is therefore a holistic construct that must be anchored in corporate strategy and the business model, and must be linked to corporate culture, processes and activities [25,26,27]. At the same time, sustainability can best be assessed within the value chain within which an organisation operates, thus encompassing the entire supply network and incorporating upstream and downstream supply chain processes [28].

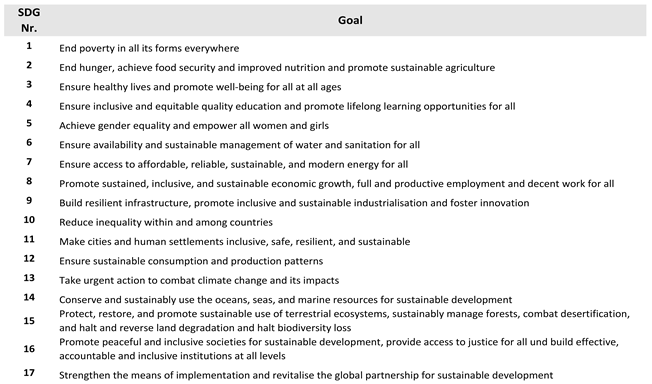

In developing their sustainability strategies and policies, many companies referred to the UN Sustainable Development Goals (SDGs), which came into effect in January 2016, and have been described by the United Nations [29] as the “2030 Agenda for Sustainable Development”, which is designed to “shift the world on to a sustainable and resilient path” (para.1). The European Commission [30] argued that “the 2030 Agenda integrates in a balanced manner the three dimensions of sustainable development – economic, social and environmental” (para. 6), and in the context of the industrial sector, PricewaterhouseCoopers [31] commented that with the advent of the SDGs “sustainability is moving from the corporate side-lines into the mainstream” (p. 6). Recent research [32] found that the three most referenced SDGs in company reports across a range of industry sectors were SDGs 8, 12 and 13 (Table 1). All the SDGs have associated targets, and for every target, there are one or more “indicators”, there being 241 in all [33].

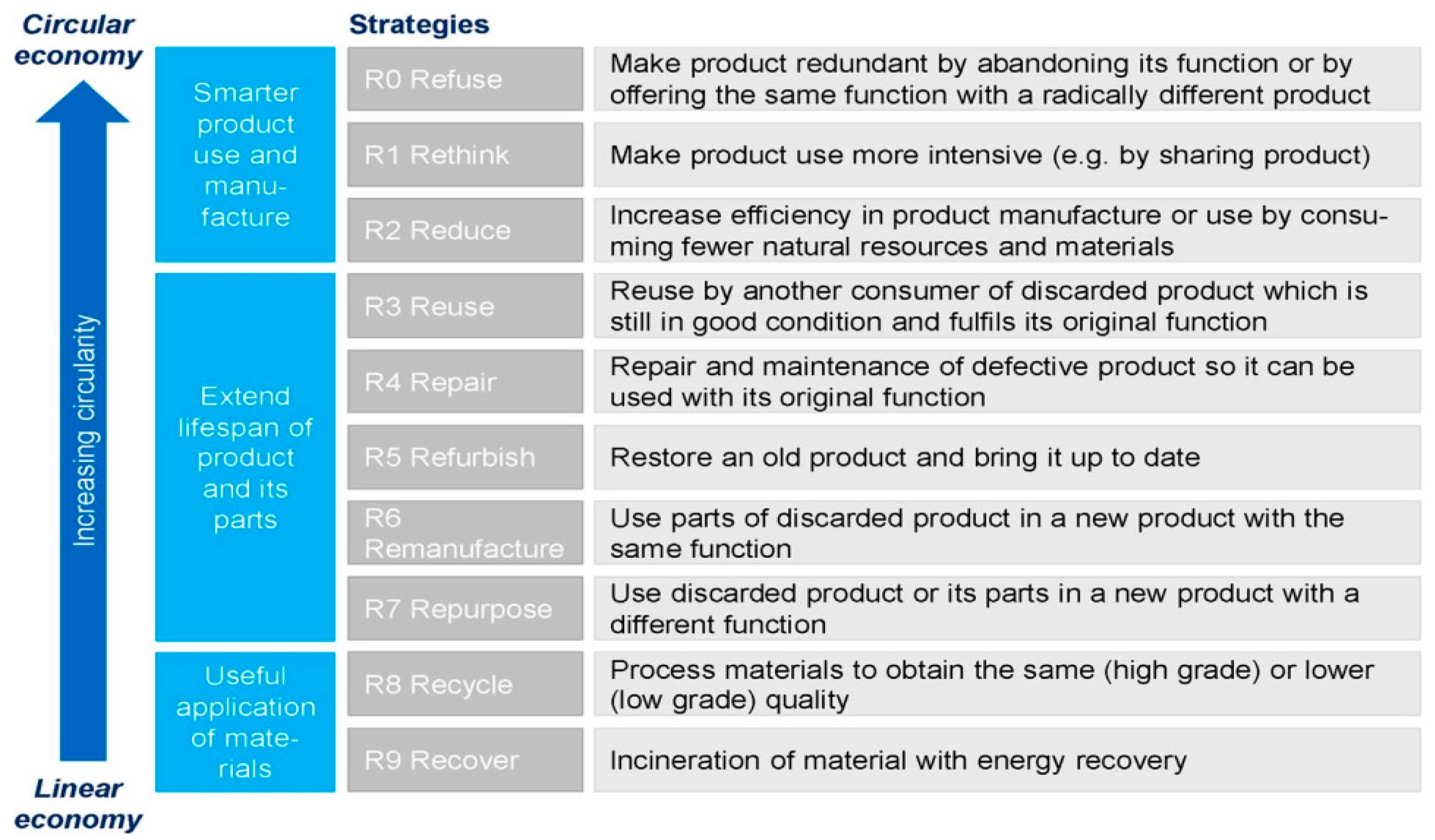

Within the wide definition of sustainability, the concept of the CE is increasingly being viewed as a key lever to effect the transition to a more sustainable future. It is of interest and relevance to both academics and practitioners as it offers principles and approaches regarding how companies can implement sustainability [20,35]. In its most basic form, “a circular economy can be loosely defined as one which balances economic development with environmental and resource protection” [36] (p. 373), and the Ellen McArthur Foundation suggest that a CE is “restorative and regenerative by design, and aims to keep products, components, and materials at their highest utility and value at all times” [37] (p. 46). In similar vein, the CE has been defined by the European Union as an “economy where the value of products, materials and resources is maintained in the economy for as long as possible, and the generation of waste minimized“ [2] (p. 2). The CE concept encompasses all stages of the product life cycle from product design and production, through marketing and consumption to waste management, re-use and recycling. A lasting transition to a CE will require radical changes in product development and manufacturing but also in consumer buying and consumption practices. The prevention, reuse and recycling of waste materials means that waste management becomes an opportunity to return as much waste as possible back into productive use. Consequently, companies need to extend their focus on the use phase and the end-of-life treatment of their products. This requires new and innovative business models, products and processes that build upon the CE principles - often referred to as R-principles [35] (Figure 1) - and which create sustainable value for the company and all stakeholders [38]. Geissdoerfer et al. [39,40] refer to business model innovation as a key tool for implementing CE in organisations.

