Submitted:

28 December 2025

Posted:

29 December 2025

You are already at the latest version

Abstract

In this exploratory paper on Environmental, Social, and Governance (ESG) issues and small and medium sized enterprises (SMEs) we offer critical insights into the meaning, scope and application of ESG principles for SMEs. Referring to both academic and indus-try literature, the paper identifies the key ESG concepts, definitions, principles and prac-tices and how they drive the interests of business and policy makers. We examine how fa-cilitative regulation, social integration and innovative opportunities among SMEs can be generated by an adherence to ESG in practice. How do SMEs incorporate the ten key prin-ciples that emphasize the different aspects of sustainability, social responsibility, and corporate governance, that can guide good business practice through ESG-led innovation? Using both academic and professional literature, we assess what concepts, frameworks, policies and principles could apply to this community of SMEs. Our in-depth analysis of principles, policies and practice includes an illustrative case study of ESG adoption in practice. This leads us to work towards the development of a practical framework appli-cation by SMEs. Our framework is proposed against the backdrop of constraints that SMEs have to contend with when incorporating new ideas and turning them into reality. We conclude by anticipating the future of ESG.

Keywords:

environmental

; social

; governance

; sustainability

; SMEs

; innovation

1. Introduction

ESG stands for Environmental, Social, and Governance (ESG) factors underpinning institutional efforts to manage sustainability. It represents a concept for use by businesses, investor and policy organisations to measure performance against the ESG factors. The general objective for different stakeholders to evaluate the risks associated with the management of ESG, and their impact on the wider society and the environment in which it is embedded [1]. Often used interchangeably with the popular concept of sustainability, Mitra and Bui (2024) [2] have argued that ESG is claimed in both private and public sector debates as a performance criteria set with which a business can communicate its impact or dependencies on:

- The environment (E) (for example, carbon emissions, use of natural resources, waste to landfill data),

- Society (S) (for example, standards for human rights, gender pay gaps, diversity representation and employee turnover).

- Taking responsibility for the efficient and effective management of opportunities and risks, or its governance (G) (for example, composition of the board, executive pay and bonuses, regulatory compliance).

ESG criteria aims to provide an instrument with which to assess both longer-term opportunities and risks that is wider in scope than what typical financial metrics can help to evaluate. The wider considerations are essentially those of environmental stewardship, social responsibility, governance practices and the wider ecosystem [3,4,5]. As their importance and applications have grown over time it is worthwhile considering how the concept has emerged and its increasing significance.

The Emergence and Growing Importance of ESG

Let us consider why ESG has attracted so much attention across policy, business and research circles. The rising momentum for change stemming from a global concern over carbon emissions, climate change, together with the resolution of economic and social implications of these issues, appears to have jolted decision makers to seek solutions to deal with them. Take for instance the question of the e world’s average temperature rising to 2.0 C instead of 1.50 above pre-industrial levels. In this situation the global economy could be $100 trillion poorer. In fact, a more ambitious target would necessitate reaching zero CO2 emissions by 2050. That means that in less than three decades the energy system of our entire civilisation together with the agricultural system that currently feeds 8 billion people around the world will have to be rebuilt [6]. The impact is not only on how we produce goods and provide for services but how we now live our lives and how we work. In considering this impact there is a need for a concerted approach towards taking innovative steps and making meaningful decisions that can generate a productive and beneficial transformation of business processes, systems, and practices within and outside organisational boundaries.

Countries have over the past few years taken some transformative steps. The USA passed the world’s largest climate bill, the EU enshrined its Green Deal in active legislation and the fast growing (and, therefore, highly polluting) economies of China and India have set net zero targets [6], although of course the USA under its current administration has reneged on its commitment again. Notable in the scheme of global awareness is the leadership of the United Nations and the motivation to sign the Paris Agreement by 195 countries. They set a target of keeping global average temperatures below 2 degrees relative to pre-industrial levels while attempting to limit it to 1.50 [6].

The core concept of ESG investing can be traced back to religious codes banning investments in slave labour. Much later in the in the 1960s and 1970s, divestments (as part of socially responsible investment strategies) from South Africa were first advocated to protest against the country’s system of apartheid. These ideas focused on avoiding investments in industries associated with negative social impacts, such as tobacco, firearms, and apartheid in South Africa [4]. There has been considerable progress since then with, however, the usual back pedalling or forestalling by various countries and agencies.

ESG can be regarded as cognate to earlier concepts of corporate social responsibility (CSR) and socially responsible investing (SRI) and indeed to the very idea of sustainability. But while CSR and ESI were primarily concerned with the application and governance of ethical principles inherent in the social responsibility of organisations to the communities they serve, sustainability can be regarded as being incompatible with business because it was never developed by, or for, businesses [7]. In other words, the term sustainability (understood as environmental and social impact) which is drawn from ecological science [8] can be regarded as an externality which does not fit in with the ideas of economic efficiency in or the bottom line of profit-making by business units [7]. Sustainable development codified in the form of international development goals of the United Nations, as Sustainable Development Goals (SDGs) that apply from 2016 to 2030 can be regarded as having a contemporaneous and possible influence on ESF. The influence can be best understood in terms of the difference of the two concepts: sustainability can be referred to as the policies and strategies that organisations use, while ESF are the practices and conduct of the organisations, based on those policies and strategies [7].

We can identify the most important landmarks of ESG’s journey to date as outlined in Table 1 below.

Various other initiatives have bolstered the importance of ESG and its application. They include the 2022, Consolidation of Sustainability standards which aimed to set global standards that moved away from the previous position of the International Financial Reporting Standards (IFRS) Foundation. The IFRS Foundation maintained accounting standards for most countries, except the U.S. The EU directive, the Corporate Sustainability Reporting Directive (CSRD) came into operation in 2023, specifying that approximately 50,000 EU companies and non-EU businesses had to ensure that annual disclosures were made on the risks and opportunities related to social and environmental issues associated with their business activities. The CSRD also mandates affected companies to report on the impact their operations have on people and the environment. Additionally, in 2024, the EU introduced another sustainability-related measure (the EU: the Corporate Sustainability Due Diligence Directive (CSDDD). From 2027 firms, qualifying firms will be required to identify and take remedial action on adverse impacts on human rights and the environment covering both internal operations and supply chains [12].

As Table 1 above shows the ESG journey has been a complex one with slow and steady movements building the interconnectedness between the three critical alphabets denoting the phenomenon of ESG. Starting first with the obvious focus on the environment it soon became clear the questions about the environment could not be regarded in isolation from social and governance factors. How could this miasma of rules, regulations, institutional change and practice be of relevance to SMEs?

Critically, for our purpose, there is the need to assess the impact on business generally (and SMEs in particular) and understanding how SMEs could find innovative ways to use ESG for productive outcomes. Entrepreneurial and innovative SMEs evolve continually. They find new directions in the changing landscape of social, environmental, technological and structural changes (all inherent in the application of ESG) have led to the emergence of organisational changes and a learning process which attempt to integrate economic and goals through various structural adjustments within the organisation and in the networks of relationships in their wider ecosystem [5].

Following an explanation of the methodology, the rest of the paper is structured in four parts to explore critically different aspects of ESG to ensure that the essential components of ESG are understood sufficiently so that they could be tested in the in the realm of SMEs in terms of their application for innovative practice. After describing our methods and approach to our research, we explain the reasons for the growing significance of ESG together with its core components showing how the three components are interconnected allowing for the emergence of a holistic and strategic approach to its creative application. Such an approach makes it possible to understand how ESG application can make both commercial and environmental sense. Crucially, we see the interconnectedness of the components as the key driver for innovative business practice. We continue with our findings in the form of a detailed and critical analysis of how ESG has been adopted in business practice with a particular focus on the application of ESG among different SMEs, and ending with a mini case study of a successful application of ESG by a small firm. This demand side scenario is then complemented by a critical overview of the supply side led provisions for ESG together with policies developed by governments across the world. The overall analysis takes us to the discussions where we propose a framework for ESG adoption together with the metrics necessary for evaluation against the backdrop of constraints faced by SMEs. We conclude by anticipating the future of ESG and their value for SMEs and business in general.

2. Methodology

2.1. Materials and Methods

Our method is simple and driven by considerations of explorations of key concepts, principles and practice. We rely on descriptive research techniques to identify, observe and describe the characteristics or functions and the interconnectedness of the ESG phenomenon in the business context. In keeping with this approach, we do not manipulate any variables or try to demonstrate causal explanations. Our purpose is to note and answer the “what, where, when, and how” of the ESG phenomenon by providing a detailed snapshot of its essence, and then reviewing them further in the specific context of SMEs [14,15].

