Submitted:

03 September 2025

Posted:

05 September 2025

You are already at the latest version

Abstract

This article investigates the complex interplay between the Banking Union (BU), Capital Markets Union (CMU), and Economic Adjustment Programmes (EAPs) in shaping the financial sectors of Greece and Cyprus, with a focus on core–periphery divergences within the euro area. Drawing on a comparative, mixed-methods approach, the study integrates quantitative analysis of non-performing loan (NPL) ratios, indicators of market concentration, and sectoral employment with qualitative examination of policy frameworks, legal instruments, and institutional reforms. The findings reveal that EAP-driven restructuring, in conjunction with supranational financial integration initiatives, has led to unprecedented consolidation of banking assets and the proliferation of private debt investors in the periphery. These processes have deepened dependency and structural inequalities between core and peripheral member states, as evidenced by the dominance of a few major credit institutions and the transfer of distressed assets to international investors. The research situates these developments within the broader theoretical context of financialization and dependency, highlighting the mechanisms through which EU crisis management and market-oriented reforms have reconfigured the institutional landscape, rein-forced core–periphery asymmetries, and shaped the trajectory of economic governance in the euro area. The article concludes that while BU and CMU reforms have contributed to financial stability, they have also entrenched patterns of uneven development and de-pendency, raising critical questions about the distributive consequences of European financial integration.

Keywords:

core-periphery development

; economic adjustment programmes

; Banking Union

; Capital Markets Union

; bank-based and capital markets-based capitalism

1. Introduction

The aftermath of the 2008 international financial crisis marked a pivotal transformation in the governance of the Economic and Monetary Union (EMU), giving rise to a new architecture of economic oversight and intervention (Scharpf 2021; De Grauwe & Ji, 2020; Lapavitsas et al. 2018). Central to this transformation was the imposition of Economic Adjustment Programmes (EAPs) on Cyprus, Greece, Ireland, and Portugal—an unprecedented policy experiment in the European Union’s history (Alcidi et al. 2016; Scharpf 2021)1. These programmes, enforced through Memoranda of Understanding (MoUs), mandated comprehensive structural reforms as conditionalities for financial assistance, targeting fiscal, financial, labor, and product markets (Zeitlin & Vanhercke 2014; Costamagna 2012). The alternative—debt restructuring—was largely precluded by creditor reluctance (Gianviti et al. 2010).

The literature has extensively documented the social and economic consequences of these EAPs, particularly the implementation of austerity measures that prioritized fiscal and financial consolidation over social protection (Costamagna 2012; Schwartz 2014). Despite more recent EU efforts to strengthen social objectives within the European Semester (Zeitlin & Vanhercke 2018; Miro et al. 2023), persistent and even widening inequalities remain evident across the euro area while contractionary monetary policy and income inequality are found positively related (Creel & Herradi 2024; Furceri et al. 2018; Baiardi & Morana 2018). Large-scale bank bailouts across the Eurozone to maintain financial stability and market confidence have led to a decline of competition in the banking sector, ultimately reducing overall social welfare (Martino & Perini, 2025). Scholars have characterized the EAPs as instruments of “competitive impoverishment” (Avlijaš et al. 2021), whereby EU institutions and the IMF imposed intrusive reforms that eroded welfare states and decentralized collective bargaining, particularly in the periphery (Schulten & Müller 2012; Rathgeb & Tassinari 2022). This strategy, influenced by Germany’s post-unification wage restraint and competitiveness agenda (Johnston, 2021), has been critiqued for subordinating social policy to the imperatives of market flexibility and fiscal discipline (Hassel et al. 2020).

The study of core-periphery patterns in the framework of the European Union and monetary union is substantial in macroeconomic literature (Gräbner et al. 2020) including heterogeneity and diversity in economic growth regimes (Höpner and Lutter 2018), comparative capitalism literature (see Johnston and Regan 2021 and 2016) and the theory of endogenous optimal currency areas (see Campos and Macchiarelli 2021; Bayoumi and Eichengreen, 1993). Campos and Macchiarelli 2021 go as far as to suggest the categorization of an extended periphery (Finland, Ireland, Norway, Portugal, Switzerland, Sweden, Greece), a hard-core group of countries (Austria, Belgium, Germany, and the Netherlands) and an intermediate group (Denmark, Spain, UK, France, and Italy). Weissenbacher (2019) has explicitly argued that the core—periphery in a global and European capitalist system is very persistent.2 Our theoretical approach is connected to the above stated macroeconomic literature while it also draws upon the distinction between core and periphery countries from a dependency perspective, a framework in which the centrality or interdependence of the notions of center (or core), periphery and semi periphery related to socioeconomic development and dependency of states and regions of the world is pivotal. This approach distinguishes between core, periphery, and semi-periphery, focusing on patterns of economic development and dependency (Rama & Hall, 2021; Weissenbacher, 2019). This theoretical tradition argues that mechanisms of exploitation and surplus transfer include unequal exchange (Amin, 1988), the structure and terms of trade (Prebisch, 1949), foreign debt payments (George, 1986), and foreign direct investment. As Petras and Veltmeyer (2007, p. 22) observe, “through a combination of these and other mechanisms, a substantial part of the social product is extracted from the periphery and transferred to the centre, where it is converted into capital, leaving workers and producers on the periphery to bear the heavy social costs of this “development”. In this article, we conceptualize EAPs as partnerships that entail the submission of recipient states to lender states, effectively reproducing unequal relations under a new guise (in a similar vein with Petras and Veltmeyer, 2007). In the context of the euro area, this manifests in the imposition of EAPs and the supranational governance of financial integration initiatives such as the Banking Union (BU) and the Capital Markets Union (CMU). These projects, although still developing, serve not only to stabilize markets but also to discipline peripheral economies, often reproducing patterns of dependency and reinforcing the structural advantages of core member states (Lapavitsas, 2019; Parker & Tsarouhas, 2018). We use these lenses to interrogate the contemporary imperial presence of certain states within organisations, particularly in the context of crisis and shifting power relations. As Elen Meiksins Wood argues, capitalist expansion increasingly relies on the imposition of economic imperatives and market compulsions, rather than direct colonial rule, and financial instruments—aid, loans, investments, and debt relief—are used to enforce market discipline and manipulate capitalist operations (Wood, 2003). The literature on financialization further sharpens this analysis by highlighting the growing dominance of financial motives, markets, and actors in shaping economic and social outcomes (Epstein, 2005; Stockhammer, 2013). Contemporary finance in its most innovative forms, functions as an extractive sector—extracting prospective value and subsequently departing, often leaving significant economic disruption in its wake (Sassen, 2017). Financialization is understood as a transformation in the accumulation regime, wherein profits are increasingly generated through financial channels rather than productive investment, exacerbating systemic risk and amplifying core–periphery disparities. In the euro area periphery, the proliferation of non-performing loans, the entry of private debt investors, and the restructuring of national banking sectors are emblematic of this broader shift.

This paper examines the impact of the interplay between two recent, in development, EU initiatives—the BU and the CMU—and the EAP-driven reforms in the financial sectors of the euro area periphery. Focusing on Greece and Cyprus, and drawing comparisons with advanced economies such as Germany and France, the analysis adopts a comparative approach to conceptualize core and periphery countries in terms of uneven development (Parker and Tsarouhas, 2018; Amin, 2019; Petras and Veltmeyer, 2007). The persistence and intensification of uneven development and heterogeneity within the EMU are highlighted (Lapavitsas, 2019; Laffan, 2016), with core countries exploiting peripheral states amid ongoing structural reconstitution of capitalism (Wallerstein et al., 2013; Gouliamos, 2014; Denk and Cournède, 2015; Magone et al., 2016). This article conceptualizes the interplay between EAPs, BU, and CMU as a process that both reflects and intensifies uneven development in the euro area. The analysis foregrounds the ways in which supranational crisis management and financial integration reforms have reconfigured the institutional landscape of peripheral economies, consolidating financial power, deepening dependency, and perpetuating structural inequalities between core and periphery.

The first section provides an alternative interpretation of the evolution of the CMU, examining its relationship to the expansion of Private Debt Investors (PDIs) in the Eurozone periphery. It presents evidence of the growing dominance of PDIs, who have acquired significant banking assets—particularly non-performing loans tied to Greek and Cypriot properties.3 The second section critically assesses the development of the BU and the EAP-driven restructuring of the banking systems in Cyprus and Greece, highlighting the unprecedented concentration of wealth and power in credit institutions. These interlinked developments are contextualized within the broader framework of the CMU.

2. Materials and Methods

We employ a comparative, mixed-methods research design to investigate the interrelation of the Banking Union (BU), Capital Markets Union (CMU), and Economic Adjustment Programmes (EAPs) in shaping the financial sectors of Greece and Cyprus, with reference to broader euro area core–periphery dynamics. The methodology is structured to capture both macro-level policy shifts and micro-level sectoral outcomes, integrating quantitative empirical analysis with qualitative institutional and critical inquiry. To obtain a more comprehensive picture, we compare the course of the periphery, Greece and Cyprus with those of Germany and France, two core euro area countries not subjected to EAPs. Our goal is to identify whether the financial structural reforms have led to a change in the balance between the periphery and the core.

2.1. Quantitative Empirical Analysis

The quantitative component is grounded in the analysis of sectoral data from the European Central Bank (ECB) data portal-Banking Structural Financial Indicators.4 Key indicators analyzed include:

- Non-performing loan (NPL) ratios (2008–2022), transactional data on the sale and management of NPLs portfolios, including the entry and activity of PDIs to consider the impact of the CMU.

- Market concentration metrics, specifically the share of the five largest credit institutions-CIs in total banking assets (CR5, domestic), sectoral employment and branch data (specifically the number of offices) to evaluate trends in asset consolidation and document the consequences of restructuring and downsizing with a focus on the periphery’s pronounced contraction.

These data are analyzed across time and comparatively, enabling identification of structural divergences between core and periphery, as well as the timing and magnitude of sectoral changes linked to BU, CMU, and EAP interventions.

2.2. Qualitative Policy and Institutional Analysis

The study undertakes a qualitative review of:

- EU-level policy frameworks and legal instruments (BU, CMU).

- Memoranda of Understanding (MoUs) and national legislation underpinning EAPs in Greece and Cyprus, with particular attention to financial structural changes

This analysis is complemented by a critical reading of official communications, legislative texts, and financial press coverage to trace the rationales, implementation processes, and contested outcomes of policy interventions. We present and analyze the content of the aforementioned reforms as identified in the original Economic Adjustment Programme documents and official reviews and as per the European Stability Mechanism (ESM) Programme Database. To identify financial reforms, we used the official classification of the ESM (Conditionality Dashboard), where these are classified under the category of financial sector policies for Cyprus (under ESM) and Greece (EFSF and ESM Programmes).5 Financial sector policies reforms that did not fall under this category were not considered. The secondary sources retrieved for analysis include European Economy Occasional Papers on EAPs.

Quantitative and qualitative findings are integrated through a process of critical-interpretive synthesis, allowing for a nuanced assessment of how macro-level EU initiatives, namely the CMU and the BU and crisis-driven national reforms under EAPs have interacted to reshape the financial landscape of Greece and Cyprus. Special attention is paid to the sequencing of events, policy feedback loops, and the reproduction of core–periphery divergences.

3. The Capital Markets Union and Private Debt Investors in Cyprus and Greece: Vulture Funds, Financialization, and Systemic Risk

Vulture Funds6 (VFs) or Private Debt Investors—defined as hedge funds or private equity funds that specialize in distressed debt investing or the acquisition of forced-sale assets (Wozny, 2017, p. 702)—are particularly notorious in developing economies for their profit-driven and frequently deleterious interventions (Gianviti et al., 2010).7 These funds typically pursue investments with exceptionally high potential returns, commensurate with the elevated risk of default inherent in distressed assets.8 VFs are active participants in the secondary debt market, which may be conceptualized as a marketplace for second-hand financial instruments.9 In this context, VFs acquire government bonds or corporate debt from distressed countries, seeking enhanced returns as compensation for the higher risk they assume. The valuation of these securities is determined by insolvency levels, as assessed by international credit rating agencies. As Toussaint and Millet (2010) explain, private credit institutions acquire such bonds at significantly discounted prices when original creditors seek to divest, aiming to recover at least a portion of their invested capital. Notably, countries such as Peru, Zambia, the Democratic Republic of Congo, Congo-Brazzaville, Argentina, and Nicaragua have been compelled to repay VFs at rates exceeding the original terms, underscoring the predatory nature of these transactions.

To contextualize this phenomenon, it is essential to clarify that financial assets refer to claims arising from contractual agreements on future cash flows or from ownership of equity instruments in another entity. In contrast, financial instruments are contracts that generate a financial asset for one party and a corresponding financial liability or equity instrument for the other. Contemporary financial markets are characterized by a dual structure: bank-based finance and capital markets-based finance (Bavoso, 2019). The development of both channels theoretically provides a model in which large borrowers may choose between bank-intermediated products and disintermediated market-based products (Bavoso, 2019, p. 4).

Sassen (2017; 2018) highlights a critical distinction between traditional banking and modern finance: while traditional banks lend out existing capital, contemporary finance often trades in notional assets, thereby increasing systemic complexity. She argues that this complexity enables finance, in its most innovative forms, to function as an extractive sector—extracting prospective value and subsequently departing, often leaving significant economic disruption in its wake (Sassen, 2017, p. 9). Regardless of the modesty of the underlying assets, the aggressive pursuit of profit by modern financial actors explains the extractive evolution of finance and the devastation it frequently leaves behind. Globally, an estimated two billion “small” borrowers unable to repay their debts represent a vast opportunity for high-finance actors, who commodify these obligations into highly liquid financial packages, frequently secured by minimal material assets such as fractional home ownership, “a little piece of the little house” (Sassen, 2017, p. 17).

Scholars of accumulation theory contend that the volatility of asset prices and the proliferation of debt have heightened systemic risk within financialized capitalism, rendering it increasingly susceptible to recurrent crises (Stockhammer, 2013). Financialization is thus understood as a profound transformation of the capitalist accumulation regime (Stockhammer, 2013). The concomitant rise in financial fragility, coupled with stagnating wages, has produced a growth model reliant on debt-driven consumption and housing bubbles—an “enormous superstructure of debt, critically undermining its own liquidity and solvency” (Lapavitsas, 2009, p. 138). Accordingly, the subprime mortgage crisis of 2008 is widely regarded by accumulation theorists as the culmination of the financialization process, rather than a mere regulatory failure or the result of investor irrationality (Lapavitsas, 2009; Deutschmann, 2011). The liberalization of capital flows has exacerbated imbalances between surplus and deficit states, particularly in developing economies, resulting in boom-bust cycles and exchange rate volatility (see Epstein, 2005b; Becker et al., 2010; Kaltenbrunner, 2010). Consequently, financialization has amplified the vulnerability of economies worldwide.