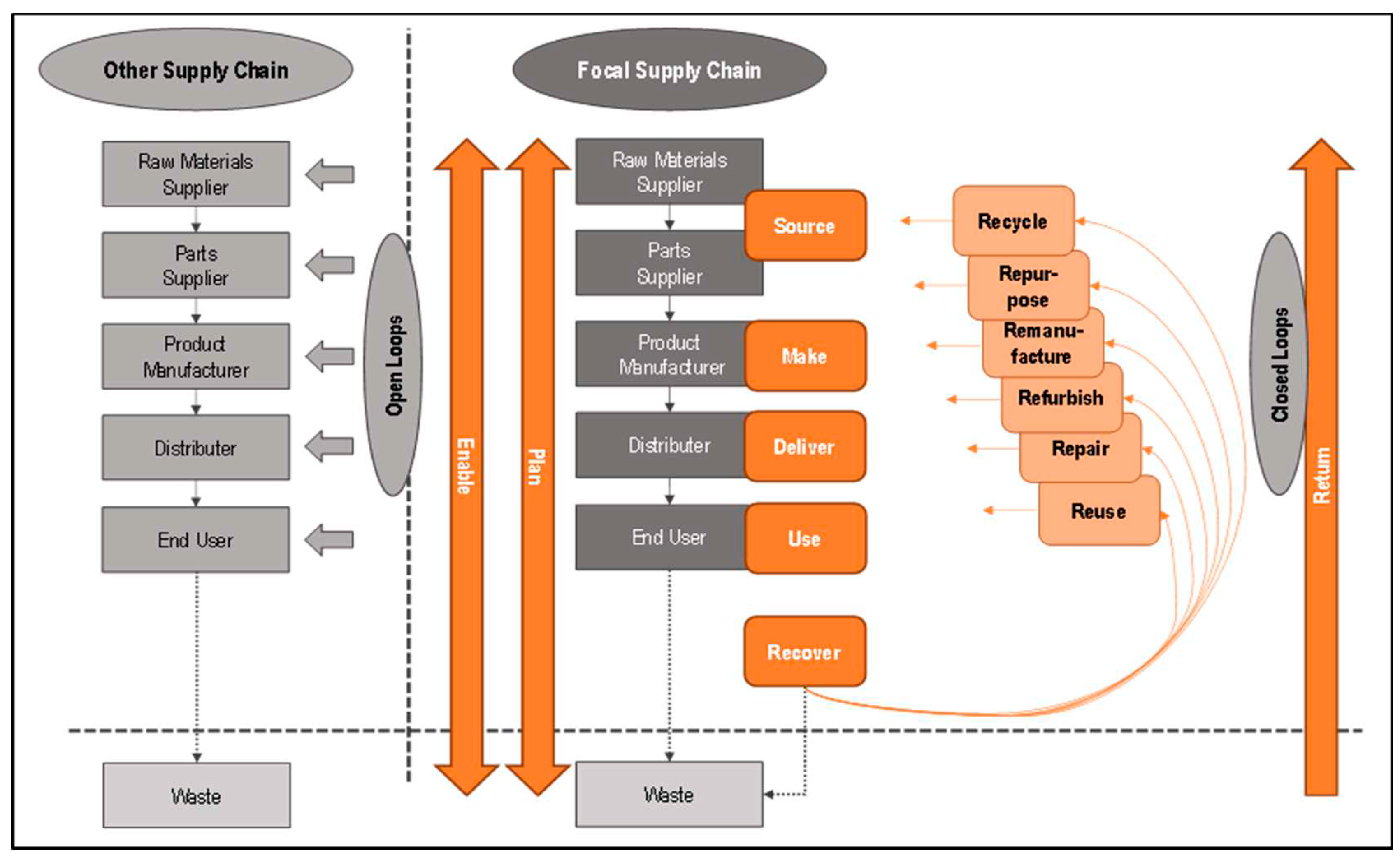

In today's economy, which is characterised by a global division of labour and outsourcing, a sustainable CE can only be implemented through joint, coordinated strategies and practices within supply chain networks [41,42]. As Brown et al. [43] conclude, well-founded partnerships and functioning collaboration are key success factors for circular oriented innovation. According to Geissdoerfer et al. [39], network infrastructure and capabilities of the supply chain play a critical role in enabling circular business models and Montag et al. [44] refer to the holistic integration of circularity into supply chain management as the enabler of circular business models. Montag et al. [44] present a circular supply chain maturity model, according to which changes are needed at the strategic, tactical and operational levels to move from a linear to a circular supply chain. First, it requires a paradigm shift within an organisation to ensure that the CE principles are incorporated into the long-term strategy and all activities necessary to implement it. At the tactical level, the authors focus on the product and its life cycle, arguing that changes are needed at all stages, from product development to use, disposal and recycling, to make the linear supply chain more circular. At the process level, the authors refer to the Supply Chain Operations Reference (SCOR) model [45], adapted for circular supply chains, and illustrate that the majority of the eight SCOR processes need to be completely redesigned with the goal of closing the product and material loops.

It is clear here that the first two levels refer to the company and its management. The model suggests that the alignment of an organisation´s strategy, business model, and product/service portfolio towards the CE is a prerequisite for implementing CE principles at the operational level. The company's internal strategic and tactical decisions are thus drivers to implement changes in internal processes and along the supply chain. The redesign of supply chain processes is therefore essential for CE implementation. As a result, the supply chain is the key to achieving circularity at corporate level.

In this context, Montag and Pettau [46] provide “a theoretical and conceptual approach for measuring supply chain performance in the circular economy era” based on the SCOR model adapted for circular supply chains (CSC). The authors maintain the model “provides a comprehensive composition of indicators to holistically measure the supply chain’s performance from an economic, environmental, social, and circular perspective” (p. 1). The framework (Figure 2) not only includes the three traditional dimensions of sustainability – economic, environmental and social – but also the new circular perspective of performance “thus reconciling the goals of sustainability and circularity” (p. 2). Their research also distinguished between the environmental and circular perspectives which may have conflicting goals. “While the CE aims for keeping products, components and materials in circulation for as long as possible and with highest value as possible through strategies such as reuse and recycling, environmental sustainability’s goal is to reduce the harm on the earth’s ecosystem by reducing waste and other negative outputs, such as CO¬2 emissions” (p. 5). Based on adapted SCOR processes for circularity, the framework “provides a horizontally integrated composition of performance measures to comprehensively assess the CSC’s performance from an economic, environmental, social and circular perspective”, thereby “enabling a clarification for the complex relationship between circularity and sustainability” (p. 9).

2.3. Digital Technologies and the Circular Economy

In recent years, digital technology and CE concepts have attracted growing interest in both the business and the academic communities, and a number of recent papers provide different perspectives on the relationship between the two concepts. Many of the early models and frameworks of digitalisation focused on the emergence of the technologies and their impacts on processes and organisational structure, possibly resulting in new business models [47]. More recently, Lang [48] identified sustainability as a driver of digital transformation and product transformation as one of its four key pillars, illustrating the relationships between sustainability, the CE and digitalisation.

Digital technologies can be defined as electronic tools, automated systems, and technological devices that allow very large amounts of data to be processed, transmitted and stored [7] (p. 1). Two acronyms are often used as generic terms to encapsulate these technologies: SMAC (Social Media, Mobile, Analytics/Big Data, Cloud) and BRAID (Blockchain, Robotics, Artificial Intelligence/Knowledge Work Automation, Internet of Things and Digital Fabrication). Some authors specify some of these technologies as being of particular significance in promoting and supporting the CE. Frost & Sullivan [49], for example, highlight the significance of IoT devices, robotics and mobile applications, acting in combination with analytical tools and optimisation software. Reuter [50] argued that IoT can help promote the CE in the metallurgy industry by providing dynamic feedback control loops, whilst Salminen et al. [51] maintain that IoT enables the improved management and analysis of data coming from various sources “to enhance services provision and the co-evolution of the circular economy” (p. 21). In similar vein, Bressanelli et al. [52] explored how IoT, big data, and analytics, can support a transition to a CE. They identified eight specific functionalities, which were seen to be important in the transition process: improving product design, attracting target customers, monitoring and tracking product activity, providing technical support, providing preventive and predictive maintenance, optimising product usage, upgrading the product, and enhancing renovation and end-of-life activities. Owen-Jackson [53] observed that “Internet-connected sensors can track the location, condition, and availability of assets in a supply chain. Direct exchange of information via secure, decentralised channels like blockchain can keep these communications secure. Together, these innovations can optimise resources, extend lifecycles, and help regenerate natural resources” (para. 10). Owen-Jackson [53] also points out that digital technology “helps support dematerialization by reducing our reliance on physical resources – e.g., retailers selling e-books directly to consumers or digital video and audio being delivered online rather than through physical media” (para 14).

For manufacturing companies this requires changes in their business models towards a “Product/Service-Systems” (PSS) model, as noted by Pagoropoulos et al. [54]. It entails a “shift from selling just products to selling the utility, through a mix of products and services while fulfilling the same client demands with less environmental impact” (p. 19). The authors found that digital technologies have often underpinned the move to a PSS business model with considerable economic, environmental and societal benefits. Ranta et al. [10] conducted a multiple case study of CE business models enabled by digital technologies, using interviews and document data from four innovative Northern Europe-based companies. The authors identified “four key types of business model innovation for CE that is catalysed by digital technologies and vary in incremental and radical improvement to the resource flows, value creation, and capture” (p. 2). Antikainen et al. [55] also suggest that digitalisation can been seen as one of the enablers of the CE by building visibility and intelligence into products, indicating location, condition and availability of assets.

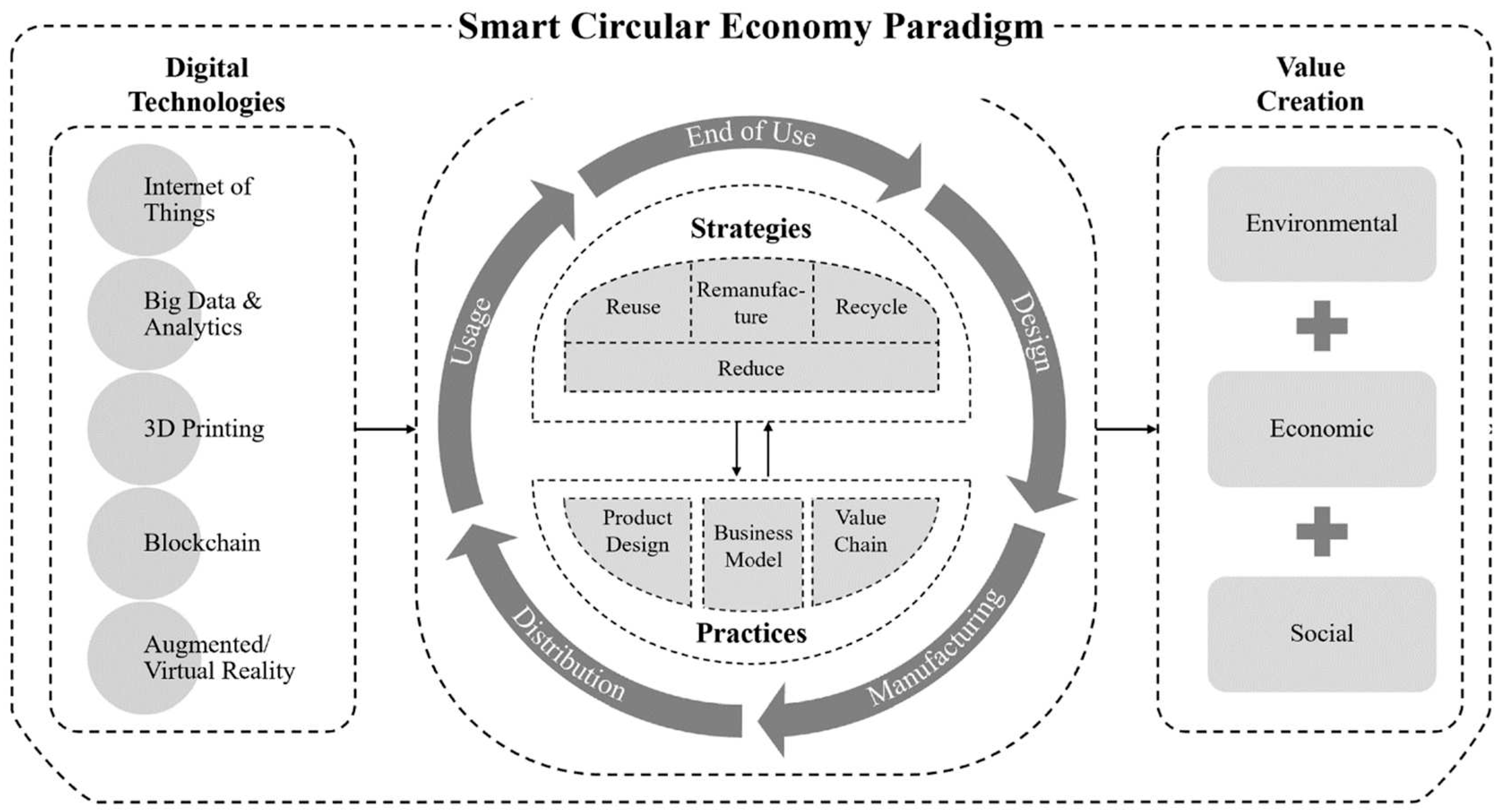

Some researchers have looked beyond individual company environments to consider these concepts across supply chains. Del Giudice et al. [56], for example, analysed the effect of CE practices on firms’ performance for a circular supply chain. Using data collected through an online survey distributed to managers of 378 Italian companies that had adopted CE principles, the authors found that in designing and promoting CE initiatives, companies must build value-added relationships by exploiting big data, which will stimulate both management and employees to adopt a collaborative approach. Bressanelli et al. [57] take a different approach in putting forward a framework (Figure 3) that “shows the linkages between digital technologies, circular strategies and practices, and sustainability performance” (p. 9). The authors conclude that digitalisation “enables a systemic redesign of products, business models, and value chains, impacting all the life-cycle phases of products to reduce material and energy consumption, reuse products, remanufacture components, and recycle materials”, and that this promotes “the achievement of enhanced sustainability performance in terms of environmental, economic, and social benefits” (p. 10).