We draw on baseline data to identify trends, thus establishing key, foundational knowledge of ESG for future research and summarise some of the intricacies and complexities of the phenomenon in the form of comprehensible descriptions. The aim is to provide policy makers and business organisations, particularly SMEs with critical insights.

We follow a narrative literature review of peer reviewed publications and industry reports that discuss advances in ESG over the period selected in the milestones table (Table 1). This allows for a flexible, interpretive synthesis of both existing academic research and scholarship together with policy interventions and evidence from practice enabling the contextualisation of dual sources of knowledge, reviewing extant debates, and identifies what is possible to develop, instead of quantifying evidence based on an acceptance of given data sets [16,17]. This approach is valuable for a broad, interdisciplinary and evolving subject and interrelated topics such as ESG where systematic reviews may be too rigid or too early to develop.

The use of both types of literature carries methodological salience not least because we are attempting to understand the relevance of complex and relatively nascent concepts and their application. Our justification for the use of mixed literature especially in the context of ESG research is based on the need for bridging theory and practice [18]. The growth in the interest in ESG has occurred almost concurrently among academic researchers, policy makers and industry practitioners, suggesting a need for urgent and joined -up thinking and action at all levels. While academic literature provides conceptual frameworks (e.g., stakeholder, legitimacy, and agency theories) to understand ESG dynamics, state-of-the-art policy and company reports provide us with real-time insights into implementation, regulatory compliance, and strategic adaptation. The resulting blend facilitates a more nuanced understanding of ESG’s impact on firm value and governance structures for both theory-building and practice.

On the specific question of ESG and multi-stakeholder perspectives, compliance and with and the use -value of ESG requires the involvement of a diverse set of actors — governments, firms, investors, and civil society [19]. While academic sources can highlight normative and analytical depth, company disclosures and policy documents reflect functional and operational realities alongside stakeholder engagement strategies. Consequently, mixed sources ensure that research is both theoretically grounded and practically relevant. This is especially important in ESG, where evolving standards and stakeholder expectations demand context-sensitive analysis, especially in a climate of flux and changing regulatory responses. In uncertain environments it becomes even more important to address gaps in data and evidence. Since metrics are heterogeneous and often lack standardisation, company reports and policy frameworks can supplement academic ‘black holes’, especially in under-researched sectors or regions where the evidence is patchy. An ensuing need is for the development of supporting comparative and longitudinal analysis. Academic studies offer historical and cross-sectoral comparisons while policy and corporate documents provide up-to-date developments, enabling dynamic tracking of ESG trends and regulatory shifts. Overall, mixed literature helps identify best practices, regulatory innovations, and market responses because it supports evidence-based recommendations for improving ESG performance, disclosure, and governance [20].

2.2. Thematic Focus

The literature review used Google scholar and Scopus with keywords and phrases including: ESG, growing significance, core components, business practice, access to finance, risk mitigation, resilience, supply chains, regulation, governance, sustainability, environment, and innovation. These keywords, phrases and sub-themes, were then re-organised as eight meta-level themes to help guide the discussion of our findings. They include materiality and transparency as conceptual meta-themes supplemented by the operationally driven constructs of stakeholder engagement, resource allocation, regulatory compliance, supply chain management, sustainable culture development, and leveraging technology for innovation.

The review highlighted different approaches to the interpretation, standardisation and application of ESG principles and their institutionalisation over time. The consideration of multiple approaches allowed us to explore an adequate level of synthesis to help develop an analytical framework.

We examine the ‘real-life’ application of these concepts and practices through a case study of an SME, investigating how meaningful and successful outcomes flow from adopting ESG as a tool for innovation. We extend our analysis by exploring the supply side aspects of ESG. It is not possible to describe all relevant ESG details since our focus was on their particular relevance and value for SMEs.

Our findings and analysis provide a solid foundation for the development of future studies and the facilitation of SME-focused policy development. The study attempts to provide a framework based on our understanding of the interrelationships between the main concepts [21] and how they can inform policy formulation. We also demonstrate their importance for entrepreneurship and management research while dealing with the problem of trying to analyse a phenomenon that has not been properly defined [22,23]. We do not attempt to build any new theory although we extract material from our findings which could lend themselves to future theoretical and empirical research.

3. Results

3.1. The Growing Significance of ESG

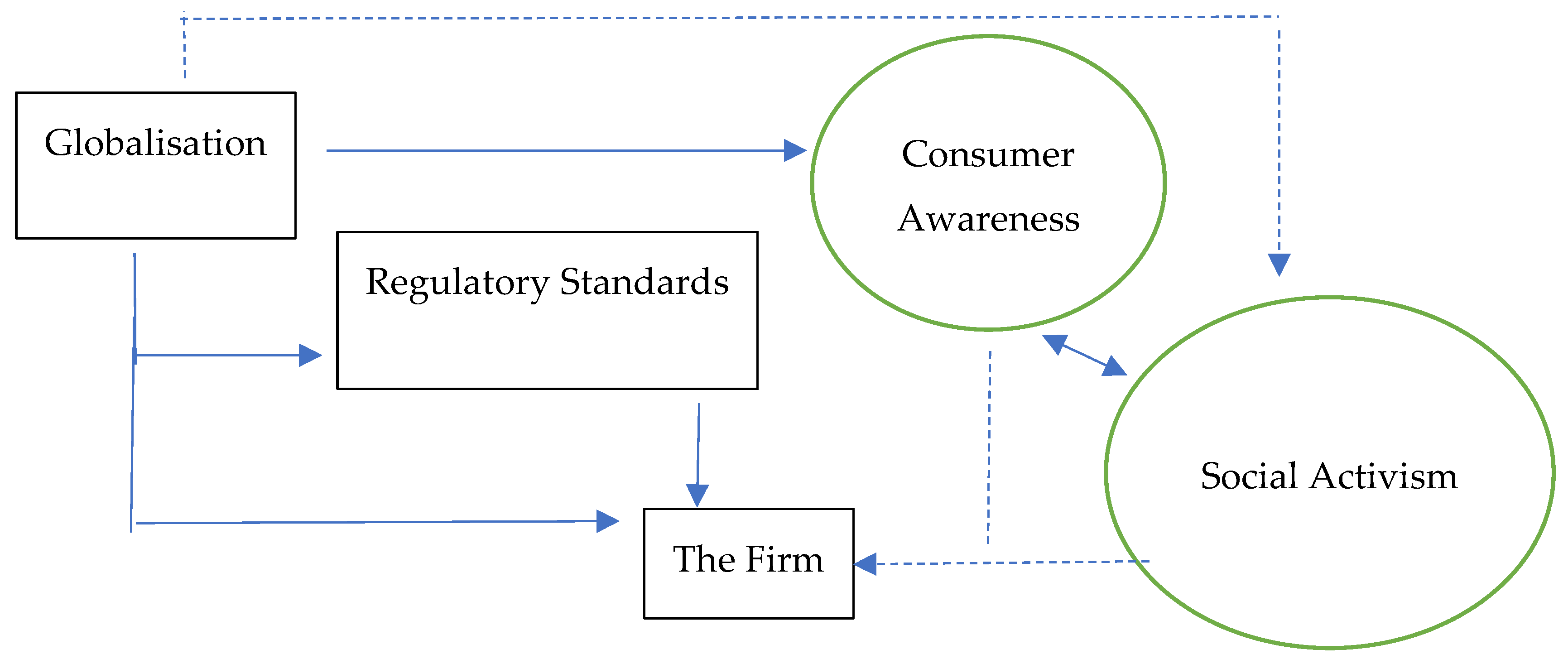

Our review of the literature helps us to identify four factors underpinning the rising significance and importance of ESG – globalisation, investor pressure and consumer demand, industry standards and regulation, and emergent social movements [2].

