Submitted:

20 November 2024

Posted:

21 November 2024

You are already at the latest version

Abstract

The European Union’s (EU) Corporate Sustainability Reporting Directive expanded its Non-Financial Reporting Directive requirements to companies with over 250 employees, mandating their sustainability reporting from 2025. This expansion will exceed the number of companies subject to mandatory reporting, presenting new challenges for managers and responsible employees. Companies will have to report according to the European Sustainability Reporting Standards. The Erasmus+ project "Smart Education for Corporate Sustainability Reporting" (SECuRe) addressed gaps in vocational education and training (VET) programs related to sustainability knowledge and reporting. It aimed to establish a unified approach for VET teachers and learners across the EU, preparing them for the evolving job market demands. The project began by developing a knowledge repository and questionnaire, focusing on current reporting practices and job requirements, and continued with the preparation of materials for the training course. The course encompassed six learning units: 1) European legislation and sustainability standards, 2) sustainability management, 3–5) environmental, social, and corporate dimensions, and 6) sustainability reporting. The initiative included multiplier events, pilot applications, and course online tests. To deliver the course effectively, the project utilized an interactive e-learning platform with gamification elements and other engaging activities to enhance learning outcomes.

Keywords:

sustainability

; corporate reporting

; EU directive

; education

; e-learning

1. Introduction

The Brundtland Commission's definition of sustainable development as “meeting the needs of the present without compromising the ability of future generations to meet their own needs.” is general, it does not provide guidance on how to implement action [1]. Subsequently, many concepts have been developed that address corporate sustainability and consider the triple bottom line (people, planet, profit), including corporate sustainability reporting. However, mainstreaming corporate sustainability, e.g., with the circular economy concept, can lead to different results depending on which targets or indicators of sustainable development goals (SDGs) the company selects [2].

For this reason, many authors have emphasized the need for alignment of the different reporting frameworks [3]. Mandatory disclosure of information is usually accompanied by an increase in its credibility and a focus on a wide range of stakeholders, not just shareholders [4]. As a result, companies also tend to disclose more social and environmental information after initially achieving higher profits by adopting sustainability practices [5]. A new need has emerged for companies to communicate their sustainability in corporate reports also in a graphic way with symbols [6]. The next step in corporate sustainability reporting was a paradigm shift from standardized disclosures to an understanding of sustainability – staying within the planet's boundaries [7,8].

The creation of new job profiles with corresponding competencies can effectively support the implementation of sustainability concepts in the value chain [9].

In 2019, the European Commission launched an ambitious initiative “The European Green Deal”, EGD [10] as an integral part of the United Nations Agenda 2030 and its SDGs [11]. Reliable, comparable, and verifiable information plays an important part in enabling consumers to make more sustainable decisions and reduces the risk of ‘greenwashing’. As a part of the EGD initiatives, companies are required to report against a standard methodology and to assess their impact on the environment. The Non-Financial Reporting Directive, NFRD [12] laid down the rules on disclosure of non-financial information by companies and was fully transposed in all EU Member States (including partners’ countries). However, as the reporting obligation applied to certain types of companies (over 500 employees), only, the proportion of businesses disclosing non-financial information was low. Moreover, several problems were identified, raising a question mark on the company’s capacity in delivering such reports; various analyses revealed that in many cases, information was provided at a general level and/or data were incomplete and non-comparable.