In the post-crisis context, VFs have consolidated their financial power by capitalizing on assets that have migrated outside the traditional banking sector over the past decade.10 A significant repercussion of the systemic crisis was the proliferation of non-performing loans (NPLs)11, a consequence of prior indiscriminate lending practices and the subsequent recession induced by austerity and socioeconomic distress (Lapavitsas et al., 2010). As Lapavitsas et al. (2010) demonstrate, finance not only precipitated the crisis but also exploited its aftermath. The acute need for liquidity within the banking sector, coupled with the excesses of the preceding speculative bubble, created rewarding opportunities for private debt markets and their investors. Banks, under pressure to comply with new EU regulatory frameworks, have increasingly sold NPLs to private investors, thereby facilitating the cleaning of their balance sheets and further entrenching the influence of VFs.

3.1. Non-Banking Financing and Non-Performing Loans in the Capital Markets Union

The European Commission’s ‘Action Plan to Tackle Non-Performing Loans in Europe (Council of the EU, 2017) has exerted significant pressure on both banks and regulatory authorities to address existing stocks of NPLs and to implement measures designed to prevent future accumulations. Of particular importance is the post-crisis establishment of the CMU, which was conceived as a comprehensive initiative to address financial shortfalls by promoting alternatives to traditional banking channels and institutions.

The CMU pursues three principal objectives:

a. To diversify sources of financing within Europe by strengthening the role of capital markets, thereby providing borrowers and investors with a broader array of financial instruments tailored to their respective needs.12

b. To deepen the single market for financial services, enabling capital markets to benefit from the scale of the single market and thereby become deeper, more liquid, and more competitive, ultimately serving the interests of both borrowers and investors.

c. To foster economic growth and financial stability by facilitating corporate access to finance and promoting diversified funding channels. This approach aims to mitigate risks associated with excessive reliance on bank lending and intermediation, thereby enhancing the stability of the financial system as a whole and enabling financial intermediaries to provide increased funding to the real economy.

However, it would be reductive to interpret this trajectory solely as a mechanism for NPL reduction. Rather, it aligns with an increasing conflation of economic growth with financialisation, as well as the expanding influence of private debt, particularly through the activities of VF investors. In this context, surplus and surplus transfer have been identified as primary mechanisms of exploitation (Gouliamos, 2014; Harvey, 2011). When profits stagnate or are projected to decline—as was the case during the recent crisis—the capitalist class seeks expansion into new geographies (Amin, 2019), often by adapting tools previously employed in less developed economies. Amin (2019) further observes that an increasing proportion of surplus can only be invested in finance to sustain accumulation under monopoly capitalism. The transition from industrial to financial capitalism (Bavoso, 2018), or more precisely, the intensification of financialisation and the growing prominence of financial markets, institutions, and motives in the global economy (Epstein, 2005), has resulted in explosive growth in GDP and financial wealth. Yet, this has not translated into commensurate benefits for the real economy, with lower- and middle-income earners experiencing minimal gains (Loorbach et al., 2020) and both corporations and households becoming increasingly dependent on capital market products rather than traditional banking instruments (Bavoso, 2018). This process contributed to a substantial increase in the revenues of financial institutions during the 1980s and 1990s (Epstein & Jayadev, 2005). As van der Zwan succinctly notes, “the victory of the rentiers has come at the expense of wage-earners and households, who have faced stagnating real wages and increased indebtedness, respectively” (2014: 105).

The intrinsic relationship between growth and financialisation is explicitly acknowledged in the European Council’s Action Plan for tackling NPLs (Council of the EU, 2017), which emphasizes the need for banks to restructure their business models to address NPLs, contributing to enhanced growth and reducing financial fragmentation. In this context, facilitating the entry of VFs into the EU’s crisis-affected secondary markets is positioned as a core element of the growth strategy: the CMU thus serves as a bridge to capital markets. Notably, EU policy documents do not address the potential for increased disparities and uneven development among member states resulting from this approach. Instead, EU institutions have advanced normative and ideological justifications, asserting that “as economies develop, the marginal gain in economic activity associated with an increase in bank intermediation becomes smaller, while the marginal impact associated with a further development of capital markets increases” (Commission Staff Working Document, 2015: 18). Furthermore, they conclude that “when recessions coincide with financial crises, bank-oriented economies tend to suffer more than market-oriented ones,” thus making diversification through capital markets more desirable (ibid: 18). This policy orientation can be interpreted as an open invitation to private debt investors, despite the risk of exacerbating social problems.

The implementation of the CMU and the Action Plan has contributed to a marked reduction in the aggregate volume of NPLs held by Europe’s significant credit institutions, from €1 trillion (an 8% NPL ratio) at the inception of the European Central Bank’s Single Supervisory Mechanism (SSM) in 2014, to €587 billion (a 3.7% NPL ratio) by March 2019. Prominent institutions such as Cerberus Capital Management, Blackstone, Lone Star Funds, Goldman Sachs, Deutsche Bank, Intrum, CarVal Investors, Fortress, Oaktree Capital Management, and Apollo Global Management exemplify the PDIs that have responded to this invitation, focusing particularly on distressed euro area countries in the periphery. Between 2014 and 2019, PDIs—predominantly US-based and consistently ranked among the world’s largest—capitalized on the opportunities presented by the EU crisis and the increasingly business-friendly environment in the euro area, facilitated by the CMU and the EAPs implemented in peripheral states. These entities have emerged as the principal acquirers in a “deleveraging Europe” (Deloitte, 2019). The top 50 PDIs (34 of which are US-based) collectively hold nearly €1 trillion in loans and properties across the EU, and in Cyprus, Greece, Ireland, and Portugal alone, they completed transactions valued at €144 billion by 2019 (Deloitte, 2019).13

Apollo Global Management (AGM) provides a paradigmatic example of the nature, operations, and impact of VFs. AGM’s self-description—reflective of the broader PDI sector—emphasizes opportunistic investment strategies that leverage crises.14 Its approach is structured around four key benchmarks: capital structure arbitrage, defensive credits, stressed credit and distressed credit-linked equities, and short exposure via alpha-centric shorts.15 Portfolio rebalancing is opportunistically driven, with asset allocation determined by the perceived “best risk/return with consideration to liquidity asset coverage, time to the event and internal rate of return expectations.”

The following subsection will present evidence on how the CMU and EAPs have affected Cyprus and Greece, with particular emphasis on the growing influence of PDIs and their interactions with credit institutions.

3.1.1. The Interplay between Private Debt Investors and Credit Institutions in Cyprus and Greece within the Capital Markets Union Framework

The Case of Cyprus

In August 2018, the Bank of Cyprus announced an agreement to sell over 14,000 loans, with a total value of €2.8 billion—of which €2.7 billion were classified as NPLs and secured by real estate collateral—to AGM for a gross cash consideration of approximately €1.4 billion. This transaction, in effect, enabled AGM to acquire the loans at a significant discount, thereby initiating a process of loan restructuring, debt-for-asset swaps, and foreclosures aimed at recovering the contractual loan balance of €5.7 billion.16 Notably, the acquisition represented nearly one-sixth of Cyprus’s 2017 GDP and followed the enactment of new legislation that introduced enhanced foreclosure provisions and facilitated securitizations. These legislative reforms, designed and enforced by the Troika-led EAP, sought to assist Cypriot banks in reducing their substantial NPL portfolios.17

As a result, AGM secured a pioneering position in the Cypriot NPL market, accounting for an estimated 14% of the country’s total NPLs. Prior to this, APS, a Luxembourg-based Czech distressed debt investment firm with expertise in debt recovery, acquired a €2.5 billion portfolio of NPLs from Hellenic Bank.18 Furthermore, AGM was a significant shareholder in Altamira Asset Management, which acquired nearly €7 billion in NPLs from the Cyprus Cooperative Bank prior to its dissolution and subsequent merger with Hellenic Bank.19 Altamira (Real Estate Cyprus) has since emerged as the most active platform for the sale of distressed assets. Another notable NPL manager, Pepper European Servicing, was selected by the Bank of Cyprus to manage an additional €850 million in defaulted collateral, subsequently expanding its operations to manage NPL portfolios across Southern Europe, including Greece and Spain.20 A more recent transaction of significance involved the Bank of Cyprus’s sale of a toxic debt portfolio with a gross book value of €916 million to PIMCO21, a subsidiary of Allianz SE, a leading global financial services provider with assets totaling €1.686 trillion.22 The “Helix 2” project, with a contractual balance of €1.46 billion, comprised 22,224 loans—primarily to retail and SME clients—secured by 5,616 real estate assets. The net book value of the assets sold amounted to €440 million. Notably, PIMCO had previously been commissioned by the Central Bank of Cyprus in September 2012, prior to the 2013 EAP, to conduct an independent due diligence exercise in the context of Troika negotiations, providing independent estimates of the capital needs of the banking sector (Hardouvelis and Gkionis, 2016; Orphanides, 2014). However, subsequent investigations revealed significant discrepancies in these estimates. As noted by Orphanides (2014), a confidential report concluded that the capital needs of the banking system ranged between €0.7 and €2.4 billion, substantially lower than PIMCO’s estimate of €5.7 billion (Zenios, 2013). The International Monetary Fund (2013) also acknowledged that PIMCO employed a more conservative methodology than in comparable exercises in peer countries.

This sequence of events raises questions regarding the dual role of firms such as PIMCO, which initially provided independent due diligence for the banking sector and subsequently acquired NPL portfolios from the very institutions they assessed. By March 2021, Cypriot banks had reduced their NPLs ratio to 17.7% of total loans, down from 27.6% a year earlier; nevertheless, Cyprus continued to exhibit the second-highest NPL ratio in the EU, surpassed only by Greece.

The concentration of NPLs among a limited number of large conglomerates underscores the strategic significance of Cyprus’s economy and the prospective profitability for PDIs and servicers. This trend indicates a high degree of property and debt consolidation in the hands of VFs, reflecting the growing influence of alternative capital market actors who capitalize on EU-driven bank restructuring policies and enabling local legislation. Such developments risk exacerbating socioeconomic inequalities, and contributing to adverse social outcomes, including rising levels of homelessness.

Table 1.

Non-Performing Bank Loans Acquired by PDIs in Cyprus, 2017–2022.

| Cyprus | PDI | Credit Institution | Assets |

|---|---|---|---|

| Apollo Global Management (AGM) | Bank of Cyprus (2018) | 14,000 loans of €2.8 billion (of which €2.7 billion relate to NPLs) and secured by real estate collateral, to AGM for a gross cash consideration of some €1.4 billion. | |

| Altamira Asset Management (AGM was shareholder) | Cyprus Cooperative Bank prior to the latter’s dissolution and merger to the Hellenic Bank | €7 billion worth NPLs | |

| APS | Hellenic Bank | €2.5 billion share in NPLs | |

| Pepper European Servicing | Bank of Cyprus | €850 million of default collaterals | |

| PIMCO (owned by Allianz SE | Bank of Cyprus | Portfolio of NPLs with a gross book value of €916 mn |

The Case of Greece

The entry of VFs into Greece’s NPL market was a gradual process, ultimately culminating in the acquisition of significant portfolios of distressed assets previously held by Greek banks. Once market conditions matured, a cohort of international VFs secured ownership of major projects involving Greek properties formerly under the purview of the domestic banking sector. Fortress Investment Group, ranked among the top 50 PDIs, acquired a portfolio of small and medium-sized enterprises (SMEs) NPLs valued at approximately €1.8 billion, sold by a consortium comprising Piraeus Bank, National Bank of Greece, Eurobank, and Alpha Bank. Additionally, Fortress purchased from Alpha Bank a pool of SME NPLs with a gross book value of €1.1 billion.23

Several VFs engaged third-party servicers to manage these portfolios, often employing more aggressive recovery strategies.24 AGM acquired from Alpha Bank the “Jupiter” package for €337 million, consisting of non-performing corporate loans secured by real estate collateral25 with claims of €1 billion, as well as 1,756 mortgages with an estimated value of €543 million.26 Bain Capital, ranked 22nd among the top 50 PDIs, acquired the “Amoeba” NPL portfolio from Piraeus Bank for €430 million, which included over 2,000 properties as collateral. Furthermore, Centerbridge Partners (ranked 43rd) and Elliott Advisors (UK) Limited jointly acquired a €250 million portfolio comprising 12,800 NPLs, secured by 8,300 real estate assets.27

This wave of transactions illustrates a pronounced redistribution of property in Greece, reflecting a competitive dynamic among global financial conglomerates to capitalize on what is, in effect, a socially adverse opportunity to advance their strategic objectives. The entry and expansion of PDIs in the Greek market appears to be an outcome of the establishment of the CMU (and the BU and the EAP, as it is demonstrated in the next sections), intensifying the concentration of distressed assets in the hands of a few powerful actors, raising concerns about the broader socioeconomic implications.

Table 2.