First, globalisation and access to widespread information enabled by accelerating technological advances, have increased the visibility of the environmental and the social impact of, primarily, corporate operations, leading to greater stakeholder awareness and demand for responsible business practices beyond the realisation of profits. ESG considerations are not independent of the high levels of global connectivity firms that is evinced in the making of products, the production of services, the generation and sharing of data inherent in product development and service provision, and often interlinked financial arrangements. These connectivity issues are affected by various ESG factors such as those related to climate change, social unrest, or governance failures, carrying with them considerable financial risks, which could affect long-term profitability. In these circumstances, prioritising ESG in their risk management strategies have become a strategic necessity [24]. For businesses today and their work in building homes delivering food, manufacturing clothing or computers, facilitating networked transportation, and offering other novel, platform and digital services, there is growing realisation that helping to raise the living standards of many is accompanied by significant environmental and social costs which together with their negative externalities can seriously denting the gains they have made [3]. Mitra and Bui (2024) [2] refer to the example of the food industry which has been transformed globally thanks to modern agricultural processing and techniques. However, it is also responsible for 25% of global carbon emissions. Food waste alone contributes to 6% of such emissions [25]. Significant consumer activism has propelled the need to mitigate ESG-related risks which could cause considerable financial, reputational, and operational damage.

Second, greater awareness of ESG issues and their effect on firms have accelerated the adoption and incorporation of ESG because of investor pressure and consumer demand. Investors are increasingly aligning their portfolios with their own values of sustainability-focused investment gains based on the recognition that companies with strong ESG performance are better managed when they are more resilient to the pressures of externalities. Not to left behinds, consumers, are opting for brands that prioritise ESG. This is especially true of younger consumers and activist shareholders who are more likely to scrutinise product labels and follow company activities. This in turn, adds to the pressure on companies to adopt ESG principles to maintain organisational credibility, goodwill, brand recognition and differentiation, together with market share [26].

Third, industry standards and regulatory pressures have led to governments and industry federations to introduce regulations and guidelines requiring businesses to disclose ESG-related information. Enhanced transparency and accountability have followed the implementation of these regulations, with firms that adopt smart ESG practice being better positioned to comply with these requirements and avoid fines and penalties [4].

Fourth, the rise in social movements during the late 20th and early 21st centuries advocating for human rights, diversity, equity, and inclusion have stirred the conscience of both individuals and institutional actors. High-profile corporate scandals, such as those of Enron or WorldCom or even the new tech companies and their energy-guzzling supercomputers, have highlighted the importance of good governance and ethical behaviour, pushing firms to adopt clearly defined socially responsible practices and stressing corporate accountability [11].

The S and G factors in ESG have become key components of corporate strategy, investment decision-making, and risk management. They have underscored the need for and the connectivity with good governance (G). Data generated from focused ESG management coupled with relevant metrics to help mitigate negative externalities of falling reputation or simply poor practice, can drive the company to create new values and help to build resilient businesses. Businesses that prioritise the necessary mix of environmental stewardship, social responsibility, and strong governance are likely to be better positioned to thrive in an increasingly complex and interconnected global economy.

Businesses have become more mindful of polling and public perceptions because political parties and governments fashion their economic and industrial policies based on data that shows that voters want robust, clearly defined policies on a broad range of sustainability challenges from their governments. A 2021/22 survey of 125 countries revealed that approximately 69% of the population expressed a willingness to contribute 1% of their personal income to addressing climate change, while 89% demanded intensified political action [27]. Here too, businesses can play a critical role given the amount of time and money spent on lobbying governments for, inter-alia, better support and easier access to resources.

We find a direct and indirect set of drivers at the level of business which can inform the strategies that drive businesses to thrive when recognition of the value of ESG factors can be taken on board. Th direct set includes those that impinge directly on business strategy and practice, namely, globalization and regulatory standards. They constitute a mix of economic forces at play with supply side or industry-led interventions. The indirect ones relate to higher levels of consumer awareness and social activism, indicating both the sophistication and volatile nature of the demand side. In essence and taken together they are of interest to all businesses which wish to thrive in a more open, information driven society where it is difficult to extricate the economics of business from its social imperatives. They also represent the way policy evolves in countries. Despite attempts by the very large players to hold off policy and activist challenges, an appreciation of the four factors of significance in ESG adoption cannot be ignored let alone being dismissed as an irrelevant externality. Figure 1 below summarises these four factors in terms of their direct and indirect influences.

3.1.1. The Core Components of ESG

The Environmental (E) component addresses a firm’s interaction with the natural environment both where it is located and where it may have offshore facilities, together with its supply chain. This includes the effective and efficient management of carbon emissions, energy efficiency, waste, depletion of resources and the overall impact on biodiversity. In other words, the efficiency and effectiveness with which firms manage environmental risks and opportunities especially in terms of their carbon footprint and conserve natural resources [24] is captured by the ‘E’ factor. Note that the proper management of the ‘E’ dimension is difficult to operationalize if firms do not seek to collaborate with external stakeholders.

The Social dimension (S) focuses on how a company manages relationships with its stakeholders, including employees, suppliers, customers, and the communities in which it operates. This aspect of ESG covers a wide range of issues, such as labour practices, human rights, diversity and inclusion, workplace safety, and community engagement. The social criteria evaluate how a company contributes to society and manages its relationships with stakeholders, ensuring that its operations benefit and not harm the communities it affects [11]. We note here the interplay between direct and indirect aspects – the four underpinning elements of the significance of ESG referred to in the previous section.

The Governance (G) component refers to the structures and processes that determine a company’s leadership, executive compensation, audits, internal controls, and shareholder rights. The major issues of governance include board composition, transparency, anti-corruption practices, ethical behaviours, and accountability in decision-making processes. Good governance ensures that a company is managed ethically, transparently, and in a way that aligns with the long-term interests of its shareholders and other stakeholders [4]. The core components of ESG only have value if decision making at the company is sufficiently democratic and transparent enough first acknowledge the depth and intricacy of the management process to manage ’E’ above and to ensure its operationalisation through a collaborative structure and protocol. This is relevant because of the interconnectedness of the three components [2].

3.1.2. The Interconnectedness of ESG Components and Its Indispensability for ESG Management

All three components (the ‘E’, the ‘S’, and the ‘G’) connect with each other to provide a mechanism for businesses to engage with their ecosystems in a productive and sustainable way. The wider environment embraces the society of people and their interactions which need good governance for their sustenance and valorisation.

Inadequate environmental practices can lead to social consequences, such as health hazards in communities due to pollution or the displacement of populations due to environmental degradation. The repercussions can, in turn, attract regulatory penalties or legal actions, potentially exposing the governance of the company [4]. A company’s social responsibility is often reflected in the sophistication of its governance structure. Failure in governance, such as lack of oversight or unethical leadership, can exacerbate social issues, and undermine the company’s environmental commitments [28], whereas effective governance helps to embed t environmental and social considerations within the strategic and operational decision-making processes of the company.

Governance failures, such as inadequate oversight, negligence or corruption are a function of use poor environmental management and social irresponsibility. They can result in consequential financial losses, reputational damage, and legal consequences [29]. A company that neglects its environmental responsibilities, such as failing to be transparent about climate-related risks in its production processes, may face social backlash, regulatory scrutiny, and litigation, or all three challenging its governance capability or structures and overall sustainability [4].

The deeply interconnected components form a holistic structure necessary for the long-term resilience and ethical standing of a company together with the appreciation of the synergies between these components, and how they contribute to sustainable value creation and effective risk management.

3.2. ESG and Business Practice - Integration of ESG into Business Practice: The Key Principles

If interconnectedness is vital for ESG policy and practice in a company, then the integration of ESG criteria into business strategies has emerged as a pivotal factor in shaping the future of global commerce.

Mitra and Bui (2024) [2] outline ten key principles (Ps) drive the integration of ESG into business practice. The importance of sustainability (P1), social responsibility (P2), and corporate governance (P3) have already been highlighted above. Suffice it to state that the need to minimise their environmental impact and contribute to sustainable development by considering long-term environmental risks necessitates the adoption of practices to reduce carbon emissions, manage waste responsibly, and use resources efficiently [24]. The social responsibility principle emphasizes the importance of creating value for all stakeholders, not just shareholders [9]. Good corporate governance calls for the company’s leadership to be ethical and for its governance structures to be designed to uphold the interests of both shareholders and other stakeholders, while maintaining compliance with legal and regulatory requirements [4]. The regulatory landscape surrounding ESG is evolving rapidly, with governments and international bodies increasingly mandating disclosures related to environmental impact, social responsibility, and governance practices. For example, the European Union’s Non-Financial Reporting Directive (NFRD) requires large companies to disclose non-financial information on how they operate and manage social and environmental challenges [30]. Although SMEs may not always be directly subject to such regulations, the ripple effects of these requirements often influence the entire supply chain. Therefore, SMEs that fail to align with ESG expectations risk losing business opportunities and facing challenges in maintaining contracts with larger corporations [31].