Other authors have found only a limited exploitation of digital technologies in support of the CE. In exploring digitalisation as an enabler of a sustainable CE in Germany, Neligan [58] analysed data from 600 manufacturing companies and found that traditional efficiency raising measures that optimise manufacturing processes are still predominant in the manufacturing sector, but that “the opportunities offered by digital networking for increasing material efficiency are only used to a limited extent” (p. 106). Wynn and Jones [59] interviewed senior IT executives in eight European organisations and found that, although all organisations were pursuing activities to engender the transition to a CE, there was very little direct linkage to digital technology deployment. Digital technologies were nevertheless used by all these organisations, who saw more general benefits in terms of cost savings and efficiency gains that acted also in support of sustainability objectives, but not specifically for this purpose or in support of the CE. Cagno et al. [60] also noted that digitisation and sustainability have so far been considered separately. They adopted the ReSOLVE framework, developed by McKinsey, to assess linkage between digital technologies and the CE. They noted the lack of an integrated and holistic analysis of the relationship between the two concepts and highlighted the need to investigate both decision-making processes and specific CE practices, from an empirical perspective. Montag and Pettau [46] point out that “future research opportunities lie in the adoption of a digital performance perspective, depicting the impact of digital technology on the CSC performance” (p. 10). Overall, to date, literature on how digital technologies enable and support the CE across supply chains remains scarce [61].

2.4. Conceptual Framework and Research Questions

A conceptual framework can be seen as a network of interlinked concepts that together represent an overview of the phenomenon being studied [62], often in the form of a top-level map of the research area, providing the basis for subsequent analysis and model development [63]. Elaboration of the conceptual framework helps the researchers focus on the key aspects of the research area in a textual or visual “big picture” [64] (p. 15).

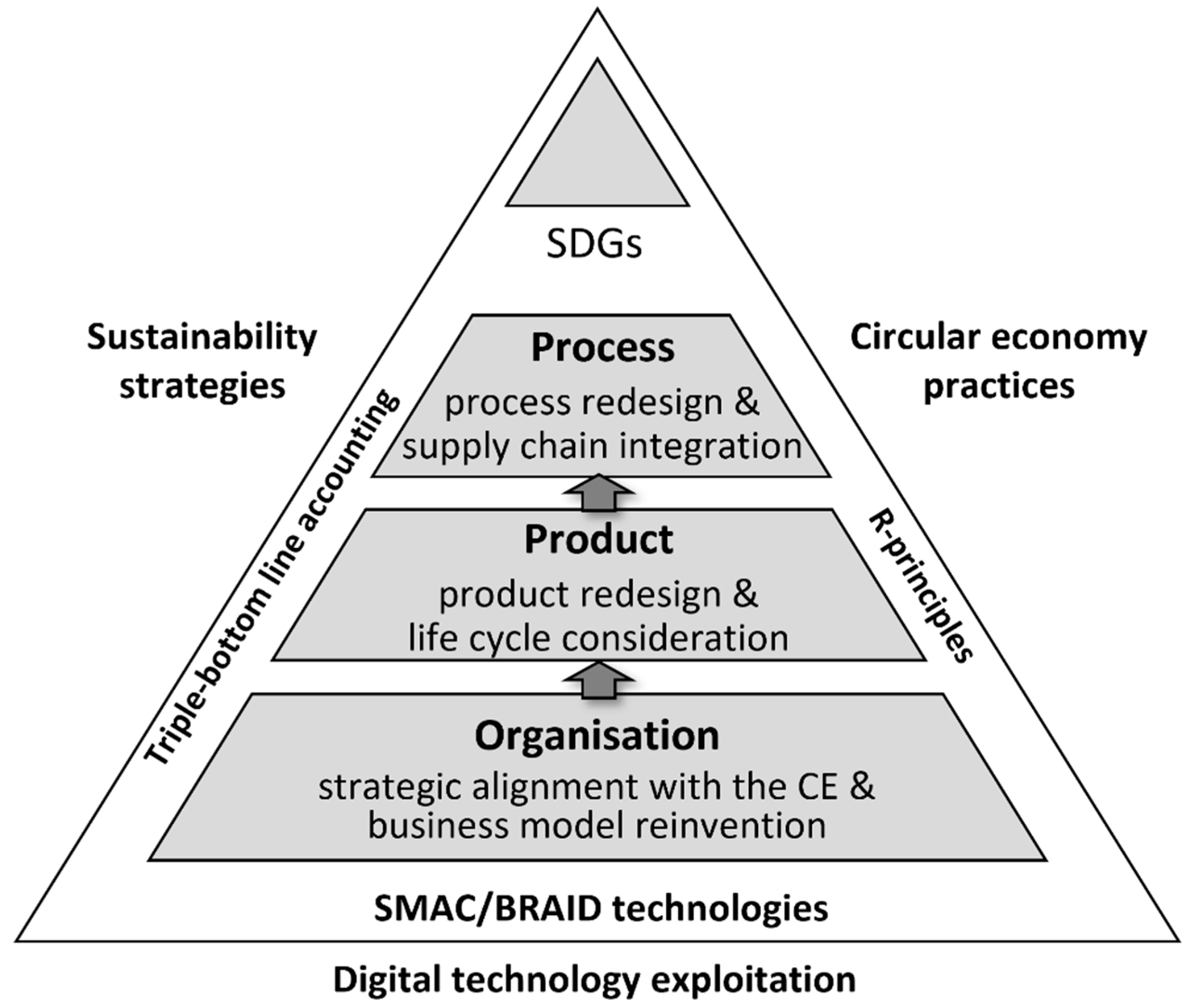

To transition to a sustainable and circular textile industry, the literature suggests there are three main conceptual areas of relevance: first, adoption of sustainable business strategies by alignment with triple bottom line accounting and the UN Sustainable Development Goals; second, migrating to CE practices by consistently following the R-principles that conserve resources and reduce waste and pollution; and third, the potential of digital technologies to act as a catalyst and driver for transition, which requires a coordinated and integrated approach involving holistic adjustments and changes within an organisation to the business model, products, and internal processes, as well as to cross-company processes along the entire supply chain (Figure 4). This builds upon the maturity model developed by Montag et al. [44], discussed above, which identified the three dimension of change - organisation, product and process - in transitioning to a circular economy.

To the authors’ knowledge, there are currently no models or frameworks for the transition to the CE in the T&C industry. This exploratory paper attempts to address this gap in the literature by building upon the conceptual framework outlined above. Available literature regarding the transformation towards a sustainable and circular T&C industry is very scarce and guidance for initiating such a transition is more or less non-existent. In this context, this paper examines how SMEs in the textile and apparel industry have approached sustainability and the CE to date and, more specifically, answers the following research questions (RQs):

- RQ1:

- How are German textile and clothing companies addressing sustainability in their corporate strategy and activities?

- RQ2:

- What strategies and activities relating to the CE are being pursued in the German textile and clothing industry?

- RQ3:

- What role are digital technologies playing in the transition to sustainability and the CE in the German textile and clothing industry?