Non-Performing Bank Loans Acquired by PDIs in Greece, 2017–2022.

| Greece | PDI | Credit Institution | Assets |

|---|---|---|---|

| Apollo Global Management (AGM) | Alpha Bank | non-performing corporate loans with real estate collateral claiming €1 bn and 1,756 mortgages with an estimated value of €543 m | |

| Fortress Investment Group LLC | Consortium of Banks Piraeus, National, Eurobank and Alpha | non-performing loans of a value around €1,8 billion | |

| Fortress Investment Group LLC | Alpha Bank | a pool of Non-Performing Loans to Greek SMEs mainly secured by real estate assets (the “Neptune Portfolio”), of a total on-balance sheet gross book value of Euro 1.1 billion | |

| Bain Capital | Piraeus Bank | € 430 million Amoeba non-performing loan portfolio, with more than 2,000 properties at collateral and face value of €1.95bn. | |

| Centerbridge Partners& Elliott Advisors (UK) Limited | National Bank of Greece | €0.9 billion portfolio of 12,800 NPLs, with 8,300 real estate collateral | |

| PIMCO (owned by Allianz SE | Bank of Cyprus | portfolio of NPLs with a gross book value of €916 mn |

3.2. The Banking Union, Structural Changes in Cyprus and Greece, and the Increasing Concentration of Credit Institution Assets

In September 2012, the European Commission published a roadmap for the institutionalization of the European Union Banking Union (BU)28, which has been described by some scholars as the most significant advancement in European economic integration since the inception of the euro area (Howarth & Schild, 2018). By 2016, the Single Supervisory Mechanism (SSM) and the Single Resolution Mechanism (SRM) had been established, and the corresponding regulatory framework was transposed into the legal systems of EU member states.29 This development resulted in enhanced oversight of banking regulations under the Capital Requirements Directive and Regulation (CRDIV/CRR), and introduced a new recovery and resolution framework for banks, as enshrined in the Bank Recovery and Resolution Directive (BRRD).30 Additionally, the Deposit Guarantee Schemes (DGSs) were formalized through the relevant Directive (DGSD). From its inception, the BU was conceived as an integral component of the broader project to deepen the EMU31, and is inextricably linked to the CMU.32

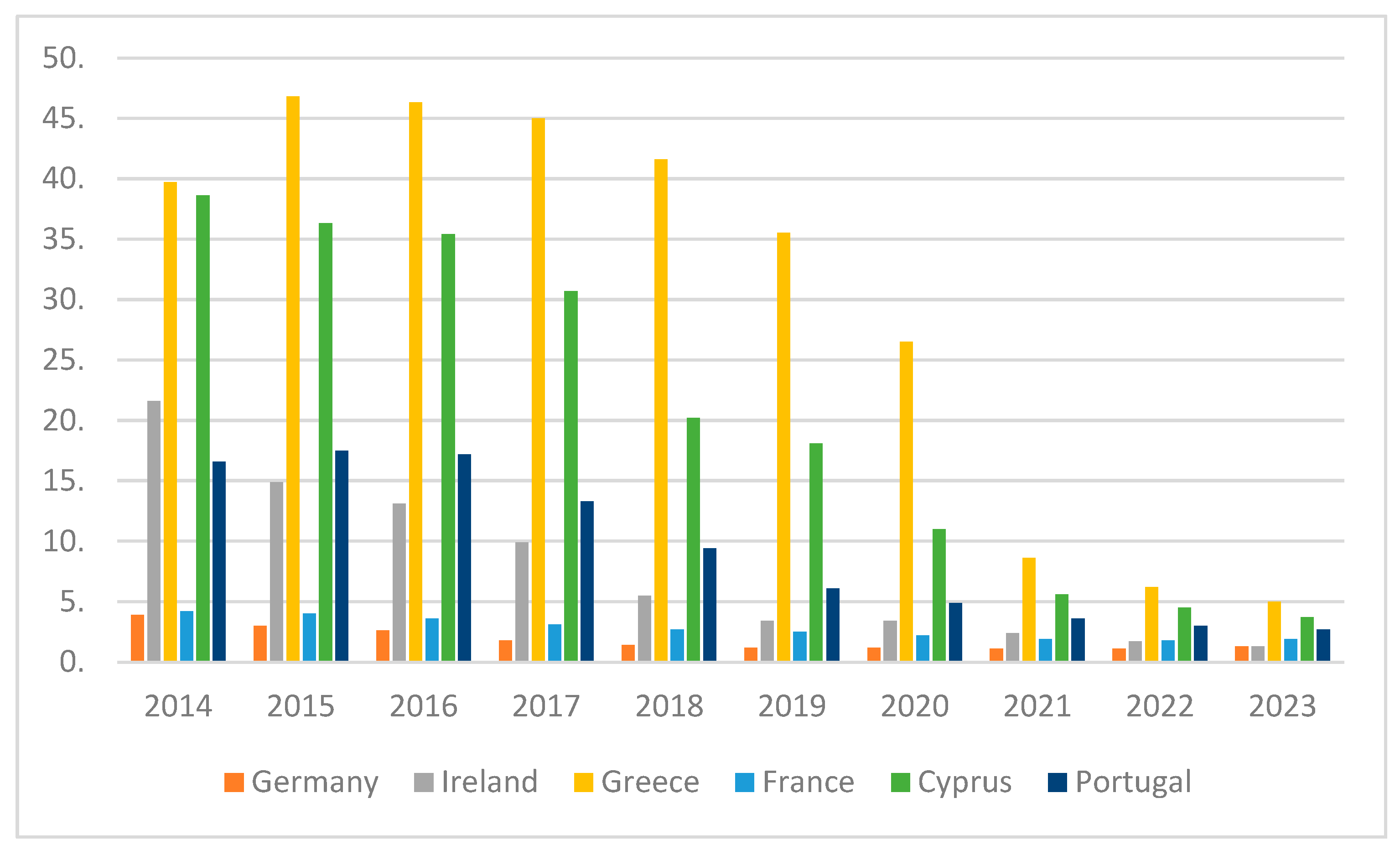

The establishment of the Banking Union (BU) took place against a backdrop of more than €5,118 billion in taxpayer-funded recapitalization and liquidity measures aimed at stabilizing EU banks (European Court of Auditors, 2019, p.4). At that time, the average non-performing loan (NPL) ratio across the EU was 3.2%. Core economies such as Germany and France exhibited relatively low NPL ratios, at 3.9% and 4.2% respectively in 2014, while peripheral economies faced much higher levels of financial distress, with NPL ratios reaching 39.7% in Greece, 38.6% in Cyprus, 21.6% in Ireland, and 16.6% in Portugal. As shown in Figure 1, this pronounced divergence between core and periphery in the pre-BU, CMU, EAP period gradually diminished following the implementation of the BU. By 2023, NPL ratios had converged to historically low levels across all countries, with Germany at 1.3%, France at 1.9%, Greece at 5.0%, Cyprus at 3.7%, Ireland at 1.3%, and Portugal at 2.7%, reflecting a significant reduction in financial sector risk and increased stability throughout the euro area.

The agreed approach within the EMU facilitated “special surveillance and supervision of cross-border banking cooperation and the termination of the toxic link between sovereign debt and the banking sector,” thereby accelerating the formulation of the BU (Momirović et al., 2017: 194). This process coincided with a trend toward increasing concentration in the banking sectors of distressed countries, including Greece, Ireland, Portugal, Spain, Italy, and Cyprus (Schoenmaker & Peek, 2014: 2). The exposure of banking sectors in peripheral countries was substantial, while stakeholders from core economies, most notably Germany, held significant interests, particularly in Greece. The stated aim of the Banking Union was to break the connection between government and bank debt, obligate banks to resolve and write off non-performing loans, and ensure they raised sufficient capital to cover potential losses (Donnelly, 2018). By creating resolution mechanisms, the intention was to reassure markets that troubled banks would be restructured, sold, or closed down instead of relying on government bailouts, thus strengthening market discipline and promoting financial stability (European Commission, 2012, p. 3; Donnelly, 2018).