The other seven principles, namely smart risk management, ecosystem-based stakeholder engagement, productive business through innovation, long-term economic and social value creation, nuanced consumer choice and preferences, investor confidence and trust and attentive talent management, flow from the first three principles.

Smart Risk Management (P4) is increasingly recognised as critical to a company’s long-term sustainability and profitability. ESG factors, such as environmental risks, social unrest, and governance failures, can pose significant financial and operational risks. Effective risk management involves identifying, assessing, and mitigating these ESG-related risks [32]. Companies that anticipate and mitigate these risks through sustainable practices are more resilient in the face of environmental disruptions. For example, businesses that have invested in renewable energy and sustainable supply chains are better insulated from energy price volatility and supply chain disruptions [33]. There are also social risks such as poor or indifferent labour practices, non-existent or patronizing community relations, and neglect of customer satisfaction issues, which can impact business operations adversely leading to costly legal disputes, strikes, and consumer boycotts. All of them together with associated governance-related risks (fraud, corruption, and executive misconduct), can have a deleterious effect on a firm’s reputation and financial stability. What can help prevent such a negative outcome is the promotion of transparency, ethical behaviour, and accountability, all as part of a robust governance framework.

Ecosystem-based Stakeholder Engagement (P5) is essential for understanding and addressing the concerns of all stakeholders, such as employees, customers, suppliers, communities, and shareholders. Engaging with stakeholders ensures that a company’s ESG strategies are aligned with stakeholder expectations and contribute to long-term success [11]. The stakeholders form the nodes of a network-based ecosystem of the firm in question and awareness of the collaborative value of these networks demonstrates a pro-active way of engagement both in routine business activity with partners and in the wider community in which it operates

Productive Business through Innovation (P6) offers opportunities for business to find a competitive edge by integrating ESG into strategy making processes and in the efficient and effective allocation of capital to provide new products and services, new materials and even new industries to people on a planet where the environmental systems are in a crisis and whose social systems are stressed. This productivity-driven innovation perspective helps businesses to make smart choices about the future rather than simply looking at ESG as a process for monitoring and evaluating the past.

Long-term Economic and Social Value Creation (P7) is one of the primary reasons for ESG being crucial for businesses. Research has shown that firms with strong ESG performance tend to outperform their peers financially. This outperformance which creates or enhances measurable economic and social value for a firm is attributable to numerous factors, including enhanced risk management, operational efficiencies, and stronger relationships with stakeholders [34] and of course, innovation. For instance, a robust environmental strategy that reduces waste and energy consumption can lead to cost savings and new product or service opportunities, while socially responsible labour practices can improve employee morale and productivity, reducing turnover rates and associated costs [35].

Investor Confidence and Trust (P8) is critical for securing long-term investment. Governance practices that promote transparency and accountability are essential in building such trust. The perception of governance quality can be poor in the case of SMEs because of their relatively low credit ratings, lack of information, insufficient capital, and problems in attracting and retaining diverse talent. Since investors are increasingly integrating ESG factors into their investment decisions, they have begun to recognise that companies with poor ESG practices can incur significant risks, thereby undermining long-term profitability [36].

Nuanced Consumer preferences (P9) have shifted significantly in recent years, with a growing demand for products and services from companies that demonstrate a commitment to ethical and sustainable practices. A study by Nielsen (2018) [26] revealed that nearly 73% of global consumers are willing to change their consumption habits to reduce their environmental impact, and 81% strongly believe that companies should take action to help the environment. This shift in consumer behaviour places pressure on businesses to not only adopt but also to effectively communicate their ESG strategies. Businesses that proactively address these concerns can differentiate themselves in the market, attract a loyal customer base, and potentially command premium pricing for their products and services.

Attentive Talent Management (P10) (attracting and retaining talent) is increasingly being associated if not governed by ESG considerations. Employees, particularly millennials and Gen Z, prefer to work for organisations that align with their values and are high stake players in terms of their commitment to social responsibility and sustainability. Companies need to pay attention to such talent. Firms with h strong ESG credentials are therefore better positioned to attract top talent, enhance employee engagement, and reduce turnover, all of which contribute to a more productive and innovative workforce [37]. Large corporations, particularly those in developed markets, have made substantial efforts in embedding ESG principles into their corporate strategies as a result of pressure from investors who are incorporating ESG criteria into their decision-making processes, as well as by regulatory changes that mandate greater transparency and accountability [36].

These ten principles taken together echo the principles of strategic innovation and transformative management in different types of firms. The distinctiveness enabled by innovation is achieved by virtue of these firms operating as vehicles for transformation. Transformation, as opposed to routine change, is exemplified in the form of identifying new opportunities, developing new products, processes and business models, and in using technologies, money, talent and other resources to do so, creating appropriate platforms for their production, their development, promotion, sale and diffusion in the market place [5,38].

Many multinational corporations have established comprehensive ESG frameworks, including sustainability reporting, carbon reduction targets, and diversity and inclusion initiatives. For instance, companies like Microsoft, Unilever, and Tesla have become leaders in ESG performance, setting ambitious goals related to carbon neutrality, responsible sourcing, and governance practices [39,40]. These corporations are not only responding to regulatory requirements but are also proactively shaping the ESG landscape by adopting voluntary standards such as the Task Force on Climate-related Financial Disclosures (TCFD) and the Sustainability Accounting Standards Board (SASB) guidelines.

Tangible evidence of progress can be traced to the activities of e large corporations. Their SME counterparts are generally either at an earlier stage of ESG integration or face difficulties because of the e unique challenges in adopting ESG practices with limited resources, a lack of expertise, and the perception that ESG is primarily a concern for larger companies [41]. The field is changing as there is a recognition among many SMEs of the importance of ESG, not least because their position in the supply chains of large firms and the pressure they face from customers and employees who demand sustainable and ethical business practices.

3.3. The Importance of ESG for Small and Medium-Sized Enterprises (SMEs)

The importance of ESG practices holds particular relevance for SMEs in terms of both its application and the difficulties associated with its implementation among such firms. SMEs are also crucial players in the global economy, accounting for approximately 90% of businesses and more than 50% of employment worldwide [42]. According to the work of the OECD (2021) [43] and Wang et al., (2021) [44], SMEs account for 60–70% of carbon emissions worldwide, and together, they have a carbon footprint that is five times higher than that of their larger corporations. The higher number of smaller firms might be expected to have a higher negative carbon emission output although that is not a straightforward correlation. What it does show is their importance for socioeconomic progress does come at a cost to the wider economy and to society in terms of their impact on environmental sustainability [45,46,47].

Ecosystems are generally characterized by both large and small firms, and while many of them have thrived with unprecedented levels of economic growth lifting millions out of poverty, there has been an almost equal amount of pressure on the sustainability of those ecosystems. This in turn has produced variegated environmental effects for SMEs [48]. Unlocking the potential of sustainable finance solutions can therefore support regional ecosystems and their economic development, enabling SMEs to prosper in a beneficial economic, social and ecological environment [49].

As suggested above, the importance of ESG for SMEs is driven by their peculiar characteristics and vulnerabilities but also by the common factors, of the growing expectations from stakeholders, and legislative and structural changes. So why are ESG considerations especially critical for SMEs and how do these enterprises leverage ESG practices for sustainable growth and competitive advantage? Part of the answer lies in examining their role in supply chains, their resilience and ability to mitigate risks, access to finance and investment and compliance with regulatory changes and future-proofing.

3.3.1. Supply Chain Integration and Competitive Advantage

SMEs are integral to the workings of global supply chains. Since larger corporations have moved to the forefront of ESG compliance and reporting, they have begun to ensure that their SME supply chain counterparts also adhere to ESG requirements, with those SMEs that fail to meet these requirements risking the loss of business opportunities and even existing contracts with larger firms. Mitra and Bui (2024) [2] note that, companies like Unilever and Walmart have implemented strict ESG standards for their suppliers, affecting thousands of SMEs globally [50,51].

With the growing consciousness of sustainability and ethical practices among businesses and consumers, proactive SMEs differentiating themselves find y special premiums in terms of their competitive edge in in sectors such as food, fashion and consumer goods, where ethical sourcing, sustainable production, and social responsibility are key marketing and selling points [52].