3. Research Method

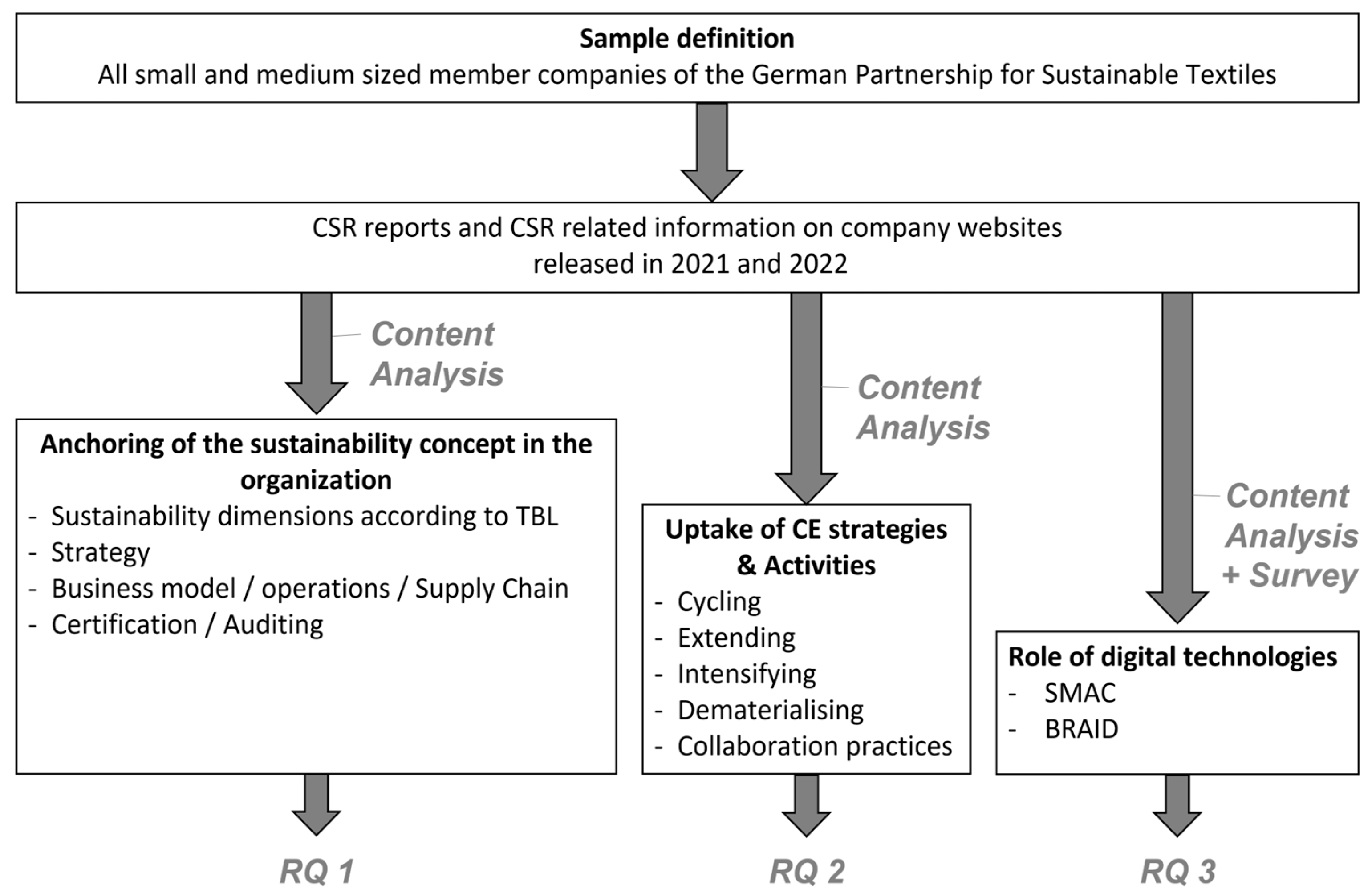

3.1. Sample Definition

The companies included in this research were systematically selected from the members of the German Partnership for Sustainable Textiles, a multi-stakeholder initiative consisting of companies and associations, non-governmental organisations (NGOs), trade unions, standard organisations, and the German government. The Partnership aims to enhance the state of global textile production, from raw material extraction to disposal. Of the 75-member companies (as of May, 2022), 29 were classified as SMEs as they had less than 250 staff and/or a turnover of less than 50m euros [65] (Table 2). Of these, 26 companies are headquartered in Germany, two are in the Netherlands and one in the UK. It is these companies that constitute the basic population for the study. The most recent corporate social responsibility (CSR) reports and sustainability related information for these companies were then searched for on their websites. CSR reports were available from 18 of these companies; for the remaining 11, some relevant information was found on the corporate websites. All the reports identified are in the public domain, and the authors took the view that they did not need to contact the selected companies or organisations to obtain formal permission prior to conducting their research.

3.2. Analysis Methodology

To answer the RQs noted above in section 2, the content of the CSR reports and corporate websites was analysed following Mayring’s [66] approach for qualitative content analysis. Regarding RQ3, it was observed that the CSR reports and company websites provided limited details about digital technology deployment. Consequently, an online survey consisting of three fundamental questions was circulated to the companies. Respondents were typically CEOs, COOs, sustainability managers and supply chain managers. The questions concerned the current and future use of digital technologies and their application within the company. This allowed an assessment of the technologies currently used (or to be used in the future), and supplemented material available from secondary sources. The online questionnaire responses reflected the view of just one individual in each company, and thus cannot be seen as a fully comprehensive analysis, but rather as a subjective snapshot of the current status quo and future possibilities in each company.

The research is mainly inductive but combines both qualitative and quantitative approaches. The analysis of CSR reports and websites follows a qualitative approach, whilst in the analysis of the questionnaire responses, a quantitative approach is pursued. The paper draws its empirical material from the CSR and related reports published by the German T&C SMEs mentioned above and from relevant academic papers. Saidani et al. [67] note that while corporate and industry body reports can be seen to “reflect current industrial reality and needs, and therefore bring meaningful insights”, the inclusion of peer reviewed academic papers “ensures scientific soundness” (p. 2).

The CSR reports were read and inductively coded in terms of their content related to the research questions (Figure 5). For RQ1, the passages containing information about the organisation´s strategy, business model, as well as specific operational practices and approaches regarding economic, environmental, and social aspects within the organisation, their products and along the supply chain, were identified and coded. For RQ2, passages which provide information relating to the CE - about the organisation´s strategy, business model and specific operational practices and approaches - were similarly identified and coded. For RQ3, passages containing information about the use and application of digital technologies in relation to sustainability or CE aspects, were located and coded. As the information from the analysed CSR reports and websites refers to the past and was found to contain little information about the current or future use of digital technologies, the authors additionally distributed an online questionnaire to the companies from the sample, as noted above. The aim of the online survey was to gain an overview of current and future developments in the companies regarding the use of digital technologies in connection with sustainability and CE aspects.

4. Results

Of the 29 SMEs studied, 28 companies have information on sustainability on separate landing pages on their websites. Only one company does not have a dedicated landing page for sustainability, but rather provides information on sustainability in a more general page on the company website. Of the 18 companies regularly publishing downloadable sustainability reports on their websites, 11 companies had published a sustainability report for 2021 (as of March 2022), four companies had published their most recent report in 2020, and for another two companies the last published CSR report was from 2019. The results below use the codes for each company shown in Table 2.

4.1. RQ1. How are German textile and clothing companies addressing sustainability in their corporate strategy and activities?Subsection

From an analysis of the above-noted reports and web sources, eight main themes emerged, providing an overview of how sustainability is addressed and implemented in these companies (Table 3).

4.1.1. Integration of sustainability into company culture and structure

The vast majority (93%) of the companies studied had departments with associated responsibilities for sustainability issues, which were also reflected in corporate values and culture. OR, for example, sees its culture as being characterised by a respectful community and relationships within the team, as well as with their customers and business partners. In similar vein, HK notes that “sustainability management is not just about questioning the use of resources, technology, and processes. It is also essential to involve and integrate the staff in the process” [68] (para. 1).

4.1.2. Adoption of the UN SDGs

Just under a third (31%) of the companies claimed an alignment with the UN SDGs. DS, for example, uses the SDGs as a guideline for structuring its sustainability activities, while HA relates all sustainability goals directly to the SDGs. Across the companies that reference the SDGs, SDGs 8, 12, 13 and 17 are seen as the most relevant, being supported through appropriate measures and policies. SDGs 7 and 16 are the least noted or overtly supported.

4.1.3. Cross-supply chain transparency

Transparency forms a fundamental prerequisite for sustainable procurement and production, and 93% of the companies studied noted this as a significant policy objective. This is of particular importance in the complex clothing supply chain, in which there is often no direct contractual relationship with the upstream stages of raw material extraction or fibre and fabric production and processing. These are therefore not subject to the terms and conditions of the direct contractual partners and in some cases are not even known. However, some companies are already taking measures to make the activities of all actors along the supply chain transparent, to enable the transition to a sustainable supply chain. SY, for example, states that “our direct business partners, particularly the small number of ready-to-wear companies, are amfori BSCI (Business Social Compliance Initiative) verified. Furthermore, we are intensively working on integrating the deeper supply chain (Tiers 2 and 3 […]) into the BSCI Audit process as well” [69] (p. 9). An alternative approach is taken by DI and ES, who prefer to work with vertically producing suppliers who have spinning, weaving, dyeing, and sewing under one roof. In this way, they can influence several supply chain stages and work with a manageable number of suppliers with the aim of long-term, trusting cooperation. Other companies (for example, ES) publish information about direct suppliers and production sites in public databases such as the Open Apparel Registry (OAR), or on the company website (for example, VO and SC). Transparency across the supply chain also allows more effective tracking. BR uses a digital tool to offer entire transparency about the origin and manufacturing of products. The tool allows consumers to track a product´s journey by entering a tracking code or scanning a QR code. Certain certificates such as the Green Button and Oeko-Tex Made in Green are intended to ensure compliance with minimum social and ecological standards in the manufacturing and sourcing processes.

4.1.4. Sustainability-related risk management

76% of the companies claimed to be adopting sustainability related risk management practices. HK assesses the level of the risk of suppliers and then sets certain requirements for working with them. The risk assessment identifies potential negative social and environmental impacts of products, relating to the materials used, the various processing steps in the supply chain, and overall complexity. This is in line with the OECD Due Diligence Guidance for Responsible Supply Chains in the Garment and Footwear Sector [70] which provides a structure for risk analysis. It describes various risks that are particularly relevant and specific to the textile sector, such as human rights violations through child and forced labour, working conditions or low wages, as well as environmental damage through hazardous chemicals, waste, and emissions.

4.1.5. Supplier selection and influence

Clothing manufacturers can influence the social and environmental impacts associated with the production of their products in emerging countries, where the raw materials are sourced and processed. All companies stated that they base their actions as well as their business relationships on a code of conduct, which is extended to partners in the supply chain and declared to be a prerequisite for business relationships. The code of conduct is normally based on internationally recognised principles and guidelines. For example, BI state that all their supplier relationships are based on the company’s code of conduct, which “precisely defines our due diligence requirements regarding ILO core labour standards, social and environmental standards and general aspects of responsible working relationships, such as the barring of corrupt practices” [71] (p 20). Subcontracting can undermine these practices as there is usually no direct supplier relationship with the subcontractors and therefore their practices cannot be controlled or influenced. To prevent this, subcontracting is prohibited by contract by some of the companies. To monitor compliance with social and environmental standards at the suppliers, companies either employ own staff in the production countries or rely on external support through audits and certifications. The companies rely on long-term supplier relationships and support them in implementing social and environmental standards. These standards and measures support the achievement of SDG 8 in the producing countries and are indirectly related to other goals, such as SDGs 1, 2 and 5.

4.1.6. Emissions and chemicals reduction

The reduction of climate-damaging emissions plays a major role in the sustainability reporting of all analysed companies. Measures to reduce the CO2 footprint are already being implemented. For example, at VO and SC, where emissions along the supply chain are monitored, reduction measures have been introduced. At SY and OR, ambitious targets have been set to further reduce emissions and achieve the goal of a climate-neutral supply chain by using innovative production processes and methods, which also help to reduce the use of resources and chemicals. ES was able to “reduce the use of water and chemicals in production [..] by printing more and more digitally rather than conventionally” [72] (p.30). SY reduced water and chemical consumption in dyeing by using spinneret dyeing technology instead of conventional dyeing processes. Suppliers are encouraged to implement responsible chemicals management and to avoid hazardous chemicals during the production process or in the end products. To minimise the impact of transportation, companies rely on sea and rail transport from the production countries to Europe instead of air freight. Distribution – for example from online shops to consumers - is carried out with more sustainable delivery services (e.g. BL, CH and VO). IV even offer emission-free delivery with cargo bikes or e-cars in many German cities. Other companies use sustainable packaging without plastics (LA) or made of recycled materials (OR). The measures mentioned here mainly contribute to environment-related SDGs, such as SDGs 13, 14 and 15.

4.1.7. Sustainable products and materials

Sustainability guidelines play an important role in minimising negative impacts in product development, notably in engendering the use of more sustainable materials, such as organic cotton, other plant-based fibres or innovative materials. All companies claimed to be pursuing such measures. For example, VO uses an innovative polyamide made from castor oil for fine tights. For synthetic materials, which are mainly used in functional and outdoor clothing, the focus is increasingly on recycled materials. Materials of animal origin are either completely avoided (BL and DE) or attention is paid to species-appropriate husbandry, by using certified materials such as mulesing-free wool (IV, OR and PA). Companies also focus on high-quality and durable products as well as repairability, "because wearing the clothes for longer can effectively reduce the ecological footprint of the products, which are costly to produce" [73] (p. 22). Even companies from the fashion industry, such as BL, GG and LA, rely on their products being durable and outlasting short-term fashion trends, through use of high-quality materials and timeless design. These measures can be seen to align with SDG 12 in particular.