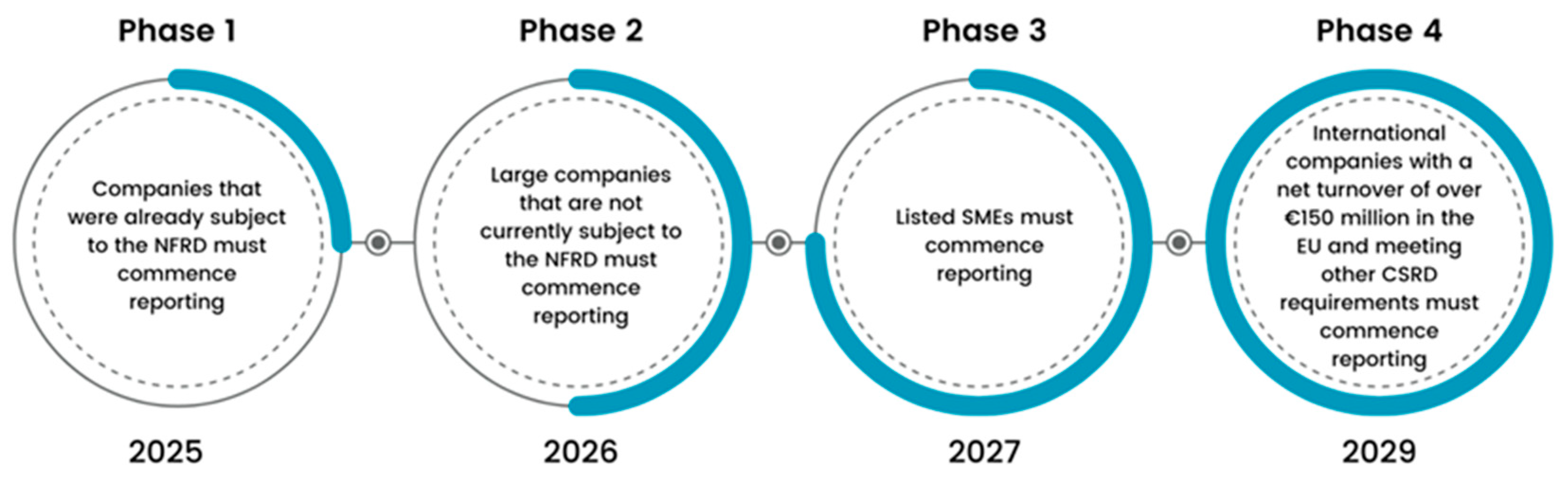

In 2022, the EU reached an agreement to replace the NFRD with the Corporate Sustainability Reporting Directive (CSRD) [13] that extends its scope to companies with over 250 employees and certain small and medium-sized enterprises (SMEs) which will be required to report on nonfinancial aspects of their business – the first time in 2025 for the financial year 2024 (European Parliament, 2022). During the years 2025–2029 (Figure 1), the number of companies, subject to the mandatory reporting will thus increase from 11 700 to approximately 50 000. The managers and responsible employees will have to cope with new challenges.

EU law requires all large companies and all listed companies (except listed micro-enterprises) to disclose information on their risks and opportunities arising from social and environmental issues and disclose the impacts of their activities on people and the environment. This will help investors, civil society organisations, consumers, and other stakeholders to evaluate the sustainability performance of companies, as part of their environmental, social, and governance (ESG) assessment. Under the NFRD, large companies must publish information related to a) environmental matters, b) social matters and treatment of employees, c) respect for human rights, d) anti-corruption and bribery, and e) diversity on company boards (in terms of age, gender, educational and professional background). The reporting rules apply to large companies and groups across the EU, including listed companies, banks, insurance agencies, and others designated by national authorities as public-interest companies.

Guidelines on NFR were published by European Commission [15,16] to help large companies disclose environmental and social information. These guidelines were not mandatory, and companies might decide to use international, European, or national guidelines according to their own characteristics or business environment.

The CSRD modernizes and strengthens the rules about the social and environmental information that companies must report. A broader set of companies are now required to report on sustainability – about 50 000 companies in total, corresponding to 75 % of their turnover:

- All large companies (regardless of capital market orientation) that meet at least two of the following three requirements: 250 or more employees; 40 MEUR (million EUR) in net turnover; and/or 20 MEUR in assets.

- All listed companies on EU-regulated markets. This applies also to companies not established in the EU but listed in EU-regulated markets generating a net turnover of 150 MEUR and which have at least one subsidiary or branch in the EU.

- Small and Medium Enterprises (SMEs) listed on EU-regulated markets from the financial year 2026. SMEs will have separate, less rigorous standards compared to the ones applied to large companies – they must report in 2027 for the financial year 2026.

- Micro-enterprises with less than 10 employees or under 20 MEUR are the only ones not covered by the CSRD.

The new rules will ensure that investors and other stakeholders have access to the information they need to assess investment risks arising from climate change and other sustainability issues. They will also create a culture of transparency about the impact of companies on people and the environment. Finally, reporting costs will be reduced for companies in medium to long term by harmonizing the information to be provided.

Companies subject to the CSRD must report according to the European Sustainability Reporting Standards, ESRSs, prepared by the European Financial Reporting Advisory Group, EFRAG [17]. The CSRD also makes it mandatory for companies to have an audit to verify the reported information. In addition, it provides for the digitalization of sustainability information. The rules introduced by the NFRD remain in force until companies must apply the new rules of the CSRD.