3.3.2. Resilience and Risk Mitigation

The liability of smallness of SMEs due to their resource constraints makes them more exposed to risks associated with environmental and social issues than larger corporations. Typically, when we have climate-related events such as floods, storms, and heatwaves these phenomena can be catastrophic for t SMEs particularly in agriculture, manufacturing, and retail sectors. At the human level, labour disputes, health and safety concerns, and community relations are high risk issues making it difficult for SMEs to manage such eventualities effectively [41].

The adoption of ESG practices notably through the promotion of sustainable resource use, application of improve health and safety standards, and good employee relations together with transparent community involvement, can assist SMEs in building long-term resilience against environmental and social upheavals, not to mention the disruption caused in the markets because of these events. Adoption is only as strong as the implementation of strong governance practices, such as ethical leadership and transparent decision-making, which can enable SMEs to navigate regulatory changes in advance, thereby, avoiding legal liabilities.

3.3.3. Access to Finance and Investment

Access to finance is a well-known critical issue for many SMEs, not least because they often incur higher costs of capital and more stringent lending conditions, than larger firms. If ESG considerations are influencing the decisions of investors and financial institutions, and impact investors and funds are looking for SMEs that demonstrate strong ESG performance, then the SMEs have two contending issues they have to grapple with to make their mark – the money needed to adopt and implement ESG requirements and the ability to generate adequate levels of financial returns alongside positive social or environmental impact [53]. With widespread Standardisation of ESG reporting, it is likely that SMEs with robust ESG practices are more likely to obtain favourable terms from investors. Several banks are offering green or sustainability-linked loans, carrying lower interest rates to firms that meet certain ESG criteria [54]. It is, therefore, incumbent upon r SMEs to embed ESG practices in their management routines and structures to attract investors and lenders, thus improving their plans for growth through better access to capital and financial resources [2].

3.3.4. Regulatory Compliance and Futureproofing

The speed with which governments and international bodies are introducing new requirements for environmental impact, social responsibility, and governance practices, characterises the fast-evolving regulatory landscape. Generally, of interest to larger firms, there appears to be a growing trend towards broader applicability to include SMEs. The European Union’s Corporate Sustainability Reporting Directive (CSRD) is expected to extend ESG reporting requirements to both large and smaller firms [55].

A proactive application of ESG practices is likely to help SMEs to comply with future regulations, and avoid both crippling costs and disruptions resulting from non-compliance. Early alignment with ESG standards can help SMEs to future-proof their businesses against regulatory changes, and for marketing themselves, proactively as leaders in sustainability and responsible business practices. The outcome of such strategies can foster greater trust and loyalty among customers, suppliers, and other stakeholders.

3.3.5. Social Responsibility and Community Impact

If not a ‘given’ SMEs tend to have deep ties in their local communities, being embedded in the local social fabric, in ways that larger forms often do not. Consequently, their business practices can have a significant positive or negative impact on local employment, economic development, and community well-being. The adoption of ESG principles can enhance the positive aspect of the involvement of SMEs in their community, especially where environmental awareness levels are high [56].

Prioritising good labour-relations through investments in employee development, and engagement in community outreach to build strong, positive relationships with their workforce and the broader community is not of course restricted to SMEs. Larger firms are also likely to enshrine such practices in their activities. However, many SMEs are ‘born-local’, they are more likely to employ from the local community, and their markets may well be limited to the region in which they are located. This local advantage coupled with sound ESG strategies and practices could enhance the reputation of SMEs and also contribute to higher levels of employee satisfaction and retention, which are crucial for maintaining productivity and growth and consolidating their presence in the region. Environmentally and socially responsible SMEs are more likely to attract customers who prioritise ethical consumption, further driving business success.

We note that the increasing awareness of ESG issues can have variegated impact on large corporations and SMEs, across different countries and regions, because of the size issue referred to earlier and the ensuing questions on resources and governance.

3.4. From Theory to Practice the Current State of Play for SMEs and ESG Integration

Two OECD reports in 2021 and 2024 [41,57] highlights that although some SMEs are progressing in areas like energy efficiency, waste management, and employee well-being, many still find ESG frameworks and reporting requirements challenging to navigate. In the European Union, SMEs are increasingly involved in the ESG landscape, especially as part of supply chains for larger companies that require ESG compliance. However, SMEs in developing nations often encounter obstacles such as limited financial resources, low awareness, and insufficient regulatory backing when trying to adopt ESG practices.

Despite these challenges, there are notable examples of SMEs successfully integrating ESG into their operations. For example, the German company VAUDE, a family-run mountain sports equipment manufacturer, has become a sustainability leader by adopting robust environmental management, ensuring fair labor standards, and practicing transparent governance. A mini-case study of VAUDE illustrates innovative ESG implementation. Similarly, Divine Chocolate, a B Corp-certified SME based in the UK, has embedded ESG values by focusing on fair trade, ethical sourcing, and community development throughout its supply chain [58]. In Asia, TNG Investment and Trading JSC (TNG), a Vietnamese textile and garment company, has embraced ESG by cutting carbon emissions and energy use, prioritizing sustainable sourcing, and enhancing employee and community welfare - actions that have helped expand its market presence in Europe and North America [59].

Overall, the evidence points to an ESG approach for SMEs that is driven more by innovation and strategic interest than by mere compliance. The following mini-case study demonstrates how a small or medium-sized business can prepare for, plan, and execute ESG initiatives through an innovation-focused strategy.

Table 2.

Mini Case Study: Case Study: VAUDE – A Pioneer in ESG Integration among SMEs.