3.2.1. Findings of Increasing Concentration in the Periphery

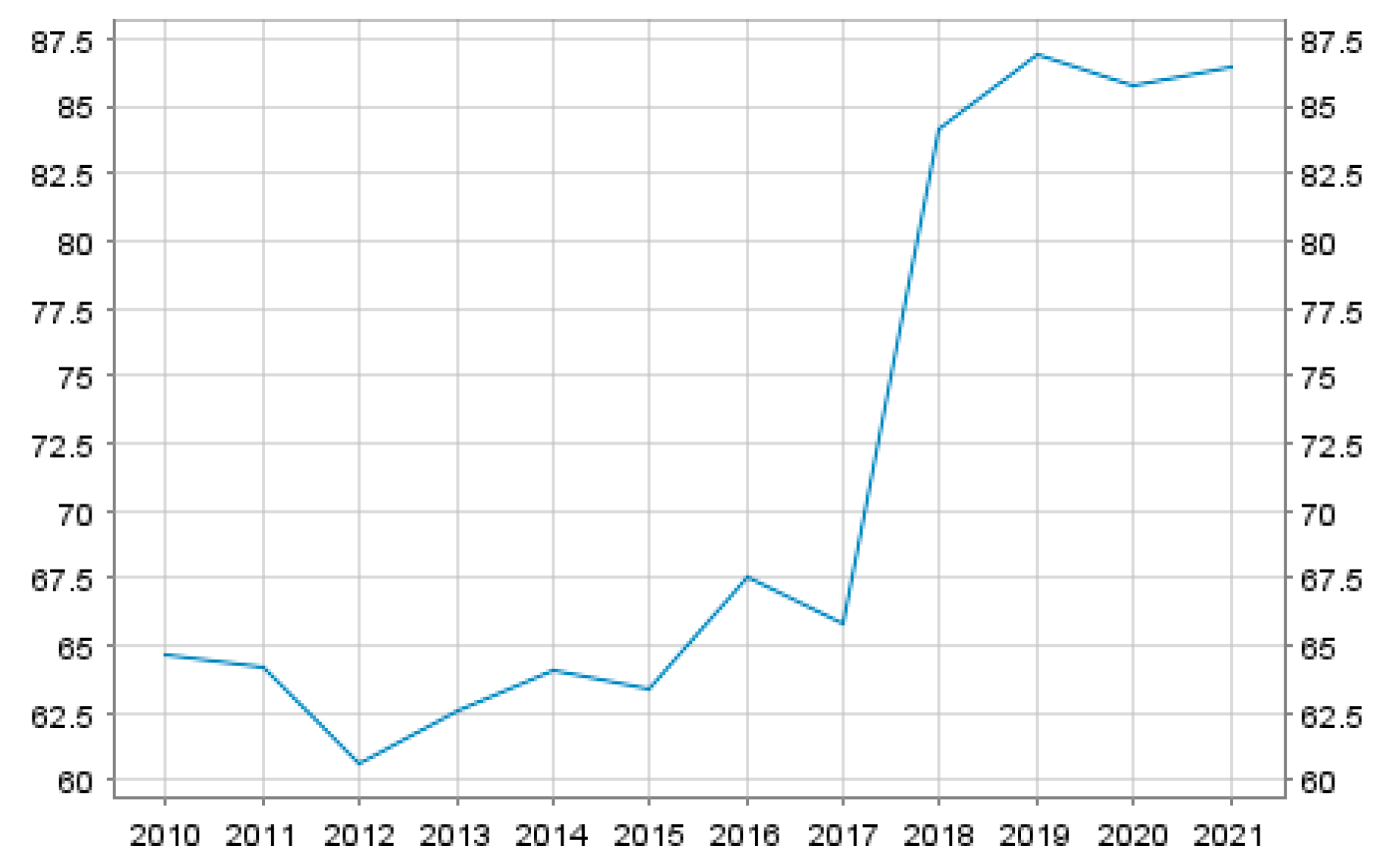

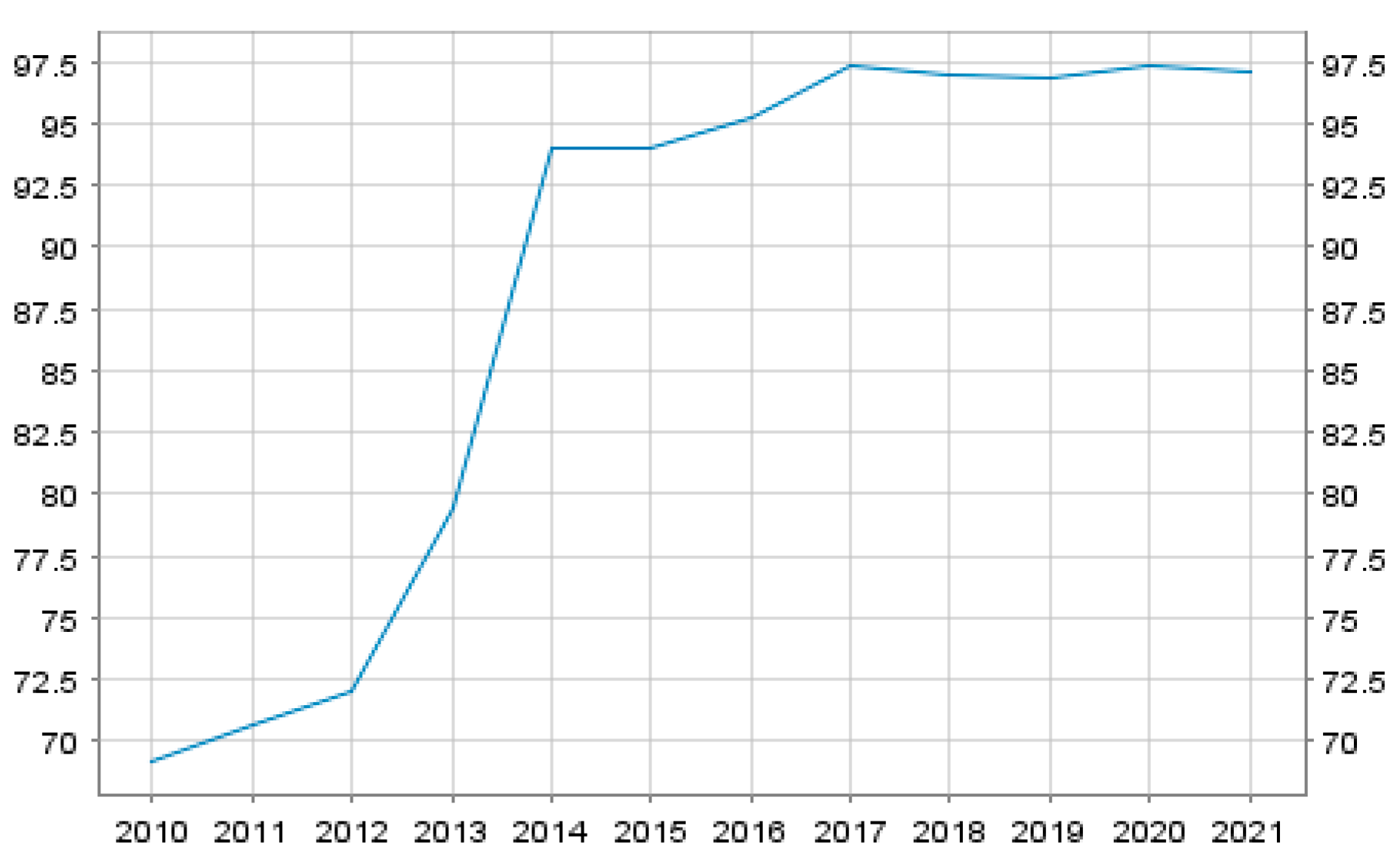

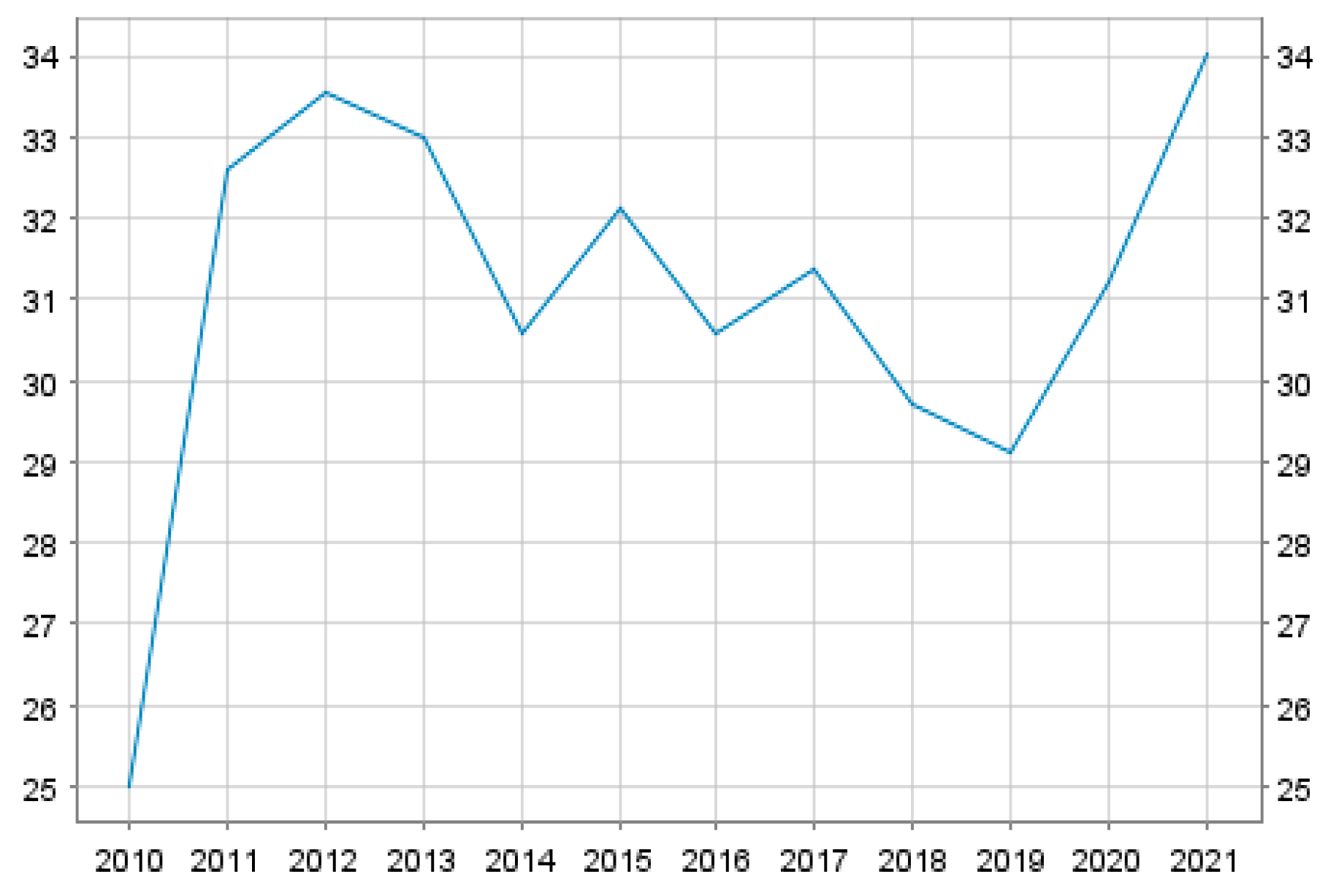

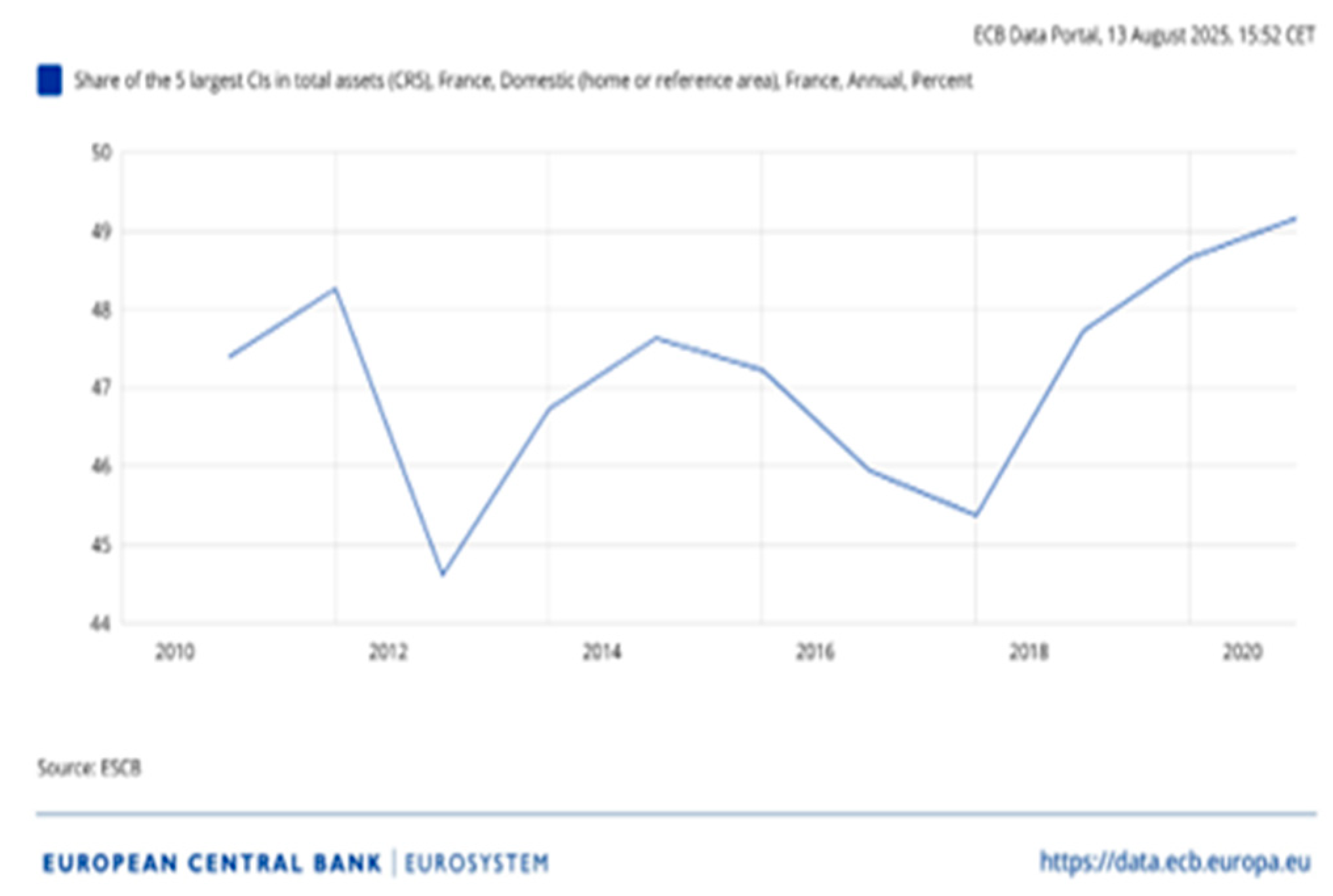

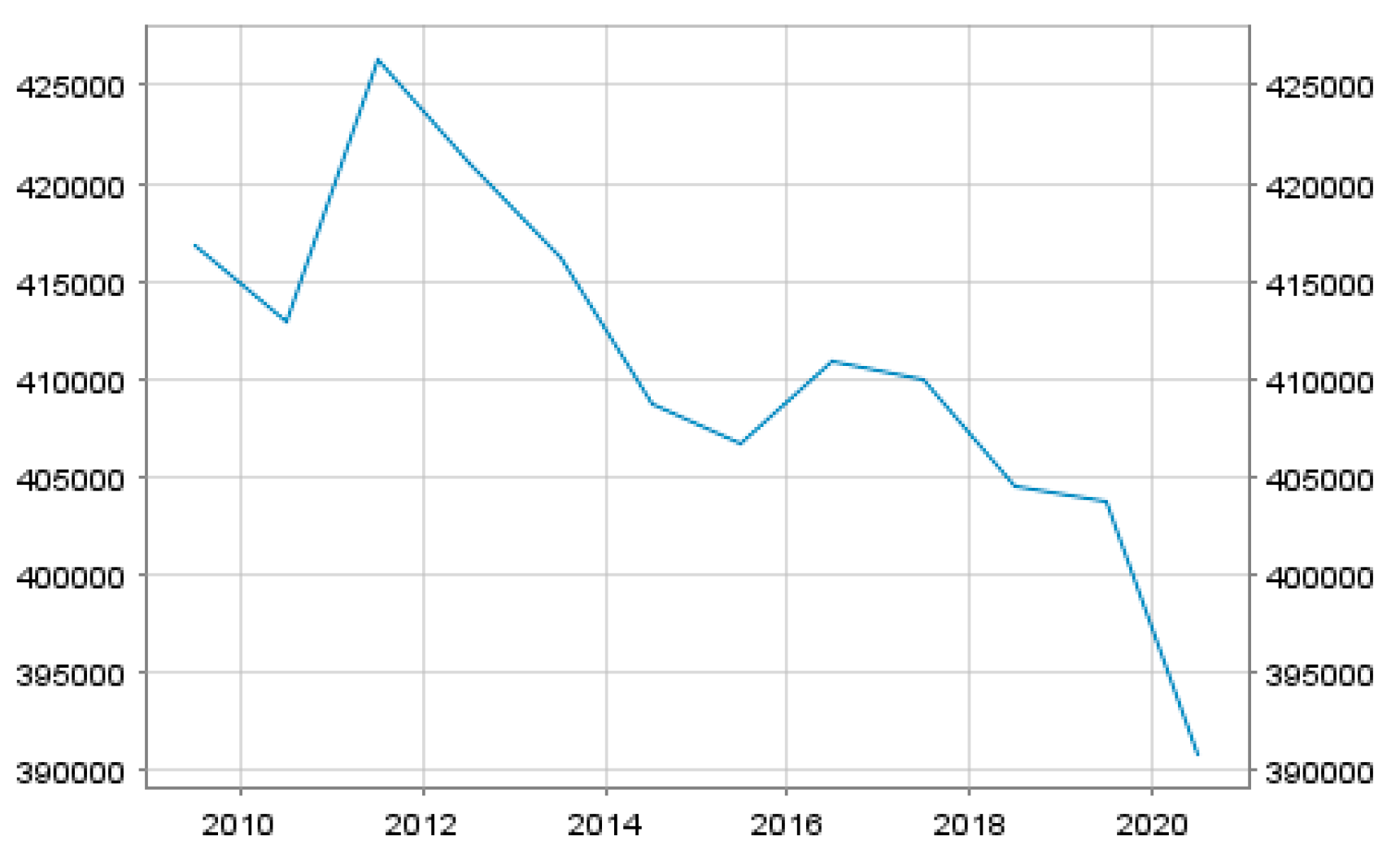

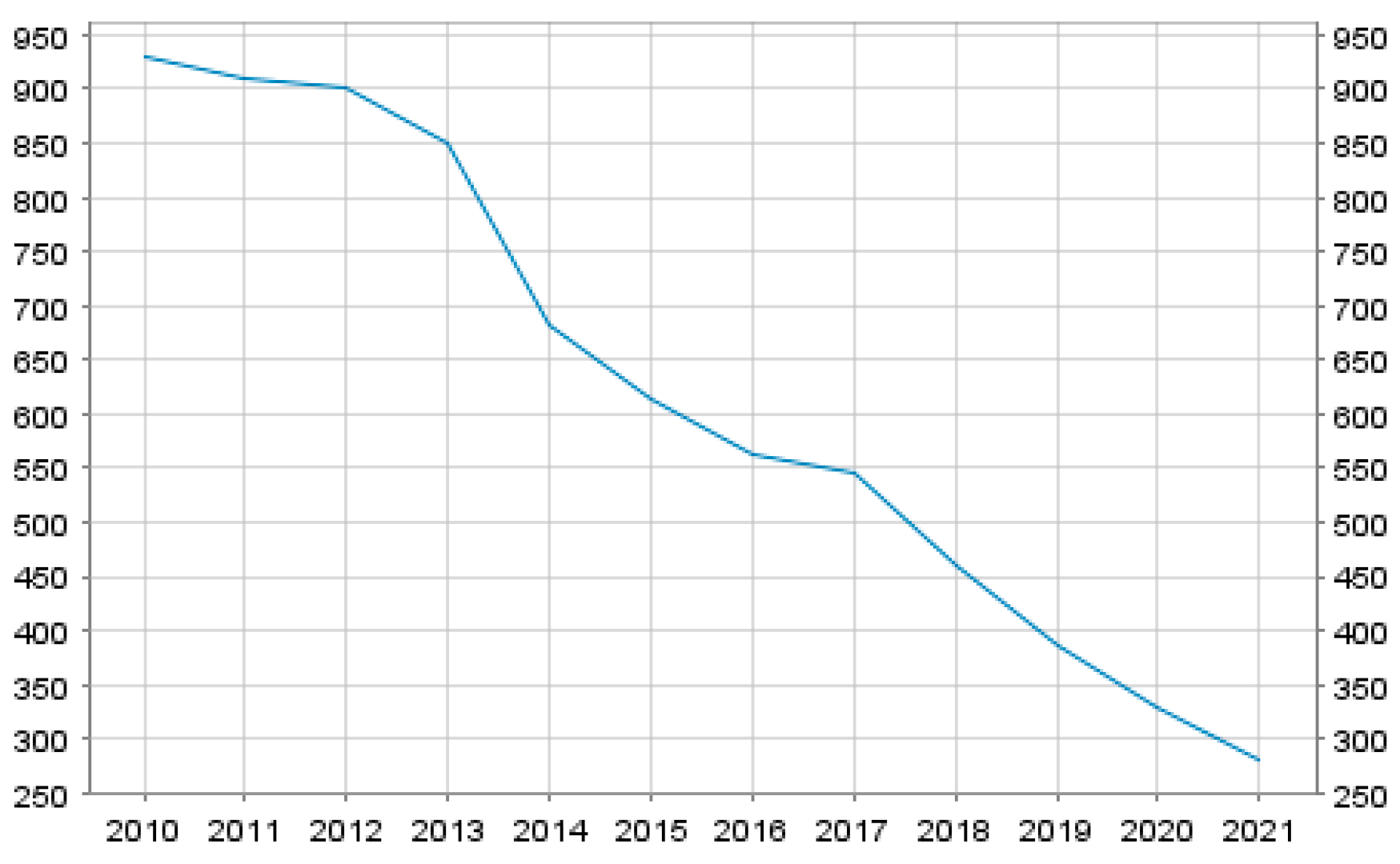

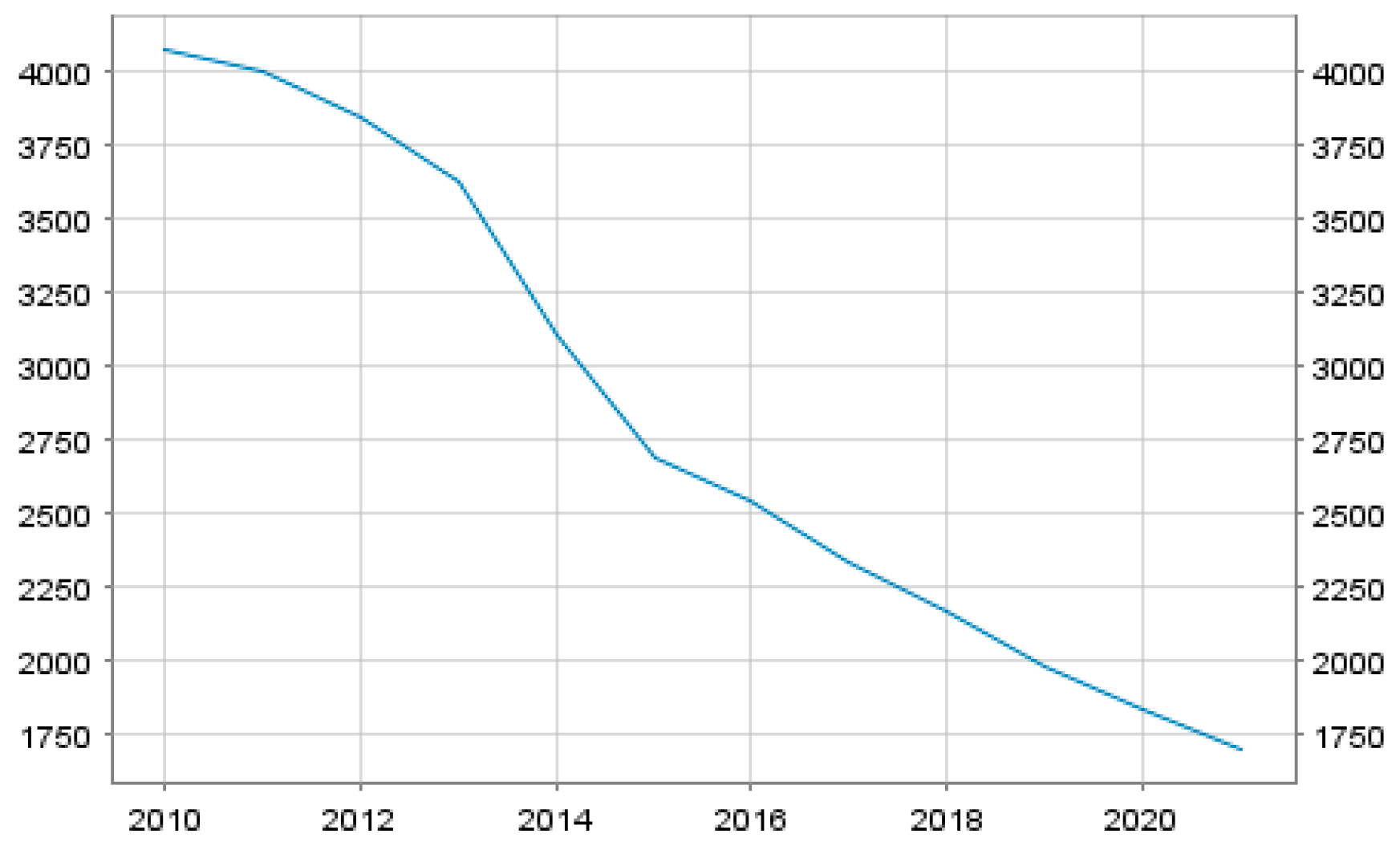

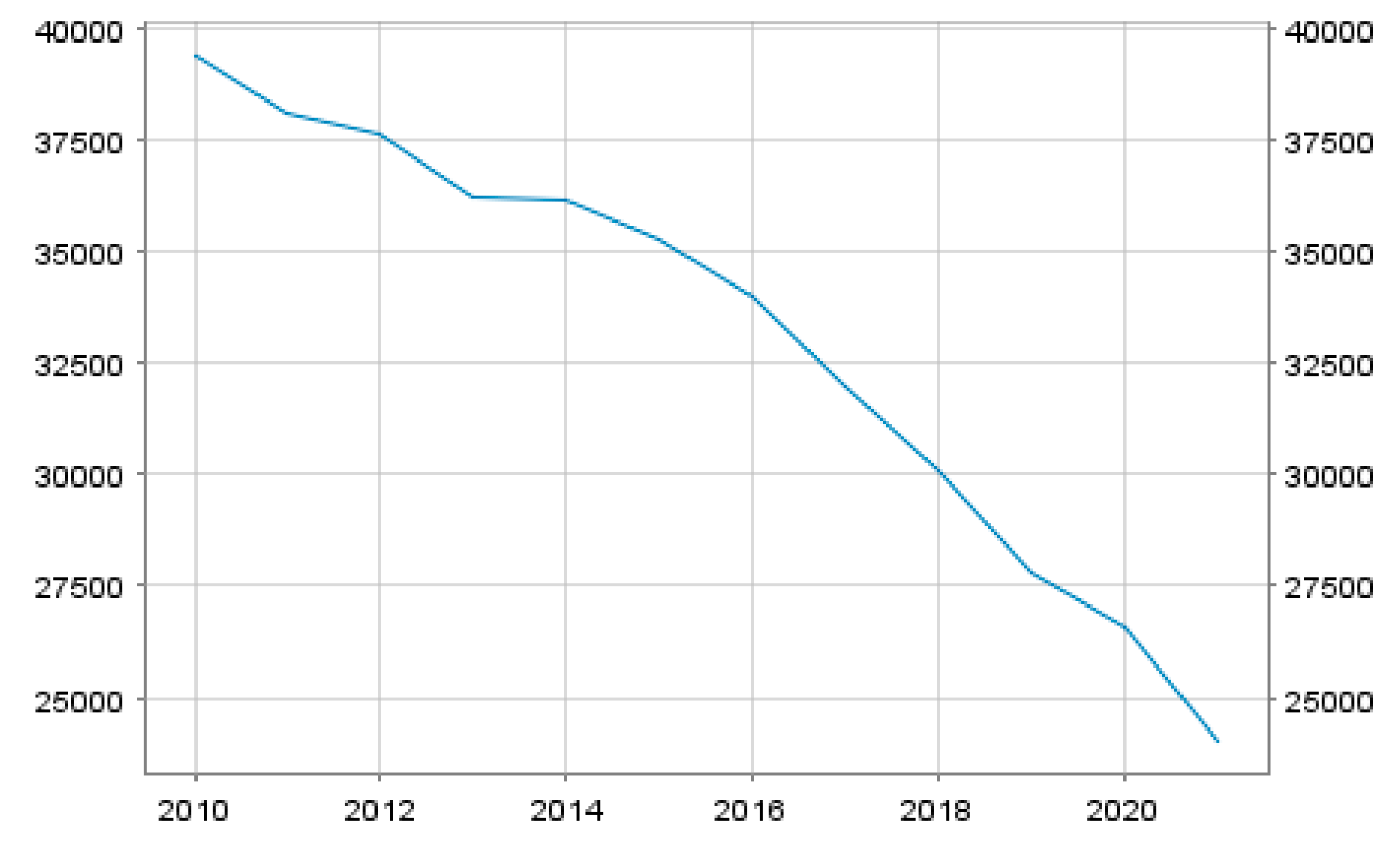

The evolution of the euro area crisis and the subsequent policy response, notably the establishment of the BU, have coincided with a marked concentration of assets among the largest banking-credit institutions (CIs) within the EMU. This phenomenon is especially pronounced in peripheral economies such as Greece and Cyprus, compared to core economies like Germany and France, as evidenced in Figure 2, Figure 3, Figure 4 and Figure 5.33

The increasing concentration in the periphery can be partially attributed to the implementation of EAPs, which prioritized the restructuring of national financial sectors through banking resolutions, recapitalization, mergers, and acquisitions. These interventions have led to a significant consolidation of banking assets. In contrast, the concentration of assets among the top five CIs in Germany and France remained at the period under study, comparatively moderate. For instance, while the asset share of the top five CIs in Germany has surpassed pre-crisis levels, it remains below 40%. Similarly, in France, the asset concentration is close to pre-crisis percentages. In the periphery, however, the asset share of the top five CIs has surged from about 70% in 2012 to close to 90% (in Cyprus) or more (Greece) in the restructured environment.