The EU taxonomy is a classification system, establishing a list of environmentally sustainable economic activities. It could play an important role in helping the EU scale up sustainable investment and implement the EGD. The EU taxonomy would provide companies, investors, and policymakers with appropriate definitions for which economic activities of companies can be considered environmentally sustainable. In this way, it should create security for investors, protect private investors from greenwashing, help companies to become more climate-friendly, mitigate market fragmentation and help shift investments where they are most needed. The Taxonomy Regulation establishes six environmental objectives: 1) Climate change mitigation and 2) Adaptation, 3) Sustainable use and protection of water and marine resources, 4) Transition to a circular economy, 5) Pollution prevention and control, and 6) Protection and restoration of biodiversity and ecosystems.

Educational initiatives play a pivotal role in fostering corporate sustainability re-porting, equipping professionals with the necessary skills and knowledge to navigate this complex field. The SECuRe project focuses on developing a vocational course centered on sustainability strategies and related activities, aiming to enhance participants' understanding of sustainable practices and their implementation in corporate settings. Moreover, the Global Reporting Initiative (GRI) Academy offers a comprehensive training program on impact reporting, allowing individuals to stay abreast of global sustainability trends and reporting standards [18]. These courses often begin by offering a broad overview of sustainability concepts and gradually delve into specific corporate sustainability strategies, enabling participants to grasp the nuances of sustainability reporting in the current business landscape and its future implications.

These courses provide a thorough understanding of essential concepts in corporate sustainability by using case studies and video examples, enriching the learning experience, and promoting practical application. Education programs aim to empower learners to become change agents for sustainability by providing them with the skills needed to drive meaningful transformations within their organizations and beyond [19].

Integrating sustainability education into corporate reporting not only fosters a culture of environmental and social responsibility but also paves the way for innovation and strategic growth aligned with SDGs. The findings underscore the significance of education as a catalyst for sustainable business practices and highlight the need for continuous learning and development in promoting corporate sustainability reporting.

2. Methods

The methodology ADDIE (Analysis/Design/Development/Implementation/Evaluation) [20], an instructional systems design framework for the development of training courses, was used to elaborate the SECuRe Course. We applied the following activities in the methodological steps in our output:

- Analysis phase (specify the problems to be solved, find the needs and objectives, actual and desired skills, knowledge, and abilities, and define learning goals).

- Design phase (specification of learning objectives, elaboration of the course curriculum and structure, delivery methods, instructional strategies).

- Development phase (creation of the content, development of e-learning and communication strategy, testing the learning product outcomes and training materials).

- First evaluation phase (training the trainers, course delivery, communication with learners and their support).

- Implementation phase (evaluation of the design, procedures for training teachers and learners, improving the course curriculum, learning outcomes, method of delivery and testing procedures, including new software or hardware tools).

- Second evaluation phase (pilot application with demo training), and final assessment using several experimental online trainings).

For assessing the e-learning platform during the demo training, we applied the Usability lab methodology [21] in our evaluation as an innovative element. In literature, usability shows how efficiently users can apply a product, a brochure, an application, a website, a software package, or a video game to achieve their goals. The purpose of the practice is to discover any missed requirements or any kind of development that seems to be intuitive but ends up by confusing inexperienced users.

The theoretical side of the project methodology consisted of literature search which is presented in the Knowledge Repository (KR). It is an online database that systematically captures, organizes, and categorizes knowledge-based information. KR has a user-friendly structure and is included into the website of the project as an unrestricted access, to establish an active link between the project and the users’ community.

The practical methodology included partners’ overviews of the situation in their countries regarding the state-of-the-art in the usage of NFRD, and preparative activities for the CSRD introduction. Information regarding stakeholders’ needs and barriers was collected by at least fifteen respondents from each partner country, based on a targeted questionnaire. The developed course was assessed, evaluated, and improved in several consecutive steps: a) joint staff training and course pilot; b) five multiplier events, one in each country, c) intermediate and d) final tests of the course in each partner country.

3. Results

Project results include: 1) Knowledge Repository, 2) development of the VET course for holistic, strategic, and sustainable performance, 3) development of the project web page, including an alternative e-learning platform for the course, 4) pilot application of the course, 5) experimental online training and 6) lifelong learning with micro-credentials experience.