|

Introduction

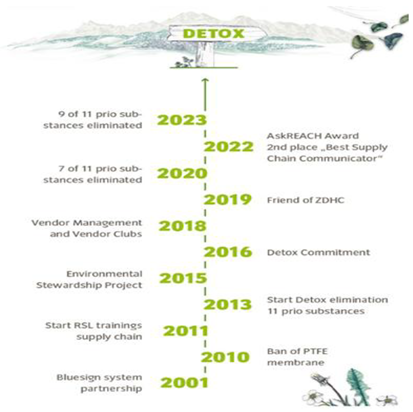

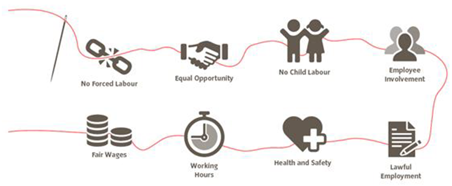

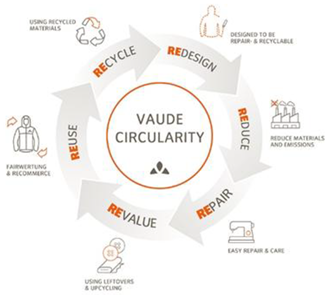

VAUDE, a German outdoor clothing company owned by a family, is a prime example of how small and medium-sized enterprises (SMEs) can successfully incorporate ESG (Environmental, Social, and Governance) principles into their operations. Since its founding in 1974, VAUDE has become internationally recognised not just for its high-quality, technologically advanced products, but also for its strong dedication to sustainability and social responsibility. The company’s approach to ESG provides a useful case study, showing how SMEs can use ESG practices creatively to boost their competitiveness, lower risks, and make a positive impact on both society and the environment. What constitutes Vaude’s approach to ESG adoption and implementation. Environmental Stewardship (‘E’ in ESG) VAUDE places environmental sustainability at the core of its business strategy. The company has made significant efforts to minimize its environmental impact throughout its operations. In 2023 and 2024, VAUDE increased its commitment to achieving climate neutrality by advancing science-based targets. It actively worked to lower its carbon emissions by improving energy efficiency and increasing the use of renewable energy at its production sites, such as installing more solar panels and adopting advanced energy management systems. These initiatives played a major role in helping VAUDE reach climate neutrality, as confirmed by the Science Based Targets Initiative (SBTi) in line with the 1.5 °C target [60]. Innovation and Circular Economy Recently, VAUDE has prioritised the circular economy, aiming for 90% of its products to be made from recycled or renewable materials by 2024. This goal is supported by advances in product design, such as using 3D printing to manufacture robust and recyclable outdoor gear, which helps minimize waste and encourages the reuse of materials. In 2023, VAUDE was honored with the International Design Award “Focus Meta” for the innovative and forward-thinking design of its “Novum 3D” backpack [61]. The company also adopted the Green Button certification, which verifies that its products meet strict environmental criteria, further demonstrating its dedication to sustainable product lifecycle management [62]. Transparency and Robust Management Beyond improving energy efficiency, VAUDE has established a comprehensive environmental management system that oversees every stage of its products’ lifecycle. The company emphasizes responsible sourcing, Utilising materials like organic cotton, recycled polyester, and other environmentally friendly textiles. VAUDE also extends its high environmental standards to its supply chain, working closely with suppliers to ensure they follow similar sustainability practices. This integrated approach has earned VAUDE several certifications, including the European Union’s Eco-Management and Audit Scheme (EMAS) and the bluesign® system, which is Recognised as the world’s strictest textile standard for environmental and consumer protection [63] .  Figure 1 : VAUDE Roadmap to Detox; VAUDE has been working with bluesign® since 2001. (Source: csr-report.vaude.com) The ‘S’ in Vaude’s ESG: Social Responsibility VAUDE complements its ‘E’ strategy with an equally comprehensive sense of dedication to social responsibility initiatives, including ethical business practices and community engagement. The company’s social policies are built around the principles of fair labour, diversity, and inclusion. VAUDE ensures that all its employees work in safe and healthy conditions, with fair wages and access to benefits such as health insurance and pension plans. Additionally, the firm is committed to gender equality within its workforce, with women holding a significant proportion at 47% of management positions [64].  Figure 2 : VAUDE’s Social Principles (Source: csr-report.vaude.com) The Socially Responsible Community VAUDE goes beyond its own operations to promote social responsibility by actively involving its suppliers and the wider community. The company works with the Fair Wear Foundation, an independent group focused on improving labor conditions in the textile sector. Through this collaboration, VAUDE ensures its suppliers adhere to strict standards, such as banning child labor, forced labor, and discrimination, and maintaining safe working environments [65]. In 2024, VAUDE strengthened its fair wage policies and expanded employee benefits, furthering diversity and inclusion within its workforce. The company also created the VAUDE Academy, which provides sustainability training for employees and stakeholders, encouraging ongoing learning and engagement [66]. VAUDE supports local communities by initiating and backing projects that improve education and healthcare in disadvantaged areas. For example, in 2023, the company launched the “Rethink! Circular Product Design” initiative, which not only advances sustainable product innovation but also helps drive community-based sustainability efforts. These activities reinforce VAUDE’s reputation as a socially responsible business and help build trust and loyalty among its stakeholders [67].  Figure 3 : VAUDE’s Circular business model (Source: csr-report.vaude.com) Governance and Ethical Leadership: The ‘G’ in Vaude’s ESG Governance forms the foundation of VAUDE’s ESG approach, ensuring that environmental and social initiatives are seamlessly integrated into the company’s overall operations. The governance system at VAUDE is marked by openness, accountability, and principled leadership. The board of directors includes independent members who oversee operations and make sure decisions benefit all stakeholders - employees, customers, suppliers, and the community. Additionally, VAUDE has implemented a code of ethics that shapes its business conduct, focusing on honesty, fairness, and responsibility. This is further supported by anti-corruption measures and clear procedures for reporting and addressing unethical actions. The governance framework has been strengthened by adding more independent board members and updating the code of ethics to include stricter anti-corruption rules and improved reporting mechanisms for misconduct [68]. Being transparent VAUDE’s dedication to ethical governance is also evident in its transparent reporting. The company’s sustainability reports are now more detailed and open, offering comprehensive information about ESG achievements and progress. By adopting standardised reporting systems like the Global Reporting Initiative (GRI) and the Higg Index, VAUDE ensures its ESG disclosures are consistent and trustworthy. This level of transparency not only strengthens stakeholder trust but also supports better decision-making and strategic planning within the organisation [69]. Reaping Acclaim and Rewards The company’s strong commitment to ESG has improved its efficiency and competitiveness, earning it significant recognition. VAUDE has received several awards for its sustainability work, including the German Sustainability Award, which honors companies making outstanding contributions to sustainable development. In 2024, VAUDE was Recognised as Germany’s most sustainable textile company in two categories, highlighting its excellent governance and sustainable business strategies. This proactive ESG approach has attracted environmentally and socially conscious customers and investors, helping the company grow its presence in Europe and North America [61]. Moreover, VAUDE’s advocacy for environmental protection, such as promoting restrictions on PFAS chemicals, demonstrates its leadership in advancing broader regulatory and environmental standards. Participation in initiatives like the German Partnership for Sustainable Textiles and the Science Based Targets Initiative further boosts the company’s credibility and independence, establishing it as a trusted name in sustainability [69]. By focusing on sustainability, ethical leadership, and social responsibility, VAUDE serves as a model for other SMEs aiming to strengthen their long-term success and contribute to global sustainability objectives. General Observations Through its commitment to environmental stewardship, social responsibility, and strong governance, VAUDE has improved its own business operations while generating a positive impact on its stakeholders and the wider environment. They can also be looked at as conscious attempts to re-design the organisation through innovative practices leading a transformation of its organisational capacity to accommodate ESG while embracing and implementing the key concept of ‘value circularity’. This case study highlights the potential for SMEs to lead in ESG practices, demonstrating that sustainability and ethical business practices can be powerful drivers of resilience, innovation, and long-term success. Following Vaude’s example SMEs can start by identifying material ESG issues, engage stakeholders, optimise resource allocation, ensure transparency, get involved in supply chains, leverage existing and new technologies for ESG-led innovation, and act as gatekeepers of regulations and standards. The case study also highlights how ESG can be a spur for innovation subject to the business adopting a clear strategy to map ESG across all its activities. It is also the case that ESG’s adoption and successful implementation is strongly dependent on two key resources, more than others – technological and human. An adequate (defined according to specific micro contexts and type of business) technology platform which accommodates regular iteration and revamping coupled with skills and capabilities (managerial, technical, networking) could pave the way for competitive positioning of firms. Details are discussed later in the paper. By systematically addressing these factors, SMEs can embed ESG into their core strategy, enhance their competitiveness, and contribute positively to society and the environment. |

Source: Adapted from a preliminary set of secondary sources only drawn mainly from materials dated 2023 to 2024 and available on their web site. A full list is cited in the references.

3.5. Global and Regional Forms of ESG Adoption

The extent of ESG adoption varies widely across countries, with some regions making more progress than others. Europe is generally seen as leading in ESG, thanks to strict regulations and strong demand from investors and consumers for sustainable business practices. This leadership aligns with Europe’s economic model, which emphasizes social contracts. The EU’s Sustainable Finance Disclosure Regulation (SFDR) and Corporate Sustainability Reporting Directive (CSRD) are establishing rigorous standards for ESG transparency and accountability, impacting both large companies and SMEs [55]. Nordic countries are especially noted for their early and thorough integration of ESG across industries, supported by a strong tradition of sustainability and social responsibility [70].

In the United States, ESG integration has historically lagged behind Europe, but there has been rapid progress recently, driven by investor influence and the growing role of ESG in company valuations. The U.S. Securities and Exchange Commission (SEC) is also moving toward stricter ESG disclosure rules, reflecting a broader recognition of ESG’s impact on financial outcomes [71]. However, the U.S. approach remains fragmented, with significant differences across industries and states, and recent reversals in or even abrogation of some commitments.

By contrast, ESG adoption in Asia is advancing more slowly, though there are important exceptions. Japan has made notable progress, especially in corporate governance and sustainability, guided by government policies like the Stewardship Code and Corporate Governance Code [72]. China is also placing greater emphasis on ESG, particularly in relation to its climate ambitions and the integration of green finance into its economic plans [73]. Vietnam, as a fast-growing economy, has demonstrated increasing commitment to sustainability, as shown by its ratification of the Paris Agreement and the launch of the National Green Growth Strategy [74]. Still, many Asian countries face obstacles such as inconsistent regulations, limited awareness, and varying levels of business commitment.

Globally, governments are increasingly acknowledging the importance of ESG and are introducing policies to help businesses, especially SMEs, integrate ESG into their operations. These policies include regulatory requirements, financial incentives, capacity-building programs, and public-private partnerships. However, we do not find that the recognition of ESG as a necessary code of practice is even acceptable across countries and sometimes even within regions. This macro-level unevenness poses problems for firms especially those tied into global supply chains not least because they can affect the flow of goods, appropriate types of certifications, and prices.

The following sections discuss how governments worldwide are encouraging ESG adoption, with a focus on the unique challenges faced by SMEs.