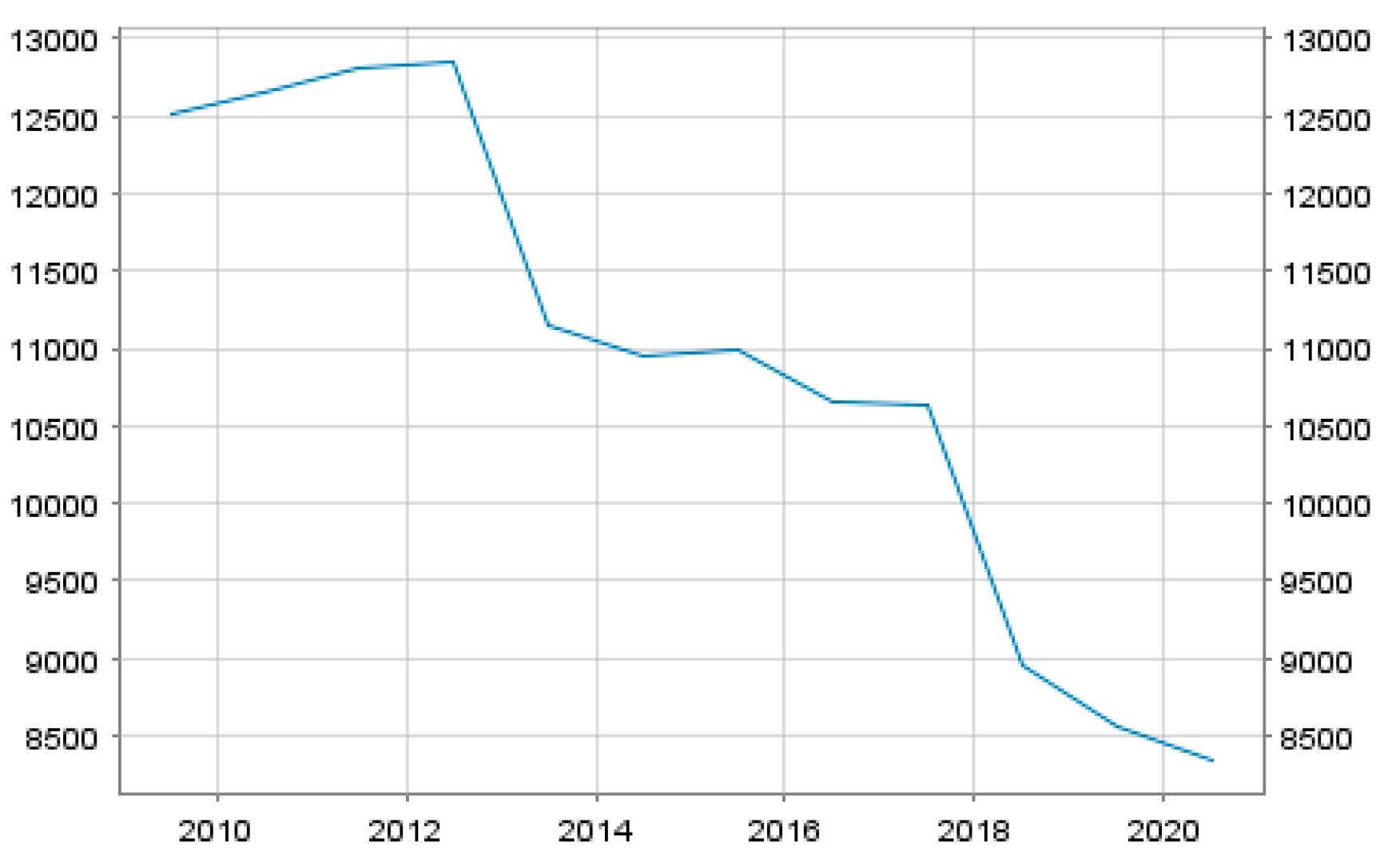

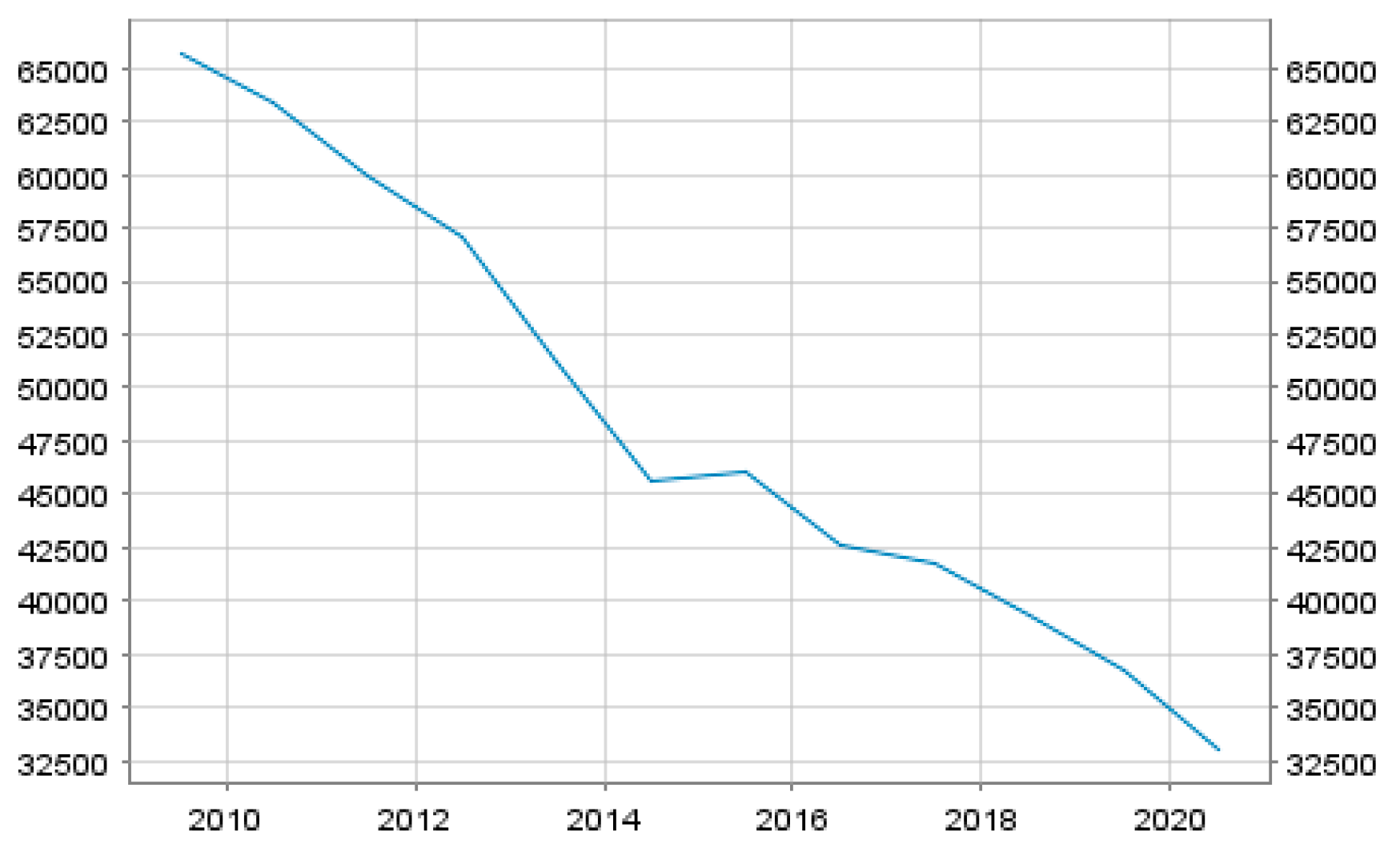

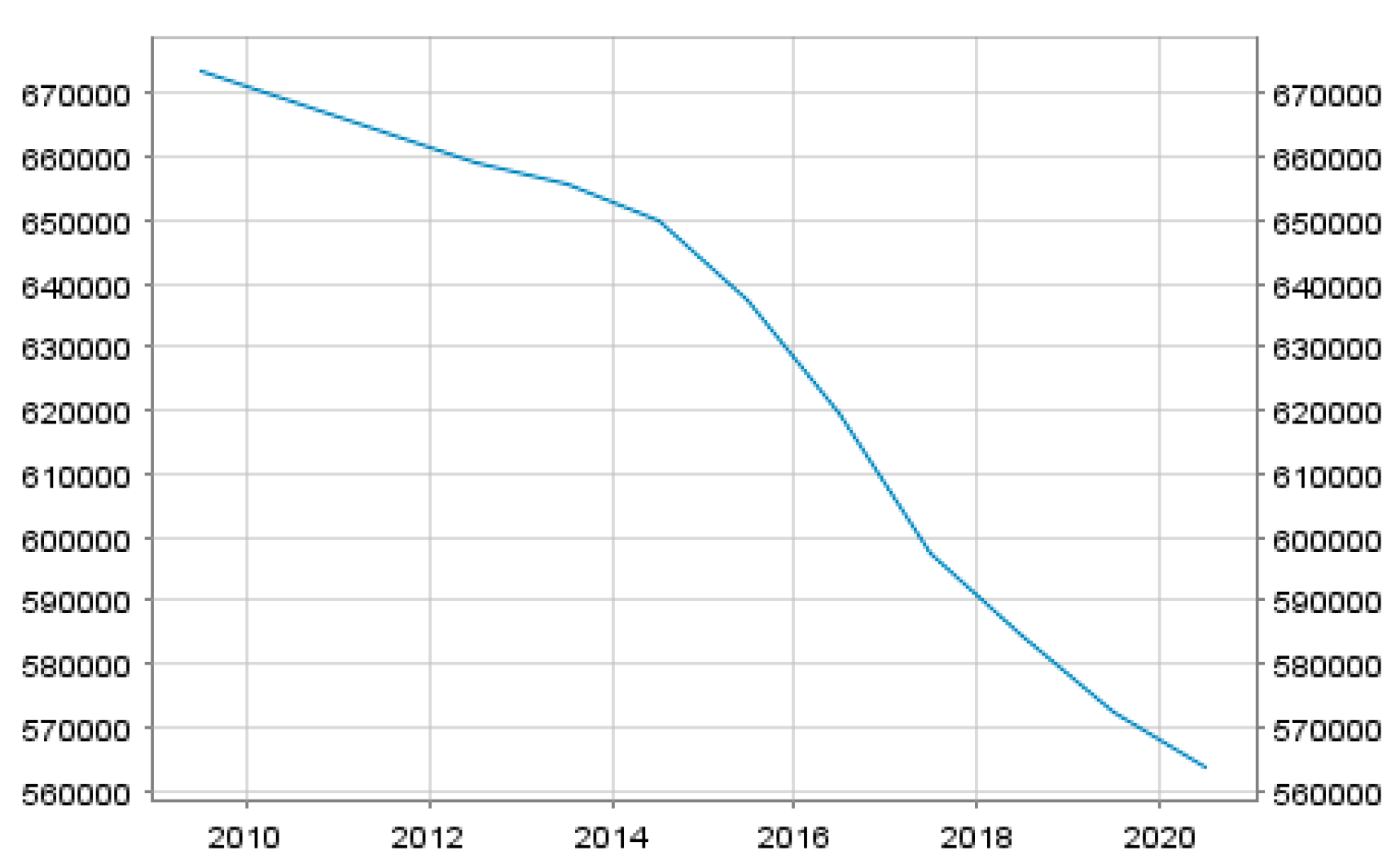

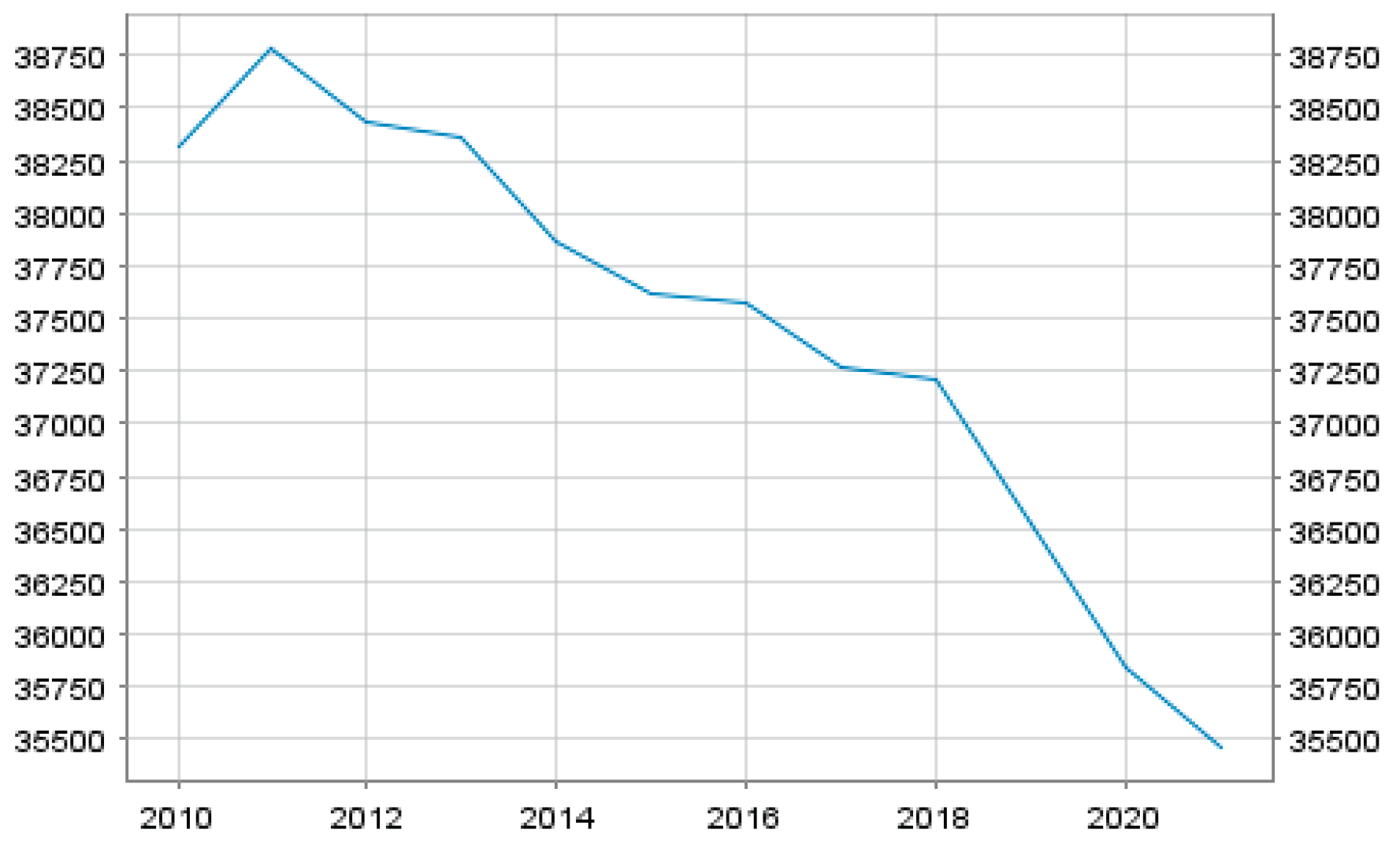

This trajectory towards increased market concentration has been accompanied by a sharp reduction in sectoral employment, a trend particularly acute in peripheral countries. The decline in the number of banking sector employees accelerated at the post-crisis inflection point, coinciding with the implementation of EAP reforms and the development of the BU. While digitalization has undoubtedly contributed to workforce reductions, empirical evidence suggests that, in the periphery, these changes were precipitated primarily by EAP-driven restructuring measures. Figure 6, Figure 7, Figure 8 and Figure 9 illustrate the decline in banking sector employment across Cyprus, Greece, Germany, and France, with the contraction being most severe in the former two.34

The identified reduction in employment appears related with a consistent decrease in the number of CI offices, as documented by European Central Bank (ECB) indicators. For example, the number of Figure 10, Figure 11, Figure 12, Figure 1335 show that CI offices in Germany peaked at 40,000 in the immediate aftermath of the crisis but fell to 24,000 by 2020. In France, the number of offices declined from 39,000 in 2008 to 32,000 in 2020. Cyprus experienced a threefold reduction in CI offices, from 900 to 280, while Greece saw the closure of nearly 3,000 offices, leaving only 1,700 in operation by 2020

These developments point to declining competition and increasing monopolistic tendencies in all four countries, corroborating findings from other studies that document a reduction in banking competition in the Eurozone periphery (Apergis et al., 2016). Notably, the decline in the number of CI offices is most pronounced in Greece and Cyprus. The increasing concentration of CI assets thus appears to be linked not only to the crisis and the BU, but also to structural reforms implemented under the EAPs in peripheral economies. This issue will be further explored in the subsequent subsection.

3.3. The EAP-Driven Reconfiguration of the Banking Sector in Cyprus

The principal objective of the EAP for Cyprus, as articulated in the Memorandum of Understanding (MoU), was the “thorough restructuring and downsizing” of credit institutions (MoU: 1). The targeted downsizing aimed to reduce the sector’s size from 550% to 275% of GDP.36 Central to this process was the unprecedented bail-in executed on 25 March 2013, which was enforced by the Eurogroup with the concurrence of the Cypriot government and parliament. This one-off “stability levy,” applicable to both resident and non-resident depositors—insured and uninsured—fundamentally restructured Cyprus’s socioeconomic fabric through a comprehensive overhaul of its financial system. This intervention is widely regarded as a foundational moment for the future Banking Union, serving as a “bone and arrow” for subsequent EU financial architecture.37

The restructuring and downsizing measures entailed the introduction of a new resolution legal framework and direct intervention in two of Cyprus’s leading commercial banks: Bank of Cyprus (BoC) and Laiki Popular Bank (LPB). LPB, unable to raise private capital despite state aid, was ultimately resolved, with its “good bank” assets absorbed by BoC (European Union, 2013: 16, 42). The Cooperative Central Bank (COOP), which held over one fifth of Cypriot deposits and 20% of market loans, was unique among CIs in having no exposure to Greek government bonds or bank loans. Under state and European Central Bank (ECB) governance, the COOP entered a joint venture with debt servicers to manage its non-performing loan (NPL) portfolio. As the island’s second-largest bank, the COOP was ultimately sold on 15 June 2018 to Hellenic Bank, with all assets except NPLs transferred (European Union, 2018: 48). The non-performing assets were moved to a newly established state-owned entity, KEDIPES.

At the height of the crisis, NPLs in Cyprus reached €15.2 billion, or 63% of gross loans in the first quarter of 2015 (European Union, 2015: 25). In this context, the only viable strategy for restoring financial stability and profitability was deleveraging through capital markets, with PDIs acquiring NPLs at significant discounts. This was facilitated by the introduction of a new legal framework for foreclosures (European Union, 2015: 26) and a comprehensive reform of corporate and personal insolvency laws (European Union, 2015: 3). Additionally, forced mergers were promoted to enhance institutional viability, albeit at the expense of competition. Together, these measures created a financial environment marked by significant consolidation and a pronounced shift toward banking sector monopolies.

Table 3.

Key Events and Relationships in the EAP-Driven Reconfiguration of the Cyprus Banking Sector.

Table 3.