4.1.8. Adopting sustainable business models

New or changed business models to achieve sustainability goals are mentioned by 41% of the companies studied. For example, several companies from the workwear, functional clothing and outdoor clothing sectors now offer repair and spare parts services to extend the lifetime of products (DS, OR and SC). Rental or leasing models are also being tested; OR for example, initiated a pilot project for clothing and backpacks rental in 2021, to save resources through the best possible utilisation of products. HA, on the other hand, has adopted a longer-term objective of analysing the options for a new integrated sustainable business model by 2030.

4.1.9. Other activities

Philanthropic activities include donations, sponsoring and “social” projects. For example, LO founded an association to help needy children in Romania, whilst ES donates 1% of turnover of a particular collection to social projects. Biodiversity is protected at company sites through the planting of flowering meadows (e.g., HA) or insect protection measures (BR). Employees at the head offices are offered job bikes and/or job tickets or healthy food and beverages, as well as sports activities.

Overall, the picture presented is of an industrial sector highly aware of sustainability issues, which are evidenced in strategies, policies, actions and culture. This is further discussed in section 5 below.

4.2. RQ2. What strategies and activities relating to the CE are being pursued in the German textile and clothing industry?

The CE is explicitly referred to by only 28% of the companies in their sustainability reporting as a core component of sustainability strategy. Although all companies are adopting some measures associated with the CE, they are presented as being supportive of a general move to sustainable practices, rather than specifically in the context of pursuing a CE based strategy. Seven sets of activities relating to the CE can be identified in the company reports studied (Table 4).

The reduction of emissions and waste in the production process was cited as a current activity by 97% of companies. Different approaches to waste prevention are in evidence. Post-production waste is sold to recycling companies (HK) or reused in new collections and products (IV). Pre-consumer waste such as defective or unsold products are offered at reduced prices through alternative channels such as outlet stores (VO) or, in the case of non-saleable products, are fed into downcycling processes as filling material for other industries (BL). OR has introduced various packaging measures, such as new folding techniques, eliminating or digitalising labels, hangtags and printed invoices, or using recycled packaging materials to reduce the use of plastics and other resources.

The use of recycled materials and the recycling of materials in production or packaging were noted by 90% of companies. The use of recycled materials refers primarily to synthetic fibres, which are made from PET bottles or marine waste, for example. True textile-to-textile recycling is evident only at pilot level. HA is participating in a pilot project in cooperation with a tech start-up, fashion brands, textile collectors and recycling companies to develop and test holistic processes from product development to recycling to create a “textile CE”. SY is pursuing a "zero-waste vision" in which the company intends to implement 100% recyclable products and processes by 2030 and is participating in various collaborations to this end. These include the Accelerating Circularity Project Europe (an NPO that develops and implements processes to achieve circular supply chains in conjunction with actors in the textile supply chain), and Wear2Wear (an association of industrial companies that want to produce new textiles exclusively from recycled and recyclable unmixed materials, and thereby develop processes and technologies for a closed textile cycle).

Just over a third of companies (34%) are involved in the production or sale of easily recyclable or biodegradable products. For example, BR and KA have developed product lines that are certified according to the Cradle2Cradle standard and can thus be (at least partially) returned to technical or biological cycles, whilst SY use mono materials for certain products that are thus 100% recyclable. Measures to extend the use phase of products, such as durable quality, repairability and repair services, were evident in 55% of companies.

Very few companies (24%) deal with the life cycle after sale of the products or packaging, i.e., the part of the supply chain that is essential to “close the loop”. There are some examples of reverse logistics processes or take-back schemes - either currently in operation or planned for the future - to receive used products or packaging back into the company for reuse or recycling. Over a third of the companies (38%) rely on cooperation and collaboration with other companies in the upstream or downstream value chain, or even competitors, for processes related to the CE. For example, BI work together with a supplier in a pilot project in which waste from production is passed on to a company that uses it to make new yarn. LA cooperates with the reselling platform Buddy&Selly, through which worn clothing can be resold and DI has founded the textile cooperative Cibutex together with partners and competitors, to collect and recycle worn-out business textiles.

4.3. RQ3. What role are digital technologies playing in the transition to sustainability and the CE in the German textile and clothing industry?

In just over half the companies considered (52%), reference is made to digitalisation or digital technologies in the CSR reports. A number of examples of how digital technologies are supporting sustainability or the CE are referred to in these reports or on the company websites. These are discussed below.

Digitalisation of operational and administrative processes can help reduce resource and materials consumption and emissions costs. HA reported on the transition to exclusively digital processes in the area of quality control: “Paperless working has the big advantage of information being available far more quickly and readily, also for communication with colleagues in other teams” [74] (p. 86). In light of the success of this initiative, the entire company is to switch to paperless processes wherever possible. ES plans to offer its regularly published book collection only digitally in the future in order to save paper. Another example is digital visualisation using 3D software to create prototypes and samples. BR reported that due to a true-to-the-original representation of the products through 3D visualisation, the company has reduced the costs of misunderstandings on the part of customers and suppliers and faults in production. The use of 3D software thus offers not only economic advantages, through the saving of resources, but also ecological benefits. BI also reported on the elimination of transportation and resource use to produce samples through 3D visualisation. VO consciously pursued an online-only sales approach to save costs and improve margins, allowing increased investment in responsible products and production processes. The high level of online meetings necessitated by the COVID-19 pandemic generally provided a positive experience with virtual meetings that will likely reduce face-to-face meetings in the future.

Supply chain and product transparency can be supported through digital product passports and tracing tools. As noted in section 4.1, digital tracing tools can provide cross-supply chain transparency for consumers. BI plans to introduce a digital product passport by 2025, in line with the recommendations of the EU Sustainable and Circular Textiles Strategy [15]. Other companies use product or QR codes and smartphone apps to provide consumers with information about their products, the supply chain and carbon footprint. BR additionally uses a digital tool to track and control chemical management in the supply chain. This allows the monitoring of chemicals used and their compliance with restricted substances lists.

The use of social media and other digital media technologies can enhance communication with external stakeholders such as suppliers, trade customers and consumers. At SC, for example, stakeholder communication is supported by digital media and product information. In addition, a supplier portal to connect with suppliers is to be implemented. HA is using social media channels such as Facebook, Twitter and Instagram not only for product communication, but also for building awareness in the area of sustainability and insights into the “company world”.

Except for HA, none of the companies cite digital technologies as a key component in the future achievement of sustainability goals. At HA, digitalisation of business processes is seen as the facilitator of service quality improvement, and digitalisation initiatives are underway in many areas of the company, impacting logistics, traceability in the supply chain, and building technology. The follow-up questionnaire, noted in section 3 above, was sent to the core population of the 29 companies in the period February to May 2022, there being 19 responses.

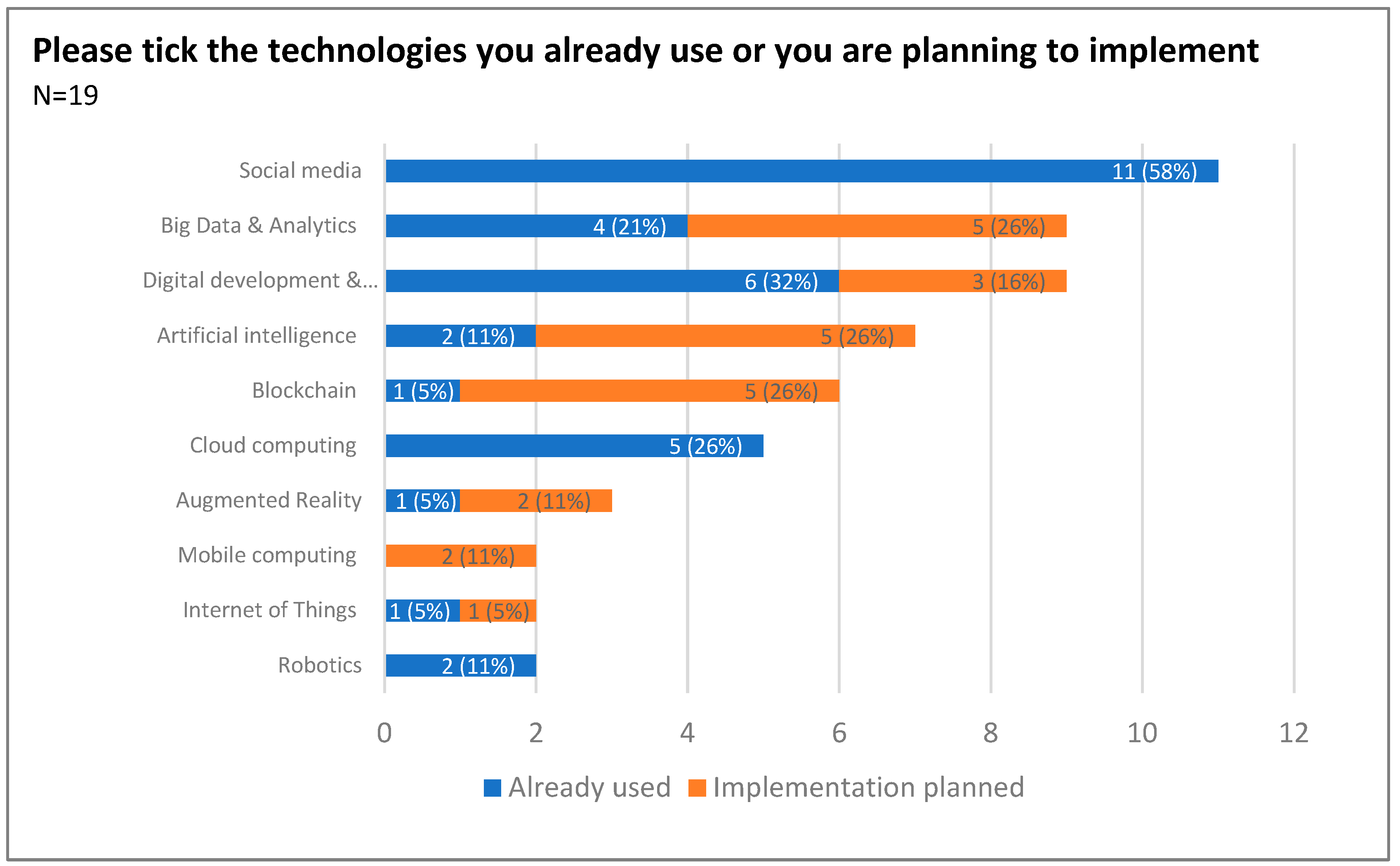

The questionnaire respondents indicated that the majority of companies were either currently using, or planned to use, the mainstream technologies – social media, big data and analytics, and digital manufacturing (Figure 6). Social media, as the CSR reports suggested, is mainly used for communication with stakeholders and for advertising purposes. Technologies used for digital product development and manufacturing included 3D design, 3D printing and CAD software, whilst big data and analytics applications provide customer and trend analysis, and demand forecasting and planning. It is somewhat surprising that no company is currently using mobile computing and only two companies are planning to introduce it. In the context of the COVID-19 pandemic and the associated lockdowns and home working activities, it can be assumed that companies were using mobile working options, but this seems to be seen as a temporary reaction to pandemic measures rather than as a long-term permanent working option.