3.5.1. Regulatory Frameworks and Reporting Requirements

A key way governments support ESG adoption is by creating and enforcing regulations that require ESG reporting and compliance. These rules aim to boost transparency and accountability, ensuring companies disclose their environmental, social, and governance impacts. For example, the EU’s Non-Financial Reporting Directive (NFRD) requires large firms to report non-financial ESG information, such as environmental performance, social responsibility, and governance. The upcoming CSRD will expand these requirements to cover more companies, including some SMEs [55]. According to the European Commission, from 2026, the CSRD will apply to SMEs listed on regulated European markets that meet at least two of these criteria: a balance sheet total of at least EUR 4 million, net turnover of at least EUR 8 million, and an average of 50 or more employees during the year. The CSRD will require detailed, standardised ESG reporting, helping SMEs align with global standards and improving their access to international markets.

Similarly, in the U.S., the SEC is moving toward mandatory ESG disclosures for publicly listed companies, which is expected to affect supply chains and, consequently, SMEs working with larger corporations [71]. Such regulatory frameworks help level the playing field, motivating SMEs to adopt ESG practices that meet the expectations of larger firms and investors.

In Asia, countries such as Japan and South Korea have launched comparable initiatives. Japan’s Corporate Governance Code encourages firms to address ESG issues and report on sustainability, and while it mainly targets large firms, it also indirectly influences SMEs by fostering a business environment where ESG is prioritised [72].

3.5.2. Financial Incentives and Access to Capital

Governments are also offering financial incentives to promote ESG adoption, especially among SMEs. These incentives include grants, tax benefits, and access to low-interest loans for projects that support environmental sustainability, social development, or better governance. For instance, the EU’s Green Deal Investment Plan provides substantial funding to help businesses transition to sustainable practices. SMEs can access grants and loans for energy efficiency, sustainable product development, and other ESG-related projects [75]. The EU also supports green bonds and other financial tools that give SMEs access to capital specifically for ESG initiatives.

The Singapore government’s Sustainable Loan Grant Scheme encourages banks to provide loans linked to ESG performance targets, offering SMEs more favorable terms if they commit to improving ESG outcomes [76]. In the UK, the government supports SMEs developing low-carbon technologies through the Clean Growth Fund, which helps bridge the gap between innovation and commercialisation and contributes to national climate goals [2,77].

3.5.3. Capacity Building and Education

In recognition of the lack the expertise and resources to implement ESG effectively by SMEs, governments are investing in training and support programs. These include workshops, advisory services, and toolkits to guide SMEs in integrating ESG into their operations.

The German government supports the Mittelstand (medium-sized and smaller businesses) through initiatives that enhance ESG capabilities. In partnership with industry associations, Germany offers training on sustainability, energy efficiency, and governance, helping SMEs understand ESG’s benefits and providing practical implementation advice [78]. Similarly, Canada’s federal government launched the Canadian Business Resilience Network, which offers resources to help SMEs integrating ESG principles while attempting to recover from the fallout of the COVID-19 pandemic. The network’s provision of webinars, toolkits, and consulting to help SMEs develop sustainable business models is predicated on this twin objective of integration and recovery [79].

3.5.4. Public-Private Partnerships and Collaboration

Governments also promote ESG adoption among SMEs through public-private partnerships (PPPs), which combine the strengths of both sectors to support sustainable business practices.

In the Netherlands, the government has joined with major corporations and financial institutions to form the Dutch Sustainable Growth Coalition, which helps SMEs access resources, expertise, and networks for ESG adoption [80]. The coalition assists SMEs in building sustainable supply chains, improving energy efficiency, and enhancing social responsibility.

The Chinese government collaborates with international organisations like the United Nations Development Programme (UNDP) to support ESG adoption among Chinese SMEs. These partnerships focus on providing SMEs with the knowledge and tools needed to meet global sustainability standards, especially in manufacturing and agriculture [81].

These laudable policy initiatives do not necessarily support or cohere with the daily problems SMEs face to compete or even survive. Rather, there is the distinct possibility of some of these measures can be seen as additive burdens adding to the cost base of struggling SMEs, and reducing their chances of remaining competitive.

4. Discussion

Our analysis highlighted the range and scope of ESG policies and principles together with the strategic and operational dimensions of adoption and implementation of ESG in business practice. We discuss our findings here alongside the generation of ideas and the creation of a pathway to developing a framework for ESG implementation for and by SMEs.

SMEs encounter distinct challenges and opportunities when integrating ESG principles into their operations. Unlike large corporations, which typically have greater resources and infrastructure to address ESG matters comprehensively, SMEs must manage these issues with more limited means. Nevertheless, adopting ESG practices can offer SMEs significant advantages, such as better access to funding, a stronger reputation, and enhanced resilience. This raises the question: what steps can SMEs take, and how can their progress be evaluated? Below, we introduce a framework designed to guide SMEs in adopting ESG practices. The design and development of the framework is informed by the key themes drawn from our review of the literature.

4.1. Towards the Development of a Framework for Adopting ESG

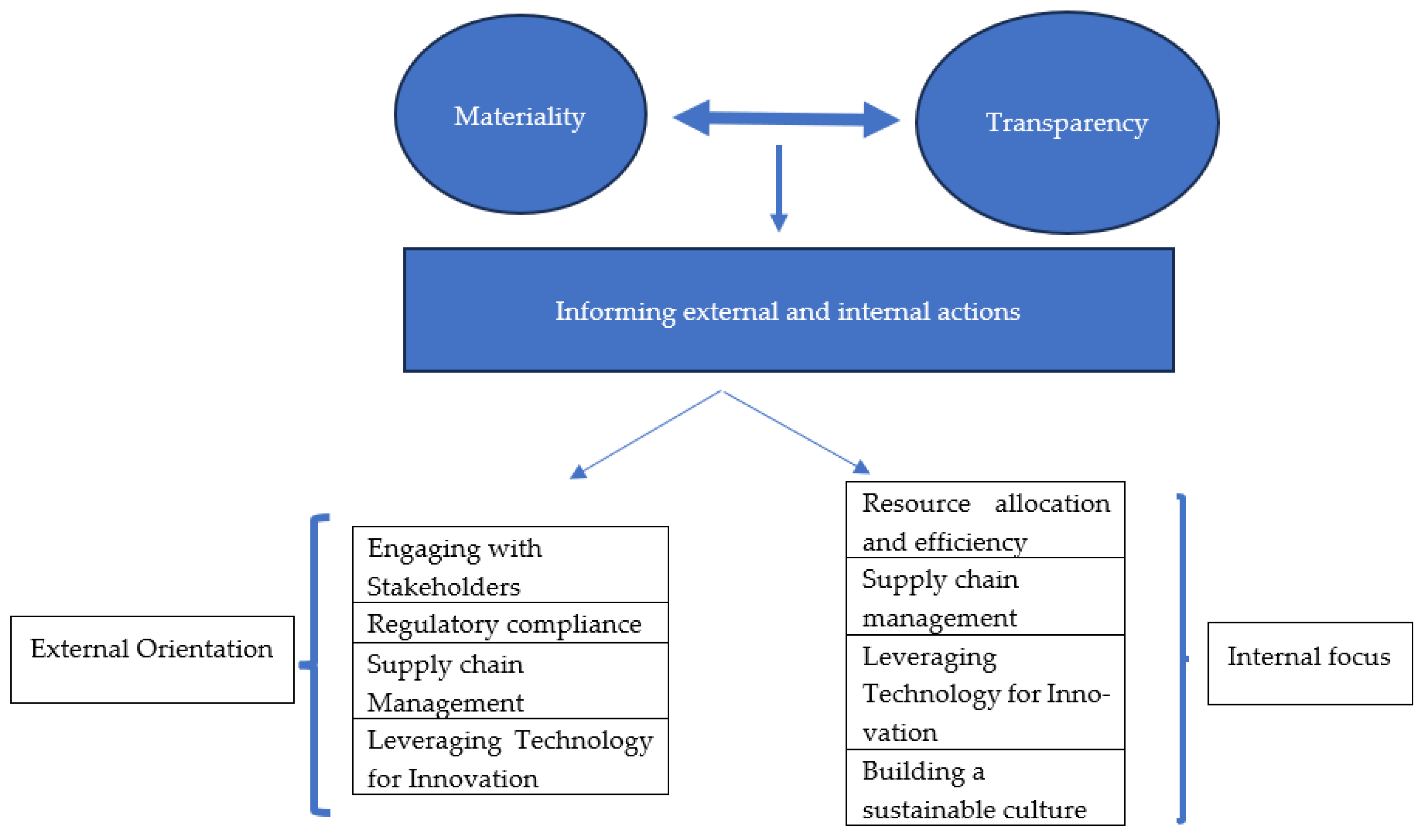

Based on our findings from both the academic and professional literature we believe that to manage ESG effectively in a highly volatile and litigious environment alongside the need to address critical economic and social imperatives driven by environmental and social change SMEs need to focus on eight key factors (F) – Materiality, Stakeholder Engagement, Efficient Resource Management; Regulatory Compliance; Supply Chain Management, and Transparency. As stated earlier this discussion is organised to reflect the meta themes derived from the thematic analysis of the combined academic and professional industry literature.