Key Events and Relationships in the EAP-Driven Reconfiguration of the Cyprus Banking Sector.

| Date/Period | Event/Action | Key Institutions Involved | Relationship/Outcome |

|---|---|---|---|

| 2013 (March 25) | Bail-in and Stability Levy imposed | Eurogroup, Cypriot Government, Parliament, All Banks | First-ever bail-in on both resident and non-resident, insured and uninsured depositors; foundational for future EU Banking Union; comprehensive sector overhaul |

| 2013 | New resolution legal framework introduced | All Credit Institutions (CIs) | Provided legal basis for restructuring and downsizing of sector |

| 2013 | Direct intervention in major banks | Bank of Cyprus (BoC), Laiki Popular Bank (LPB) | LPB resolved; “good bank” assets absorbed by BoC; BoC becomes dominant player |

| 2013–2018 | COOP under state/ECB governance; NPL management JV | Cooperative Central Bank (COOP), ECB, Debt Servicers | COOP manages NPLs via joint venture; no Greek bond exposure |

| 2018 (June 15) | Sale of COOP to Hellenic Bank | COOP, Hellenic Bank, KEDIPES | COOP’s assets (except NPLs) transferred to Hellenic Bank; NPLs moved to state-owned KEDIPES |

| 2015 (Q1) | NPLs peak at €15.2bn (63% of gross loans) | All Banks, PDIs | Financial stability pursued through deleveraging; PDIs acquire NPLs at discounts |

| 2015 onwards | New legal framework for foreclosures and insolvency | All Credit Institutions, Legislators | Facilitates NPL resolution, supports sales to private investors |

| 2013–2018 | Forced mergers and consolidation | Major Banks, Regulatory Authorities | Mergers promoted to ensure viability; increased concentration and monopolistic tendencies |

3.3.1. The MoU-Driven Reconfiguration of the Banking Sector in Greece

The primary objective of the first EAP for Greece was to restore the country’s credibility with private investors by “securing fiscal sustainability, safeguarding the stability of the financial system, and boosting potential growth and competitiveness” (European Union, 2010: 11).38 In terms of financial sector policy, the Programme sought to re-establish confidence and viability in the banking sector, which had lost access to wholesale markets by the end of 2009 and subsequently faced significant deposit outflows, resulting in an increased reliance on ECB refinancing (European Union, 2010: 23). According to the European Union, the Greek banking sector was not the original source of financial instability; rather, it was adversely affected by an economic and confidence crisis that stemmed from the “2008–2009 global crisis which exposed Greece’s vulnerabilities” (European Union, 2010: 6).

In response to these challenges, the EAP for Greece initially encompassed a suite of measures, including liquidity support for banks, recapitalisation initiatives compliant with competition rules, the establishment of the Hellenic Financial Stability Fund (HFSF)39, and the requirement for a comprehensive restructuring plan for the banking sector. These objectives were ultimately achieved, albeit at considerable cost to the Greek populace and to other euro area countries such as Cyprus, despite the initial reluctance of EU authorities to consider debt restructuring, which was deemed unaffordable for the EMU.40

A significant policy decision by the ECB was to accept Greek government debt and other liabilities guaranteed by the Greek state as collateral “regardless of its rating,” a move that arguably reflected a bias in favor of core systemic banks (European Union, 2010: 35). During the initial phase of the EAP, as the crisis unfolded, developments in the Greek banking sector were relatively moderate compared to subsequent periods. Competition within the sector remained largely unregulated; for example, Piraeus Bank unilaterally acquired two state-owned institutions, ATE and TT Postbank, while another bank that failed the stress test was required to “implement interim restructuring measures under enhanced supervision by the Bank of Greece” (European Union, 2010: 92).41

Within this context, a strategic review was commissioned to assess options for all state-owned banks, including ATE, and to articulate a vision for future government involvement in the sector. Three international investment banks—HSBC, Deutsche Bank, and Lazard—were tasked with conducting this review and proposed a range of options, including “mergers, sales of individual or merged entities to private banks, full privatisation and liquidation” (European Union, 2010: 24).42 Furthermore, the employment status of bank staff was identified as a constraint on operational flexibility; consequently, new legislation was introduced to allow banks to negotiate employment conditions directly with their employees (European Union, 2010: 25). Ultimately, the Programme envisaged a complete withdrawal of government ownership from the banking sector.43

The comprehensive fiscal and structural adjustment reforms,44 coupled with the imposition of austerity measures45, precipitated a period of severe economic contraction and prolonged recession in Greece—conditions described as “deeper and longer” than initially projected by international lenders (European Union, 2011: 1). This environment of tightening liquidity and escalating non-performing loan (NPL) ratios placed considerable strain on the Greek banking system, as credit availability continued to contract (European Union, 2011: 76). Specifically, the sovereign debt restructuring, undertaken amidst a recessionary context, resulted in significant capital shortfalls across the entire Greek banking sector. This necessitated the development of a targeted recapitalisation strategy, wherein viable banks were to be recapitalised, while non-viable institutions faced dissolution—a process that constituted a forced restructuring of the sector (European Union, 2012: 3–4). For example, TT Bank was resolved, with its assets transferred to Postbank and Proton Bank.

The second EAP for Greece focused on achieving debt sustainability and restoring national competitiveness. To facilitate more effective implementation of fiscal consolidation, privatisation, and structural reforms, the permanent presence of the Troika Task Force was established in Greece.46 Notably, the Greek constitutional legal framework was amended to prioritise external debt servicing payments, thereby subordinating domestic social needs—including private and household debt servicing—to the overarching objective of stabilising the banking system. By 2011, NPLs had reached 15.5%, underscoring the magnitude of the crisis.

Within this context, a Private Sector Involvement (PSI) exchange offer was agreed, encompassing all private sector bondholders and entailing a nominal haircut of 53.5%.47 The PSI was designed to alleviate Greek sovereign debt by restructuring government and selected state-owned enterprise bonds. A portion of the funds released through the PSI haircut was allocated to the financing of the second adjustment programme, including the recapitalisation of Greek banks (Statement by the Eurogroup, 21 February 2012: 7). However, the PSI-II48 initiative also contributed to further bank insolvency issues, as it resulted in significant additional losses and capital needs for Greek banks. The net present value losses on government bonds were projected to exceed 70% of the sector’s portfolio, amounting to approximately €43 billion (European Union, 2012: 17–18).

The Second EAP for Greece marked a pivotal stage in the reorganisation of the country’s financial system. The adopted strategy distinctly favoured core systemic banks over non-core institutions.49 Specifically, core banks were eligible to receive recapitalisation funds from the HFSF, while non-core banks were required to secure capital exclusively from private sources (European Union, 2013, p. 37). In conjunction with increased capital requirements and the designation of core banks as “integrators of smaller domestic banks” (European Union, 2013, p. 37, para. 58), these measures facilitated a more concentrated and monopolistic structure within the Greek banking sector. This consolidation was further evidenced by the dissolution of state banks such as Hellenic Postbank and the sale of Emporiki and Geniki, alongside the expansion of private bank portfolios, as exemplified by Piraeus Bank’s acquisition of the BCP Portugal subsidiary. The strengthening of bank portfolios and solvency was also critically linked to the removal of restrictions on home foreclosures (Law 4224/2013), a measure introduced to address the surge in non-performing loans (NPLs), which reached 39.9% in April 2014.50 This period also saw Greece’s return to the international bond market with the issuance of a new five-year bond after a four-year absence.51 Additionally, the political leadership of the EMU, actively encouraged the transfer of cooperative bank assets to core private banks, thereby consolidating their dominance in the sector (European Union, 2014, p. 46, para. 83).

The extension of the Master Financial Assistance Facility Agreement for Greece on 18 February 2015 followed the unsuccessful attempt by the SYRIZA government to renegotiate EMU rules, compelling Greece to sign a new Memorandum of Understanding (MoU) under the European Stability Mechanism (ESM) for a three-year period.52 The immediate priorities outlined in the MoU included the resolution of NPLs and the completion of bank recapitalisation (European Union, 2015, p. 18). The MoU promoted private management and strategic investment in banks recapitalised with public funds, thereby fostering the emergence of robust private credit institutions reliant on public resources, yet serving private interests. Notably, systemic banks were not only recapitalised through the HFSF but also received additional capital injections in the form of common shares and convertible capital.53

Parallel to these developments, a new NPL framework was established54, facilitating rapid reforms of corporate and household insolvency laws to accelerate NPL resolution and promote the development of “sales markets” for distressed assets (European Union, 2015, pp. 8, 18–19). Law 4354/2015 (FEK A 176) liberalised the sector by enabling the licensing and regulation of non-bank servicers and facilitating loan transfers.55 Furthermore, the Government Council for Private Debt Management was introduced as a purpose-specific institutional structure.56

A clear indication of Greece’s ongoing dependency on the Troika and EU institutions is reflected in the composition of the selection panel for the leadership of the HFSF, wherein 50% of the “independent” experts were appointed by the lending institutions.57

The primary objective of the comprehensive restructuring of the Greek financial sector was explicitly articulated as “strengthening the balance sheets of banks and (to) enable the return of domestic credit to the Greek economy” (European Union, 2015).58 The Supplemental Memorandum of Understanding (MoU) of June 2016 provides a striking illustration of the prioritisation of banking sector stability over potential social needs, as promoted by the international lenders. It stipulated:

“No unilateral fiscal or other policy actions will be taken by the authorities, which would undermine the liquidity, solvency or future viability of the banks. All measures, legislative or otherwise, taken during the Programme period that may have an impact on banks’ operations (i.e., solvency, liquidity, asset quality etc.) should be taken in close consultation with the EC/ECB/IMF and where relevant the ESM” (European Union, 2016).

In alignment with these priorities, the finalisation of the NPL framework enabled the sale of distressed Greek assets—including loans secured by primary residences—to VFs.59 The non-performing exposure (NPE) ratio of the four core Greek banks remained elevated at 45%. To address this, an out-of-court framework was introduced, ostensibly to facilitate equitable solutions between creditors and debtors.60 However, in practice, these mechanisms primarily expedited debt restructuring and minimised creditor losses (Mesnard et al., 2016). Furthermore, the acceleration of “liquidation of non-viable businesses to support the recovery of the economy” was legislated, while electronic auctions were implemented to overcome enforcement bottlenecks that hindered creditor recovery.61

The supplement to the MoU of 2017 further entrenched the bias in favour of core banks by advocating for the reduction of “existing tax disincentives regarding loan loss provisioning and write-off policies of domestic banks, thus supporting bank efforts to reach the above targets on NPE resolution” (European Union, 2017).62 Additionally, in-court insolvency procedures were streamlined through the appointment of new support staff to address the backlog of household insolvency cases under Law 3869/2010.63

With a primary budget surplus reaching 4% of GDP—exceeding the ESM target of 2.5%—Greece was on track to formally exit the EAP in August 2018.64 The four core banks (Alpha Bank, Eurobank, National Bank of Greece, and Piraeus Bank) ultimately achieved the positions envisaged under the adverse scenario, as the secondary NPL market became operational and two banks completed NPL sales.65

In conclusion, the structural reform of Greece’s financial framework, the transfer of NPLs to a newly established secondary market dominated by VFs, and the implementation of out-of-court workouts, electronic auctions, and reformed insolvency frameworks collectively facilitated the consolidation and preservation of core banks. These measures, alongside accelerated debt restructuring and the liquidation of non-viable businesses, were embedded in law and rigorously enforced to promote economic recovery, supported by a series of bank resolutions, mergers, and recapitalizations.

Table 4.

Key Events and Relationships in the EAP-Driven Reconfiguration of the Greek Banking Sector.

Table 4.

Key Events and Relationships in the EAP-Driven Reconfiguration of the Greek Banking Sector.

| Sequence/Stage | Key Event/Policy | Description & Relationships |

|---|---|---|

| 1. Pre-Crisis & Initial Shock | Global Financial Crisis (2008–2009) | Exposed vulnerabilities in Greece; banking sector not original source of instability (EU, 2010: 6) |

| Loss of Market Access | Banks lose wholesale market access by end-2009; deposit outflows; reliance on ECB refinancing (EU, 2010: 23) | |

| 2. First EAP (2010–2012) | Programme Objective | Restore credibility, fiscal sustainability, financial system stability, growth (EU, 2010: 11) |

| ECB Collateral Policy | ECB accepts Greek government debt as collateral, regardless of rating (EU, 2010: 35) | |

| Banking Sector Measures | Liquidity support, recapitalisation (competition-compliant), HFSF established, restructuring plan | |

| Strategic Review | HSBC, Deutsche Bank, Lazard propose mergers, privatisation, liquidation (EU, 2010: 24) | |

| Labour Reform | New law allows banks to negotiate employment directly (EU, 2010: 25) | |

| Forced Restructuring | Viable banks recapitalised; non-viable dissolved (e.g., TT Bank resolved; assets to Postbank/Proton Bank) (EU, 2012: 3–4) | |

| Government Exit | Gradual withdrawal from banking sector | |

| 3. Fiscal/Structural Adjustment & Recession | Austerity & Contraction | Recession “deeper and longer” than projected; credit contracts; NPLs rise (EU, 2011: 1, 76) |

| Sovereign Debt Restructuring | Capital shortfalls; targeted recapitalisation strategy | |

| 4. Second EAP (2012–2015) | Programme Focus | Debt sustainability, competitiveness, fiscal consolidation, privatisation, structural reforms |

| Troika Task Force | Permanent presence in Greece | |

| Constitutional Amendment | Prioritises external debt servicing over social needs | |

| NPLs Escalate | NPLs reach 15.5% by 2011 | |

| Private Sector Involvement (PSI) | 53.5% haircut for bondholders; funds for bank recapitalisation; PSI-II causes further bank losses (€43bn) (EU, 2012: 17–18) | |

| Core Bank Strategy | Core banks recapitalised via HFSF; non-core banks to seek private capital (EU, 2013: 37) | |

| Market Consolidation | Core banks as “integrators”; state banks dissolved/sold; private banks expand (Piraeus acquires BCP Portugal subsidiary); cooperative assets transferred to core banks (EU, 2014: 46, para. 83) | |

| Foreclosure Reform | Law 4224/2013 lifts restrictions to address NPLs (39.9% in 2014) | |

| Return to Bond Market | New 5-year bond issued after four years | |

| MoU (ESM, 2015) | Prioritises NPL resolution, recapitalisation, private management/strategic investment in recapitalised banks (EU, 2015: 18) | |

| NPL Framework | Rapid reform of insolvency laws; “sales markets” for distressed assets (EU, 2015: 8, 18–19); Law 4354/2015 enables non-bank servicers/loan transfers; Government Council for Private Debt Management created | |

| Troika/EU Influence | HFSF leadership panel: 50% appointed by lenders | |

| 5. Supplemental MoUs & Final Developments (2016–2018) | Supplemental MoU (2016) | No unilateral national actions undermining banks; all measures to be coordinated with EC/ECB/IMF/ESM (EU, 2016) |

| NPL Market Finalised | Sale of distressed assets (including primary residences) to Private Debt Investors; NPE ratio at 45% | |

| Out-of-Court Framework | Expedites debt restructuring, minimises creditor losses | |

| Liquidation/E-Auctions | Accelerated liquidation of non-viable businesses; electronic auctions for enforcement | |

| MoU Supplement (2017) | Reduces tax disincentives for loan loss provisioning/write-offs; more staff for household insolvency cases (Law 3869/2010) | |

| Fiscal Surplus & Exit | Primary surplus >4% GDP; Greece exits EAP (Aug 2018); four core banks achieve envisaged positions; secondary NPL market operational; NPL sales completed | |

| 6. Outcome | Consolidation & Recovery | Core banks preserved/consolidated; NPLs transferred to secondary market; reforms embedded in law; economic recovery promoted via resolutions, mergers, recapitalisations |

4. Discussion

This article sought to examine how the interplay between the BU, CMU, and EAPs has reshaped the financial sectors of Greece and Cyprus. Through comparative analysis, the study finds that these EU initiatives have intensified core–periphery disparities, consolidating financial power among a few credit institutions and facilitating the entry of private debt investors. The resulting concentration of wealth and persistent debt dependency have reinforced structural inequalities, privileging core interests while peripheral economies bear the costs. The findings highlight the need for broader, more inclusive reforms to address financial divergence and promote equitable integration within the euro area. The BU and CMU initiatives constitute pivotal elements in the ongoing transformation of the euro area’s political economy, as highlighted by Epstein and Rhodes (2018). This transformation is marked by the centralisation of regulatory and supervisory powers over major banking institutions at the EMU level (De Rynck, 2016), coupled with a relaxation of regulatory constraints on market mechanisms at the supranational tier. Such a reconfiguration has disproportionately favoured large, core systemic banks and facilitated the entry and expansion of PDIs within the distressed economies of the EMU periphery. Rather than mitigating structural disparities, the BU has, in practice, engendered “asymmetric effects” (Quaglia, 2019) that have exacerbated peripheral vulnerabilities.