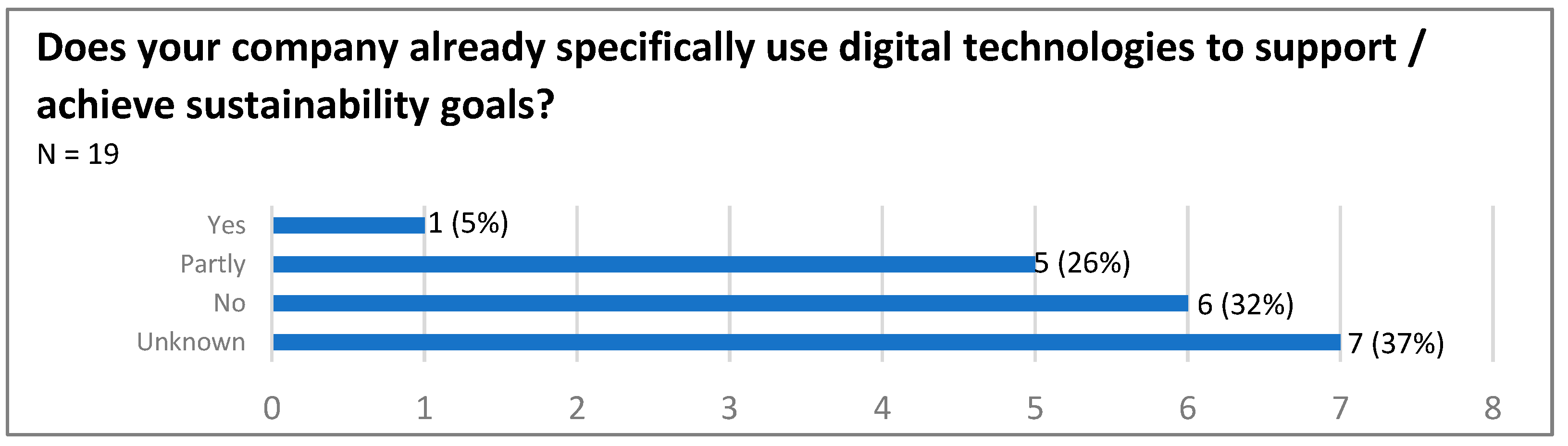

When asked specifically if these technologies were used to support sustainability goals, 6 respondents answered “yes” or “partly”, 6 answered “no”, with 7 “don’t know” replies (Figure 7). However, looking to the future, respondents suggested digital technologies would play a more significant role. Asked if digital technologies will play a key role in the transformation to the CE, 7 (37%) responded “yes” and a further 9 (47%) attributed at least a partial role to digital technologies in the transition to a sustainable and circular T&C industry. Only 3 (16%) of the 19 respondents answered this question with “no”. This is surprising insofar as this assessment has not yet been reflected in the CSR reports.

5. Discussion

The results outlined above raise a number of issues that merit further discussion.

Firstly, the CE is gradually emerging as a key strategic issue for companies in this sector, rather as sustainability in general has done over the past decade. Sustainability is now firmly anchored in the strategic goals of the majority of the companies that want to be perceived as responsible and sustainable and thereby develop and maintain competitive advantage. The CE is explicitly included in some company sustainability strategies, whilst other companies pursue measures and activities related to individual aspects of the CE in their general sustainability efforts but do not link these directly to strategic objectives. At present, the CE concept is not approached holistically, but rather individual aspects are integrated into the existing linear value creation processes and business models. For example, the reduction in the use of fossil energies and climate-damaging emissions plays a major role in all companies. However, the focus is on the emissions caused directly by the company, and only five of the 29 companies provide information on emissions that occur in the production processes of the upstream supply chain and measures to reduce them. It is also noteworthy that although the adoption of new digital business models to accommodate sustainable practices is mentioned by 41% of companies, there is no specific reference to the significance of the CE in such transitioning. This lack of connectivity between the two concepts is evidenced in a recent survey of global CEOs that found “84% of companies see digital and sustainability transformation as separate initiatives” [75] (para. 9). These inconsistencies and contradictions highlight the need for some underpinning theory and modelling linking digitalisation with the CE. As Saccani et al. [76] note “practices and strategies proposed by the literature are still largely fragmented and not interpreted through an overarching theory, which prevents the understanding of how circular supply chains should be managed and coordinated” (p. 469).

Secondly, there is only very limited recycling of the end product. Existing concepts for reuse and recycling in the companies are currently mainly found for packaging materials, but only in individual cases for the textile products themselves. The foundations for the recyclability of a product are already in place in the design phase, in which the material composition ensures that products can be manufactured without hazardous chemicals, used for as long as possible, repaired if necessary and recycled at the end of the use phase. This is in line with the eco-design guidelines within the EU strategy for sustainable and circular textiles [15]. So far, however, companies seem to focus primarily on the upstream supply chain. The phases of product use, disposal and recycling, which are usually downstream processes external to the company, are only considered sporadically and supported by appropriate measures in product development. Products will need to be broken down into their components after reaching the end of life and fed back into appropriate biological or technical cycles. This will require functioning processes to collect and sort used textiles from customers and consumers, and the technical capability to separate and recycle the individual components.

Thirdly, there are issues around standards and measurement of sustainability. There are no uniform standards for reporting and no tangible, verifiable indicators, making it very difficult to compare or evaluate the quality and success of sustainability performance. Surprisingly few companies are actively adopting the UN SDGs in their reporting of sustainability. Companies individually set different priorities and comparisons are only possible to a limited extent. Similarities in sustainability activities relate primarily to social and ecological standards among suppliers and partners in the Asian production countries, which the companies undertake as part of their inspection operations in line with their code of conduct. In doing so, they are guided by the OECD's sector risks [70], which are achieved through direct support in the implementation of standards and monitored through regular visits, audits and certifications. However, cross-supply supply chain transparency and monitoring vary greatly among the companies studied. While some of them trace back all processing steps and ingredients and make them transparent for consumers, others have set this as a goal for the next few years, and still others do not provide any information about the deeper supply chain. Although various labels and certificates are used, there are no standard formats or templates. Most labels focus either on environmental or social factors. Furthermore, they often concern different parts of the textile value chain (raw material production, manufacturing, transport/trade, use phase, end-of-life). Only a few labels, such as the Green Button, cover both social and environmental standards along a large part of the supply chain. Fourthly, the transition to a CE will require appropriate partnerships and collaborative investment. Size and resource constraints make it difficult for SMEs to develop and implement own recycling processes. Individual examples such as Cibutex - established by DI and other industry actors - demonstrate the importance of partnering with other companies to establish recovery and recycling processes. For such companies that operate in the Business-to-Business (B2B) sector, it seems to be easier to develop and implement corresponding collaborative concepts. Companies operating in the Business to Consumer (B2C) sector still lack functioning take-back systems or end-of-life concepts for used products. The expected introduction of producer responsibility in accordance with the EU strategy for sustainable and circular textiles is therefore not yet matched by any functioning concepts or capabilities on the part of the SMEs considered.

Fifthly, the industry appears to be at a turning point in the use of digital technologies for the implementation of sustainability goals and CE related activities. Although few companies currently report on product or process innovations in connection with digital technologies, the need for increased transparency along the entire supply chain to reduce and avoid negative impacts requires digital technologies for data collection and processing. Already, a few companies are making product and supply chain information available to consumers quickly and easily using QR codes and Smartphone apps. Without knowledge of the entire supply chain, the goals set out in the EU strategy for sustainable and circular textiles cannot be achieved. In particular, the requirement for a digital product passport, which is to be introduced by 2024 according to the EU strategy, will force companies to further address the digital transparency and traceability of their entire supply chain.

The comparatively high number of companies planning to implement blockchain and big data applications may indicate that companies are adapting and starting to act in response to these future requirements. It is also clear from individual company statements that it is increasingly recognised that a lack of digitalisation leads to high administrative costs in achieving sustainability goals. BR reports that, particularly in the case of data retrieval and maintenance of the supply chains, the administrative effort is immense. Similarly, LO reported that their risk analysis is based first and foremost on the company's data, but due to outdated legacy IT infrastructure, analysing the data is very time-consuming and in-depth analyses of the data are very difficult to carry out. The company planned a comprehensive digitalisation project, to improve data collection and evaluation.