FI: Materiality refers to the what specific and relevant ESG factors apply to a company’s operations, networks of stakeholders, the use of its resources and its overall business strategy. Specificity and relevance are metrics for materiality in a business, and it is, therefore, crucial for owner-managers and SME management teams to identify which ESG factors are considered to be the most material to their business. This involves assessing and mapping the environmental, social, and governance questions that are most likely to have differential impact on the firm’s s financial performance, reputation, and stakeholder relationships. A manufacturing SME might find that waste and energy efficiency management to be highly material due to the nature of its operations because they affect both inputs and outputs. Effective energy management is dependent on the use of smart technologies and optimum use of resources while waste management is both a corollary of effective energy management and outputs which generate waste. A service-oriented SME, such as a restaurant or a social media firm can be expected to prioritise social factors like employee well-being, customer feedback and data privacy. Understanding materiality helps SMEs focus their ESG efforts on the areas that matter most, ensuring that their resources are used effectively [82].

F2: Engaging with stakeholders, such as employees, customers, suppliers, investors, and the local community, is a critical aspect of managing ESG for SMEs. Stakeholders are increasingly concerned with how companies manage ESG issues, and their expectations can drive change within the organisation. SMEs need to actively engage with their stakeholders to understand their concerns and expectations related to ESG. This engagement can take various forms, including surveys, focus groups, direct communication, and partnerships. By involving stakeholders in the ESG process, SMEs can ensure that their strategies align with stakeholder values, which can enhance trust and loyalty, as well as improve the company’s reputation [83].

F3: Resource Allocation and Efficiency. Optimally allocating resources is a major challenge for SMEs when implementing ESG practices. Unlike larger companies, SMEs often have limited financial and human resources, so it’s important for them to pursue ESG initiatives in a practical and efficient way. They can begin by focusing on affordable, high-impact actions, such as improving energy efficiency, reducing waste, or introducing basic governance measures like a code of ethics, which typically require minimal investment. SMEs can also seek out partnerships, grants, and government programs that provide support for ESG efforts, helping to reduce associated costs [30].

F4: Regulatory Compliance and Anticipation. With governments worldwide introducing stricter ESG-related regulations, compliance has become increasingly important for SMEs. These rules may cover areas like environmental protection, labor rights, corporate governance, and transparency. SMEs must stay updated on current and upcoming regulations relevant to their sector and region to avoid legal issues and penalties. Beyond simply complying, SMEs should try to anticipate future regulatory trends, often with the support of industry federations. Proactively adapting to new regulations can help SMEs become industry leaders and gain competitive advantages. For example, adopting sustainable practices early can better position an SME to meet future customer and regulatory expectations [41]. However, acting as a regulatory gatekeeper is often costly and time-consuming, highlighting the importance of industry bodies and federations. These organisations, with government support, should enhance their capacity to help SMEs innovate and avoid pitfalls in ESG adoption, planning, and execution.

F5: Supply Chain Management. Managing supply chains is especially important for SMEs, particularly those involved in global supply networks. Large companies are increasingly requiring their SME suppliers to comply with ESG standards, including environmental regulations, labor rights, and good governance. SMEs should assess their supply chains to ensure alignment with ESG principles. This may involve conducting supplier due diligence, adopting sustainable sourcing, and working collaboratively with suppliers to improve ESG performance. A responsible supply chain not only reduces risks but also boosts the SME’s reputation and appeal to potential partners and customers [84].

F6: Transparency is fundamental to effective ESG management. SMEs should aim to be open about their ESG activities, challenges, and progress, both internally (with employees and management) and externally (with customers, investors, and regulators). While comprehensive ESG reporting can be demanding, SMEs can start by reporting on the most relevant ESG metrics for their business. As their ESG practices mature, they can expand their reporting scope. Being transparent helps build stakeholder trust, enhances reputation, and may improve access to funding [82].

F7: Building a Sustainable Culture. For ESG to have a lasting impact, it must be embedded in the company’s culture. This means integrating ESG considerations into daily decision-making and reflecting them in company values and behaviors. Creating a sustainable culture involves educating employees about ESG, promoting responsible actions, and tying ESG goals to performance measures. Leadership is crucial, SME leaders need to champion ESG, and set the standard for the organisation. By fostering a culture of sustainability and responsibility, SMEs can ensure their ESG practices endure over time [85].

F8: Leveraging Technology for Innovation can empower SMEs to implement effective and leading ESG practices. Digital tools, especially AI, can help monitor and reduce energy use, manage supply chains, and ensure regulatory compliance. SME federations and support services could facilitate network models that share information on ESG technology deployment and trends. Innovation is also key for developing new products, services, and business models that align with ESG goals. SMEs that focus on sustainability-driven innovation can access new markets and attract customers who value ethical practices. Additionally, technology can streamline ESG reporting and data management, making it easier for SMEs to track and communicate their progress [86].

Materiality and Transparency (F1 and F6) constitute abstract concepts allowing for the consideration of significant strategic decisions for managing externally-oriented pressures (F2 and F4) supplemented by internally-focused operational considerations (F3 and F7), with inevitable overlaps in practice, for tactical purposes, across certain key factors (F5 and F8) as captured in Figure 2 below. These factors have to be considered against the constraints and barriers faced by SMEs as discussed below.

A framework is sufficiently robust if it is capable of identifying and using an appropriate set of metrics to assess, evaluate (ex-ante and post-hoc), report and improve ESG implementation.

4.2. Key Metrics for SMEs in Recording and Reporting ESG Issues

To successfully manage, document, and disclose their ESG (Environmental, Social, and Governance) performance, SMEs must select and utilize appropriate metrics. These indicators, both quantitative and qualitative, demonstrate a company’s dedication to responsible and sustainable business conduct. While the exact metrics will differ based on the sector and the ESG topics most pertinent to each business, there are several core metrics SMEs should consider for ESG tracking and reporting.

4.2.1. Environmental Metrics

Environmental indicators are vital for evaluating a company’s effects on natural resources and the environment. SMEs should prioritise metrics that align closely with their activities and sector. Common environmental metrics include:

- (a)

- Carbon Footprint (CO2 Emissions): This measures the total greenhouse gases (GHGs) the company emits, both directly and indirectly, typically reported in metric tons of CO2 equivalent. SMEs should account for scope 1 (direct), scope 2 (indirect from purchased energy), and, where possible, scope 3 (indirect across the value chain) emissions [87].

- (b)

- Energy Consumption: This tracks the company’s total energy use, usually in megawatt-hours (MWh) or gigajoules (GJ). Reporting the share of energy from renewable sources as a percentage of total consumption is also recommended [88].

- (c)

- Water Usage: This records the total water consumed, generally in cubic meters. For water-intensive sectors like agriculture or manufacturing, water intensity (usage per unit of output) is also a useful measure [82].

- (d)

- Waste Management: This tracks the total waste produced, the proportion recycled, and hazardous waste generated. Reporting waste diversion rates (percentage of waste kept out of landfills via recycling or composting) is also valuable [89].

- (e)

- Resource Efficiency: These metrics assess how efficiently the company uses resources such as raw materials, energy, and water. For example, resource intensity might be measured as the amount of raw material used per unit of product [90].

4.2.2. Social Metrics

Social indicators evaluate the company’s influence on employees, customers, suppliers, and the wider community, helping SMEs assess their social responsibility and stakeholder well-being. Key social metrics include:

- (a)

- Employee Health and Safety: This includes indicators like the number of workplace accidents, lost-time injury frequency rate (LTIFR), and hours of health and safety training per employee [91].

- (b)

- Diversity and Inclusion: Metrics here may include the percentage of women in the workforce and management, as well as workforce diversity by ethnicity, age, and other factors. They can also track diversity program implementation and employee satisfaction with inclusion efforts [86].

- (c)