The acceleration of financialisation—encompassing both bank-based and capital market-based modalities—has been catalysed by reforms targeting PDIs and the restructuring of major banking institutions in peripheral economies. These reforms have allowed both traditional banks and alternative capital providers to consolidate their market dominance. Consequently, leading systemic CIs in the periphery have amassed substantial power through the accumulation of privately owned assets, a development propelled by comprehensive restructuring measures such as recapitalisation, resolution of state-owned banks, mergers and acquisitions, and legislative changes affecting household and corporate debt, as well as the legalisation of secondary market involvement in NPL management. These restructuring initiatives, implemented at both the EMU and EAP levels, have reinforced the concentration of financial power. More specifically, as shown, despite a reduction in the number of banking offices and employees, the assets—and thus the wealth and influence—of leading CIs in Greece and Cyprus have increased and become concentrated in fewer financial centres, a tendency more pronounced in the periphery rather than in core euro area countries, Germany and France. This consolidation has occurred irrespective of the sector’s overall downsizing, resulting in the emergence of a privileged class of financial actors in the EMU periphery. The BU has provided a clear avenue for risk-seeking profit maximisation within the banking sector. Moreover, the policy of encouraging PDIs to acquire NPLs at discounted prices, as promoted by both the BU and CMU, has entrenched debt dependency in the periphery, extending it to the euro area core and to international actors, notably US-based VFs The interplay between the BU, CMU, and EAP-driven reforms has thus reinforced two principal tendencies: the emergence of wealthier, more concentrated core credit institutions in the periphery, and the further opening of peripheral markets to international, predatory investors, facilitating the extraction of surplus value and profits from these economies. This dynamic constitutes a form of rent extraction at the expense of peripheral populations, who have borne the costs of banking system rescues. The resultant euro area context, as previously argued, reflects the imperatives of transnational capital and replicates core-periphery dependency relations historically observed in Latin America (Epstein & Rhodes, 2018; De Rynck, 2016; Quaglia, 2019).

This study is subject to limitations. Notably, the unavailability of ESB Banking Structural Financial Indicators beyond 2021 constrained the temporal scope of the empirical analysis. Furthermore, the research focused on a selective set of financial indicators, which, while illustrative, do not capture the full complexity of financial divergence within the euro area. The findings should therefore be interpreted as indicative rather than exhaustive. Nevertheless, by integrating empirical sectoral data with institutional and critical analysis of EAP-driven restructuring and supranational financial integration initiatives, the study provides clear evidence of the unprecedented consolidation of banking assets among a limited number of CIs and the proliferation of private debt investors in the periphery.

Future research should seek to address these limitations by incorporating a broader range of structural financial indicators and extending comparative analyses between core and peripheral euro area countries. Such an approach would contribute to a more holistic understanding of financial divergence and inform policy debates on “reforming the reforms” in the euro area periphery, with an emphasis on reducing social risk and promoting equitable financial integration.

Funding

This research received no external funding.

Data Availability Statement

Data supporting reported results can be found at ECB European Central Bank. (2021). SSI: Banking structural financial indicators. https://sdw.ecb.europa.eu/browse.do?node=9689719 ; European Stability Mechanism-Conditionality Dashboard https://www.esm.europa.eu/financial-assistance/programme-database/conditionality; Deloitte. (2019, October). Deleveraging Europe. Financial Advisory. https://www2.deloitte.com/content/dam/Deloitte/uk/Documents/corporate-finance/deloitte-uk-deleveraging-europe-2019.pdf. Data analysed can also be found in several other sources cited in the reference section.

Acknowledgments

During the preparation of this study, the author

used Read AI to improve the structure of the article and the readability of the

article’s tables. The author has reviewed and edited the output and takes full

responsibility for the content of this publication.

Conflicts of Interest

The author declares no conflicts of interest.

Abbreviations

The following abbreviations are used in this manuscript:

| AGM | Apollo Global Management |

| BRRD | Bank Recovery and Resolution Directive |

| BU | Banking Union |

| CIs | Credit Institutions |

| CMU | Capital Markets Union |

| CRDIV/CRR | Capital Requirements Directive and Regulation |

| DGSs | Deposit Guarantee Schemes |

| EAPs | Economic Adjustment Programmes |

| EMU | Economic Monetary Union |

| ESM | European Stability Mechanism |

| EFSF | European Financial Stability Facility |

| EU | European Union |

| IMF | International Monetary Fund |

| MoUs | Memorandum of Understanding |

| NPLs | non-performing loans |

| PDIs | Private Debt Investors |

| SSM | Single Supervisory Mechanism |

| SRM | Single Resolution Mechanism |

| VFs | Vulture Funds |

| UK | United Kingdom |

References

- Amin, S. (1988). Eurocentrism. London: Zed Press.

- Amin, S. (1996). The challenge of globalization. Review of International Political Economy, 3(2), 216–259. [CrossRef]

- Amin, S. (2019). The new imperialist structure. Monthly Review, 71(3). [CrossRef]

- Apergis, N., Fafaliou, I., & Polemis, M. L. (2016). New evidence on assessing the level of competition in the European Union banking sector: A panel data approach. International Business Review, 25(1), 395–407. [CrossRef]

- Apollo Offshore Credit Strategies Fund Ltd. (n.d.). European overview. https://www.apollo.com/site-services/european-overview.

- Apollo takes over Citi’s global real estate funds platform. (2010, November 15). https://realassets.ipe.com/apollo-takes-over-citis-global-real-estate-funds-platform/37924.article.

- AURA Real Estate Experts. (2019, June 6). Greece: doBank buys servicing licence and is renamed to doValue. https://www.auraree.com/greece/real-estate-news/greece-dobank-buys-servicing-licence-and-is-renamed-to-dovalue/.

- AURA Real Estate Experts. (2019, November 13). Funds flood the market with real estate. https://www.auraree.com/greece/real-estate-news/funds-flood-the-market-with-real-estate/.

- AURA Real Estate Experts. (2020, January 30). NPL servicers have started the sales of real estate. https://www.auraree.com/greece/real-estate-news/npl-servicers-have-started-the-sales-of-real-estate/.

- Avlijaš, S., Hassel, A., & Palier, B. (2021). Growth strategies and welfare reforms in Europe. In Growth and welfare in advanced capitalist economies: How have growth regimes evolved (pp. 372-436).

- Baiardi, D., & Morana, C. (2018). Financial development and income distribution inequality in the euro area. Economic Modelling, 70, 40-55. [CrossRef]

- Bank of Cyprus confirms Apollo NPLs sale. (2018, August 31). https://www.news.cyprus-property-buyers.com/2018/08/31/bank-of-cyprus-confirms-apollo-npls-sale/id=00154648.

- Bank of Cyprus Holdings. (2020, August 3). Agreement for sale of a portfolio of non-performing loans. https://www.bankofcyprus.com/globalassets/investor-relations/press-releases/eng/20200803-helix2announcement_eng_final.pdf.

- Bavoso, V. (2019). [Review of the book Capital Markets Union in Europe, by D. Busch, E. Avgouleas, & G. Ferrarini (Eds.)]. Journal of International Banking Law & Regulation, 34(5), 183–185.

- Bayoumi, T., & Eichengreen, B. (1993). One money or many? On analyzing the prospects for monetary unification in various parts of the world.

- Becker, J., Jäger, J., Leubolt, B., & Weissenbacher, R. (2010). Peripheral financialization and vulnerability to crisis: A regulationist perspective. Competition & Change, 14(3–4), 225–247. [CrossRef]

- BloombergQuint. (n.d.). HSBC reaches agreement to sell Greek bank branches to Pancreta. https://www.bloombergquint.com/business/hsbc-reaches-agreement-to-sell-greek-bank-branches-to-pancreta.

- Bryant, C. (2011, September 29). German banks can stomach Greek debt. Financial Times. https://www.ft.com/content/7cbdc3f4-e9f0-11e0-b997-00144feab49a.

- Campos, N. F., & Macchiarelli, C. (2021). The dynamics of core and periphery in the European monetary union: A new approach. Journal of International Money and Finance, 112, 102325. [CrossRef]

- Cheng, G. (2020). The 2012 private sector involvement in Greece. Publications Office of the European Union.

- Corporate Finance Institute. (n.d.). What are vulture funds? https://corporatefinanceinstitute.com/resources/knowledge/trading-investing/vulture-funds/.

- Costamagna, F. (2012). Saving Europe under strict conditionality: A threat for EU social dimension? Centro Einaudi – Comparative Politics and Public Philosophy Lab, Working Paper- LPF 7/12.

- Council of the EU. (2016, June 17). Council conclusions on a roadmap to complete the Banking Union (Press Release).

- Council of the EU. (2017, July 11). Council conclusions on action plan to tackle non-performing loans in Europe. https://www.consilium.europa.eu/en/press/press-releases/2017/07/11/conclusions-non-performing-loans/.

- Council of the EU. (2017, July 11). ECOFIN Council in July 2017. https://www.consilium.europa.eu/en/press/press-releases/2017/07/11/conclusions-non-performing-loans/.

- Council of the European Union. (2010, May 9–10). Economic and Financial Affairs: Extraordinary Council meeting (Press Release 9596/10).

- Creel, J., & El Herradi, M. (2024). Income inequality and monetary policy in the euro area. International Journal of Finance & Economics, 29(1), 332-355.

- De Grauwe, P., & Ji, Y. (2020). Structural reforms, animal spirits and monetary policies. European Economic Review, 124, Article 103395. [CrossRef]

- De Rynck, S. (2016). Banking on a union: The politics of changing eurozone banking supervision. Journal of European Public Policy, 23(1), 119-135. [CrossRef]

- Deloitte. (2019, October). Deleveraging Europe. Financial Advisory. https://www2.deloitte.com/content/dam/Deloitte/uk/Documents/corporate-finance/deloitte-uk-deleveraging-europe-2019.pdf.

- Denk, O., & Cournède, B. (2015). Finance and income inequality in OECD countries. OECD Economics Department Working Papers, No. 1224, OECD Publishing.

- Deutschmann, C. (2011). Limits to financialization: Sociological analyses of the financial crisis. European Journal of Sociology/Archives Européennes de Sociologie, 52(3), 347-389.

- Donnelly, S. (2018). Liberal economic nationalism, financial stability, and Commission leniency in Banking Union. Journal of Economic Policy Reform, 21(2), 159–173. [CrossRef]

- Epstein, G. A. (Ed.). (2005). Financialization and the world economy. Edward Elgar Publishing.

- Epstein, G., & Jayadev, A. (2005). The rise of rentier incomes in OECD countries: Financialization, central bank policy and labor solidarity. In G. Epstein (Ed.), Financialization and the world economy (pp. 46–74). Edward Elgar.

- Epstein, R., & Rhodes, M. (2018). From governance to government: Banking union, capital markets union and the new EU. Competition & Change, 22(2), 205–224. [CrossRef]

- Eurogroup. (2016, May 9). Eurogroup statement on Greece. https://www.consilium.europa.eu/en/press/press-releases/2016/05/09/eg-statement-greece/.

- European Central Bank. (2021). SSI: Banking structural financial indicators. https://sdw.ecb.europa.eu/browse.do?node=9689719.

- European Commission. (2012). Communication from the Commission to the European Parliament and the Council: A roadmap towards a banking union (COM/2012/0510 final).

- European Commission. (2015). Commission staff working document: Economic analysis accompanying the document Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions Action Plan on Building a Capital Markets Union (SWD/2015/0183 final).

- European Commission. (2015, August 11). Memorandum of understanding between the European Commission acting on behalf of the European Stability Mechanism and the Hellenic Republic and the Bank of Greece. https://ec.europa.eu/info/sites/default/files/01_mou_20150811_en1.pdf.

- European Commission. (2015, August 14). Report on Greece’s compliance with the draft MOU commitments and the commitments in the Euro Summit statement of 12 July 2015.

- European Commission. (2016, June 16). Supplemental memorandum of understanding.

- European Commission. (2017). Factsheet: Completing the banking union.

- European Commission. (2017, July 5). Supplemental memorandum of understanding (second addendum to the memorandum of understanding) between the European Commission acting on behalf of the European Stability Mechanism and the Hellenic Republic and the Bank of Greece (p. 26). https://ec.europa.eu/info/sites/default/files/smou_final_to_esm_2017_07_05.pdf.

- European Commission. (2018, June 20). Supplemental memorandum of understanding: Fourth review of the ESM Programme [Draft].

- European Commission. (n.d.). Supplemental memorandum of understanding: Greece third review of the ESM Programme. https://ec.europa.eu/info/sites/default/files/economy-finance/third_smou_-_final.pdf.

- European Commission, Directorate-General for Economic and Financial Affairs. (2010). The economic adjustment programme for Greece: First review – summer 2010 (Occasional Papers 68/August 2010).

- European Commission, Directorate-General for Economic and Financial Affairs. (2010). The economic adjustment programme for Greece: Second review – autumn 2010 (Occasional Papers 72).

- European Commission, Directorate-General for Economic and Financial Affairs. (2011). The economic adjustment programme for Greece: Third review – winter 2011 (Occasional Papers 77).

- European Commission, Directorate-General for Economic and Financial Affairs. (2011). The economic adjustment programme for Greece: Fourth review – spring 2011.