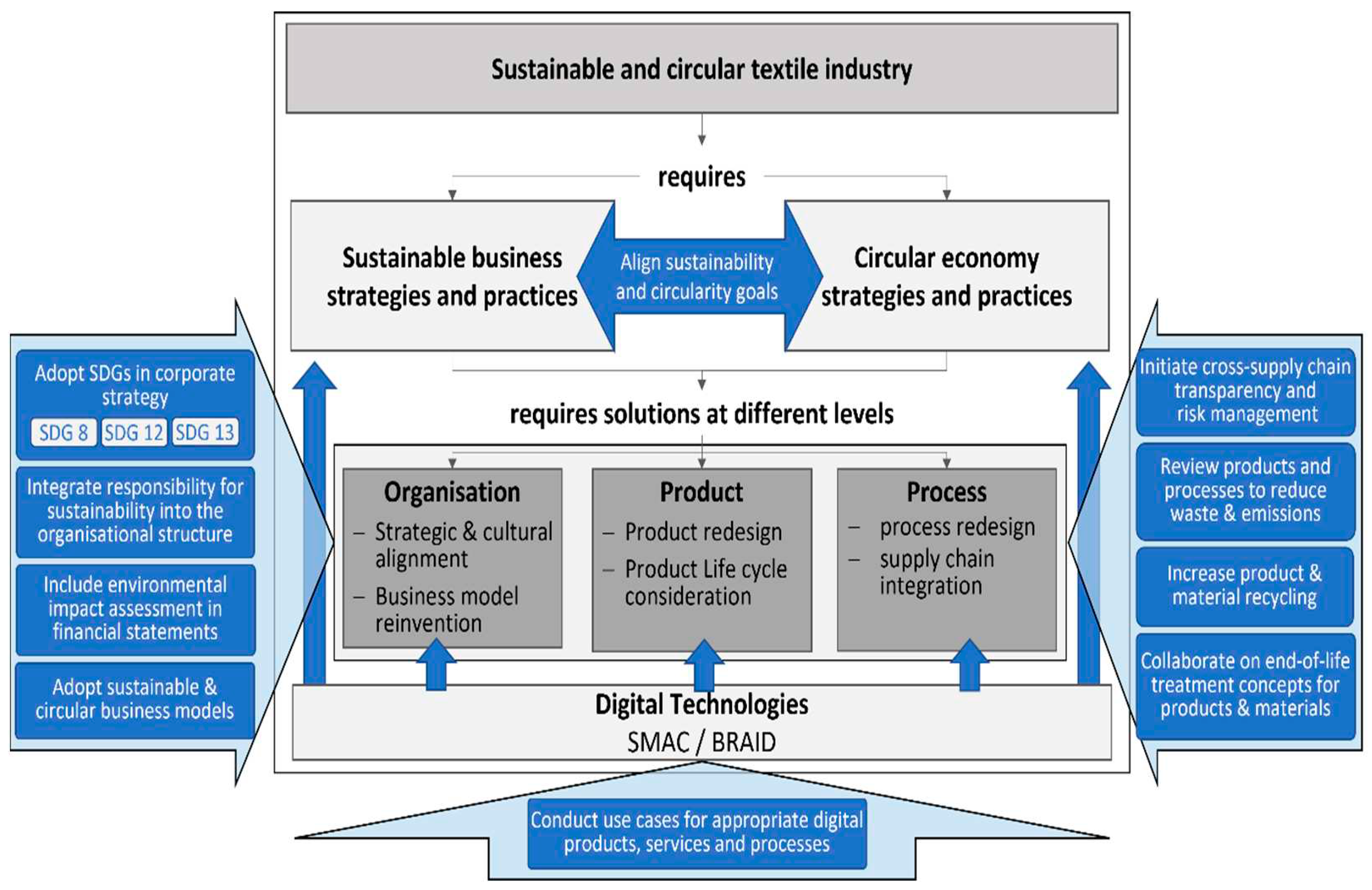

Company size is an important factor here, as high investments in technologies, processes and employee training are often necessary, as examples from larger companies show [77]. For SMEs operating in the T&C sector, there are no exemplar cases of best practice in companies of this size, with little guidance available on how to progress the transition to a CE with a more limited resource base. As regards the academic literature, Bressanelli et al. [57] recently observed that “the literature continues to struggle to understand how these technologies might contribute to value creation in the implementation of the circular economy” (p. 2). This research makes a small contribution to addressing this gap in the literature, and a simple operational model for transitioning to the CE is put forward here (Figure 8). This builds upon the conceptual framework set out in section 2, and contains a number of possible actions that can be used as a check-list to initiate the transition to a CE. It is not definitive, and not all of these possible initiatives will apply in all company contexts, but it may act as a top-level blueprint to kick-start and monitor transition.

The model requires that both circular economy and wider sustainability strategies and practices are aligned and encompassed within the company’s overall business strategy. Some of the United Nations’ SDGs may be useful points of reference in re-orientating corporate strategy. The transition can be initiated via a range of initiatives to change the overall organisational culture and mode of operation. This may entail cross-company training and awareness programmes, new company structures, the creation of new posts and recruitment or redeployment of key personnel to fill them. The core company products may require re-design to reduce waste and emissions and engender product and materials recycling. Wider process re-design will likely be necessary, and TBL accounting practices, notably as regards environmental impact assessment, can be adopted in financial reporting processes. Cross-supply chain collaboration and action will be required, including new product end-of-life treatment, quality assessment and data transparency in both upstream and downstream business partners. Appropriate trialing of digital technologies to support these initiatives should be undertaken as use cases that may provide the starting point for wider technology change projects. All these change initiatives need to be coordinated, cross-referenced and well-managed as part of a major corporate change project, led, ideally, by the CEO or other senior manager.

6. Conclusions

This exploratory paper has examined how SMEs in the German T&C industry are approaching the issues of sustainability and the CE, and assessed the role digital technologies are playing in the transition to a sustainable and circular textile industry. The results suggest these companies view sustainability as a key strategic issue and orient their corporate actions towards the achievement of social and ecological goals to gain competitive advantage by consciously differentiating themselves from the global fast fashion industry. A large proportion of the sustainability reports also refer to specific activities related to the CE, but at present, there is no clear recognition of the concept as a strategic objective, nor is it viewed holistically within these companies or across the extended supply chain. Although these businesses currently make only limited use of digital technologies to support their sustainability efforts, the results suggest that digitalisation is increasingly influencing the competitiveness of companies in the T&C sector, and notably that of SMEs. At the same time, supply chain transparency is putting more pressure on companies to make processes and products more sustainable. As of now, initiatives to implement more sustainable and circular processes, products, and business models have not been directly driven by digitalisation, which to date has seemingly not acted as the catalyst for such a transition. However, indications from the CSR reports and feedback from the online survey suggest the industry may now be at a crossroads, from which many companies will advance with a more positive recognition of the need to transition to CE practices, facilitated by digitalisation to effectively meet compliance requirements and satisfy evolving customer expectations.

The study has its limitations in that it is based on publicly available information from 29 SMEs, and a short follow-up survey focused on digital technology deployment. The analysis of company reports provides an incomplete picture and needs to be considered with caution when drawing conclusions at industry level. Future work based on case studies is needed to investigate best practices and approaches that can enable and facilitate the transformation process for SMEs, including recommendations for action and strategies for their long-term competitiveness in a sustainable and circular textile industry. In this context, the operational framework put forward in this article may act as a starting point for more detailed research, which could apply, develop and refine the actions required to move towards the circular economy. Further research could also focus on examining external market influences such as the expected laws and regulations under the EU strategy for sustainable and circular textiles and how SMEs can most effectively align their sustainability strategies and actions. Further studies might also examine how the growing customer awareness of the environmental impact of the clothing industry in different geographical locations is affecting the industry. As Claudio [78] noted fifteen years ago, “the biggest impacts for increasing sustainability in the clothing industry rests with the consumer” and “consumer awareness about the fate of clothing through its life cycle may be the best hope for [future] sustainability” (p. 454). This indeed may be the key factor that finally pushes the industry into adopting the CE in its practices and operations.

Author Contributions

Conceptualization, T.W. and M.W.; methodology, T.W. and M.W.; validation, T.W.; formal analysis, T.W. and M.W.; investigation, T.W.; data curation, T.W.; writing—original draft preparation, T.W. and M.W; writing—review and editing, T.W. and M.W.; visualization, T.W. and M.W.; supervision, MW.; project administration, T.W. All authors have read and agreed to the published version of the manuscript

Funding

This research received no external funding.

Data Availability Statement

All research data is displayed within the article. The on-line survey was conducted anonymously.

Conflicts of Interest

The authors declare no conflict of interest.

References

- European Commission. Sustainability strategy for textiles. Available online: https://ec.europa.eu/growth/industry/sustainability/strategy-textiles_en (accessed on 28 December 2021).

- European Commission. Closing the loop - An EU action plan for the Circular Economy. Available online: https://ec.europa.eu/transparency/documents-register/api/files/COM(2015)614_0/de00000000332178?rendition=false (accessed on 11 March 2022).

- Alonso-Muñoz, S.; González-Sánchez, R.; Siligardi, C.; García-Muiña, F.E. New Circular Networks in Resilient Supply Chains: An External Capital Perspective. Sustainability 2021, 13, 6130. [CrossRef]

- European Commission. COM(2020) 98 final: A new Circular Economy Action Plan: For a cleaner and more competitive Europe. Available online: https://eur-lex.europa.eu/resource.html?uri=cellar:9903b325-6388-11ea-b735-01aa75ed71a1.0017.02/DOC_1&format=PDF (accessed on 5 May 2022).

- EURATEX. Circular textiles: Prospering in the circular economy. Available online: https://euratex.eu/wp-content/uploads/EURATEX-Prospering-in-the-Circular-Economy-2020.pdf (accessed on 28 December 2021).

- Okorie, O.; Salonitis, K.; Charnley, F.; Moreno, M.; Turner, C.; Tiwari, A. Digitisation and the Circular Economy: A Review of Current Research and Future Trends. Energies 2018, 11, 3009. [CrossRef]

- Wynn, M.; Jones, P. Digital Technology Deployment and the Circular Economy. Sustainability 2022, 14, 9077. [CrossRef]

- World Economic Forum. Why digitalization is critical to creating a global circular economy (accessed on 9 December 2021).

- Kottmeyer, B. Digitisation and Sustainable Development: The Opportunities and Risks of Using Digital Technologies for the Implementation of a Circular Economy. Journal of Entrepreneurship and Innovation in Emerging Economies 2021, 7, 17–23. [CrossRef]

- Ranta, V.; Aarikka-Stenroos, L.; Väisänen, J.-M. Digital technologies catalyzing business model innovation for circular economy—Multiple case study. Resources, Conservation and Recycling 2021, 164, 105155. [CrossRef]

- EEA. Textiles and the environment in a circular economy: Eionet Report - ETC/WMGE 2019/6. Available online: file:///C:/Users/Twiegand4/Downloads/ETC-WMGE_report_final%20for%20website_updated%202020.pdf (accessed on 22 August 2022).

- Neugebauer, C.; Schewe, G. Wirtschaftsmacht Modeindustrie – Alles bleibt anders [In English: Economic Power of the Fashion Industry - Everything Remains Different]. Aus Politik und Zeitgeschichte 2015, 65, 31–41.

- Gözet, B.; Wilts, H. Die Kreislaufwirtschaft als neues Narrativ für die Textilindustrie: Eine Analyse der textilen Wertschöpfungskette mit Blick auf Deutschlands Chancen einer kreislaufwirtschaftlichen Transformation [In English: The Circular Economy as a New Narrative for the Textile Industry: An Analysis of the Textile Value Chain with a View to Germany's Opportunities for a Circular Economy Transformation]. Zukunftsimpuls No. 23, Wuppertal, 2022. Available online: http://hdl.handle.net/10419/260402.

- European Commission. COM(2020) 102 final: A New Industrial Strategy for Europe. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52020DC0102&from=EN (accessed on 5 May 2022).

- European Commission. COM (2022) 141 final: EU Strategy for Sustainable and Circular Textiles. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52022DC0141.

- CSIL. Center for Industrial Studies: Final Roport on Data on the EU Textile Ecosystem and its Competitiveness. Available online: https://op.europa.eu/o/opportal-service/download-handler?identifier=574c0bfe-6142-11ec-9c6c-01aa75ed71a1&format=pdf&language=en&productionSystem=cellar&part=.

- Ki, C.-W.; Chong, S.M.; Ha-Brookshire, J.E. How fashion can achieve sustainable development through a circular economy and stakeholder engagement: A systematic literature review. Corp Soc Responsib Environ Manag 2020, 27, 2401–2424. [CrossRef]

- Stewart, R.; Niero, M. Circular economy in corporate sustainability strategies: A review of corporate sustainability reports in the fast-moving consumer goods sector. Bus. Strat. Env. 2018, 27, 1005–1022. [CrossRef]

- Franco, M.A. Circular economy at the micro level: A dynamic view of incumbents’ struggles and challenges in the textile industry. Journal of Cleaner Production 2017, 168, 833–845. [CrossRef]

- Ghisellini, P.; Cialani, C.; Ulgiati, S. A review on circular economy: the expected transition to a balanced interplay of environmental and economic systems. Journal of Cleaner Production 2016, 114, 11–32. [CrossRef]

- Farooque, M.; Zhang, A.; Thürer, M.; Qu, T.; Huisingh, D. Circular supply chain management: A definition and structured literature review. Journal of Cleaner Production 2019, 228, 882–900. [CrossRef]

- World Commission on Environment and Development. Our common future. Available online: https://digitallibrary.un.org/record/139811 (accessed on 1 May 2022).

- Montiel, I. Corporate Social Responsibility and Corporate Sustainability. Organization & Environment 2008, 21, 245–269. [CrossRef]

- Elkington, J. Cannibals with forks: The triple bottom line of 21st century business; New Society Publishers: Gabriola Island, B.C., 1998, ISBN 0865713928.

- Amini, M.; Bienstock, C.C. Corporate sustainability: an integrative definition and framework to evaluate corporate practice and guide academic research. Journal of Cleaner Production 2014, 76, 12–19. [CrossRef]

- Hallstedt, S.; Ny, H.; Robèrt, K.-H.; Broman, G. An approach to assessing sustainability integration in strategic decision systems for product development. Journal of Cleaner Production 2010, 18, 703–712. [CrossRef]

- Porter, M.E.; Kramer, M.R. Strategy and Society: The Link Between Competitive Advantage and Corporate Social Responsibility. Harvard Business Review 2006, 78–92.

- Seuring, S.; Müller, M. From a literature review to a conceptual framework for sustainable supply chain management. Journal of Cleaner Production 2008, 16, 1699–1710. [CrossRef]

- United Nations. Transforming Our World: The 2030 Agenda for Sustainable Development. Available online: https://sustainabledevelopment.un.org/post2015/transformingourworld (accessed on 24 May 2022).

- European Commission. The 2010 Agenda for Sustainable Development and the SDGs. Available online: http://ec.europa.eu/environment/sustainable-development/SDGs/index_en.htm (accessed on 24 May 2022).

- PricewaterhouseCoopers. Making It Your Business; Engaging with the Sustainable Development Goals. Available online: https://www.pwc.com/gx/en/sustainability/SDG/SDG%20Research_FINAL.pdf (accessed on 24 May 2022).

- Wynn, M.; Jones, P. The Sustainable Development Goals; Routledge, 2019, ISBN 9780429281341.

- United Nations. Summary Table of SDG Indicators. Available online: https://unstats.un.org/sdgs/files/meetings/iaeg-sdgs-meeting-06/Summary%20Table_Global%20Indicator%20Framework_08.11.2017.pdf (accessed on 24 May 2022).

- Deloitte. How Deloitte supports the United Nations Sustainable Development Goals. Available online: https://www2.deloitte.com/content/dam/Deloitte/global/Documents/About-Deloitte/gx_SDGs_Deloitte.pdf (accessed on 4 June 2022).

- Kirchherr, J.; Reike, D.; Hekkert, M. Conceptualizing the circular economy: An analysis of 114 definitions. Resources, Conservation and Recycling 2017, 127, 221–232. [CrossRef]

- Murray, A.; Skene, K.; Haynes, K. The Circular Economy: An Interdisciplinary Exploration of the Concept and Application in a Global Context. J Bus Ethics 2017, 140, 369–380. [CrossRef]

- Ellen McArthur Foundation; Mc Kinsey Center for Business and Environment. GROWTH WITHIN: A CIRCULAR ECONOMY VISION FOR A COMPETITIVE EUROPE. Available online: https://emf.thirdlight.com/link/8izw1qhml4ga-404tsz/@/preview/1?o (accessed on 1 May 2022).

- Bocken, N.; Short, S.W. Towards a sufficiency-driven business model: Experiences and opportunities. Environmental Innovation and Societal Transitions 2016, 18, 41–61. [CrossRef]

- Geissdoerfer, M.; Morioka, S.N.; Carvalho, M.M. de; Evans, S. Business models and supply chains for the circular economy. Journal of Cleaner Production 2018, 190, 712–721. [CrossRef]

- Geissdoerfer, M.; Pieroni, M.P.; Pigosso, D.C.; Soufani, K. Circular business models: A review. Journal of Cleaner Production 2020, 277, 123741. [CrossRef]

- Fluchs, S.; Neligan, A.; Schleicher, C.; Schmitz, E. Zirkuläre Geschäftsmodelle. Wie zirkulär sind Unternehmen? [In English: Circular Business Models. How circular are Businesses?]. Available online: https://www.iwkoeln.de/studien/sarah-fluchs-adriana-neligan-wie-zirkulaer-sind-unternehmen.html (accessed on 7 October 2022).

- Nußholz, J. Circular Business Models: Defining a Concept and Framing an Emerging Research Field. Sustainability 2017, 9, 1810. [CrossRef]

- Brown, P.; Daniels, C. von; Bocken, N.; Balkenende, A.R. A process model for collaboration in circular oriented innovation. Journal of Cleaner Production 2021, 286, 125499. [CrossRef]

- Montag, L.; Klünder, T.; Steven, M. Paving the Way for Circular Supply Chains: Conceptualization of a Circular Supply Chain Maturity Framework. Front. Sustain. 2021, 2. [CrossRef]

- Association for Supply Chain Management. The SCOR Digital Standard. Available online: https://www.ascm.org/corporate-solutions/standards-tools/scor-ds/ (accessed on 29 April 2023).

- Montag, L.; Pettau, T. Process performance measurement framework for circular supply chain: An updated SCOR perspective. CE 2022. [CrossRef]

- Turchi, P. The Digital Transformation Pyramid: A Business-driven Approach for Corporate Initiatives. Available online: https://www.thedigitaltransformationpeople.com/channels/the-case-for-digital- (accessed on 4 October 2021).

- Lang, V. Digitalization and Digital Transformation. In Digital Fluency; Lang, V., Ed.; Apress: Berkeley, CA, 2021; pp 1–50, ISBN 978-1-4842-6773-8.

- Frost & Sullivan. The Impact of Digital Transformation on the Waste Recycling Industry: Capitalizing on Opportunities in the Emerging Digital Economy: Research Code: Maab-01-00-00-00. Sku: En01044-Gl-Mo_21500, 2018.

- Reuter, M.A. Digitalizing the Circular Economy. Metall and Materi Trans B 2016, 47, 3194–3220. [CrossRef]

- Salminen, V.; Ruohomaa, H.; Kantola, J. Digitalization and Big Data Supporting Responsible Business Co-evolution. In Advances in Human Factors, Business Management, Training and Education; Kantola, J.I., Barath, T., Nazir, S., Andre, T., Eds.; Springer International Publishing: Cham, 2017; pp 1055–1067, ISBN 978-3-319-42069-1.

- Bressanelli, G.; Perona, M.; Saccani, N. Challenges in supply chain redesign for the Circular Economy: a literature review and a multiple case study. International Journal of Production Research 2019, 57, 7395–7422. [CrossRef]

- Owen-Jackson, C. Reducing waste and cutting costs: How digital tech is powering up the circular economy. Available online: https://www.kaspersky.com/blog/secure-futures-magazine/circular-economy-it/31811/.

- Pagoropoulos, A.; Pigosso, D.C.; McAloone, T.C. The Emergent Role of Digital Technologies in the Circular Economy: A Review. Procedia CIRP 2017, 64, 19–24. [CrossRef]

- Antikainen, M.; Uusitalo, T.; Kivikytö-Reponen, P. Digitalisation as an Enabler of Circular Economy. Procedia CIRP 2018, 73, 45–49. [CrossRef]

- Del Giudice, M.; Chierici, R.; Mazzucchelli, A.; Fiano, F. Supply chain management in the era of circular economy: the moderating effect of big data. IJLM 2021, 32, 337–356. [CrossRef]

- Bressanelli, G.; Adrodegari, F.; Pigosso, D.C.A.; Parida, V. Circular Economy in the Digital Age. Sustainability 2022, 14, 5565. [CrossRef]

- Neligan, A. Digitalisation as Enabler Towards a Sustainable Circular Economy in Germany. Intereconomics 2018, 53, 101–106. [CrossRef]

- Wynn, M.; Jones, P. ICTs and the Localisation of the Sustainable Development Goals. International Journal of Social Ecology and Sustainable Development 2022, 13, 1–15. [CrossRef]

- Cagno, E.; Neri, A.; Negri, M.; Bassani, C.A.; Lampertico, T. The Role of Digital Technologies in Operationalizing the Circular Economy Transition: A Systematic Literature Review. Applied Sciences 2021, 11, 3328. [CrossRef]

- Laskurain-Iturbe, I.; Arana-Landín, G.; Landeta-Manzano, B.; Uriarte-Gallastegi, N. Exploring the influence of industry 4.0 technologies on the circular economy. Journal of Cleaner Production 2021, 321, 128944. [CrossRef]

- Jabareen, Y. Building a Conceptual Framework: Philosophy, Definitions, and Procedure. International Journal of Qualitative Methods 2009, 8, 49–62. [CrossRef]