The project target group was including VET providers, environmental associations, local authorities, job finding/creation associations, employee agencies and associations, VET learners/students in the environment, engineering, manufacturing, process and technology, or business management programs, professionals from industry, financial and public institutions, interested to enrich their interdisciplinary skills and knowledge in the field of sustainability and in particular, the CSR and SDGs reporting.

The project web page (https://platform.csr-secure.eu/) is including an interactive e-learning platform for the course from which users can access the Knowledge Repository and the course material used for training for free. Offering learning material online is essential to reach a broad target group, and to introduce future oriented ideas, concepts and skill sets to the market. The possibility of following daily activities remotely is of high importance. At the same time, the platform serves as a network of internal users, enabling course participants to communicate, and to learn from the ideas, skill sets, and experiences of others enrolled in the course. By engaging in a shared task, course participants gain the opportunity to learn a variety of skills that are essential to managers, such as group analysis and collaborative team building. The platform is available in English and five languages of partner countries, allowing a broad application in companies. The database includes the name of the source, a short description and a link to the document and will be an open source on the project online platform available in all project languages.

The Knowledge Repository (https://csr-secure.eu/knowledge/) helps learners to connect with information and expertise globally via online searchable libraries, by providing a central location to collect, contribute and share digital learning resources for use. It includes scientific research, webpages, case studies, and databases. KR is available in English and in five partners’ languages (Czech, Polish, Romanian, Slovenian, and Spanish). The search can be filtered by the year of publication (2004–2024), by access type (free, payable), by 14 resource types (e.g., article, book, legislation, standard, video, regular course or training, tool, best practice or case study, web site), or by 39 keywords (e.g., circular economy, climate change, corporate sustainability, disclosures, ESG, EU taxonomy, GHG protocol, GRI, SDG, social responsibility, sustainability reporting). ESRSs as presented by EFRAG were included in the web, too.

3.1. State-of-the-Art Review

Overviews from partner countries indicated that most large companies were publishing annual NFR information, either nationally or as a member of an international group. The following trends in environmental, social and governance (ESG) reporting have been observed:

- Reporting companies have a clear preference for communicating ESG information via a separate report than including this data in their annual financial reports.

- There is a growing interest in using recognized reporting standards like the GRI standards.

- Only in few reports, an opinion is issued by an independent verifier. In most cases, the opinion is of limited assurance and relates to a narrow set of indicators.

- Concerns about climate change are increasing at the local level with targets for reducing greenhouse gas (GHG) emissions. But only a few companies are reporting at the local level on the risks associated with climate change.

The results show that companies are increasingly following the Task Force on Climate-related Financial Disclosure (TCFD) by accepting their recommendations [22]:

- Companies increasingly disclose climate-related information in their filings.

- Preparers and users of disclosure increasingly view climate-related issues as mainstream business and investment considerations.

- The number of companies implementing the recommendations grows, and the types of information disclosed are further developed.

- Disclosures are becoming more complete, and there is more appropriate pricing of climate-related issues.

3.2. Questionnaire Results

The aim of the research was to understand the state of knowledge in companies, their needs, and the main barriers. Therefore, a questionnaire with 37 open and closed questions was sent to stakeholders in each partner country. 77 of them responded. Most of the responders were managers or experts on sustainability issues from large companies and SMEs. Their responses indicated that the environmental dimension and sustainability management were the most frequently reported issues, while the social and governance dimensions were less frequently reported. 52 % of the companies were not familiar with the European CSR guidelines. Companies listed customers as the most important stakeholders, followed by company owners, investors, or banks. 43 % of companies were not required to report non-financial data, and 55 % of them did not have a person responsible for sustainability reporting. The most important constraints in corporate sustainability reporting were missing knowledge (30 %), and lack of data (25 %).

3.3. Training Course Contents

The course is addressing the area of VET, and combines academic perspective with hands-on practical work, giving the participants the knowledge, skills and experience they need to develop a career in sustainability and specifically in being able to develop sustainable management and reporting services”. The training content is designed to give participants the opportunity to develop clear alternatives for professional organizations to secure a sustainable future in economic, environmental, and social terms.

Six learning units (LUs) have been developed. Each one starts with a job profile and expected learning outcomes – knowledge, skills, and competencies. The learning outcomes are structured in accordance with the standards outlined in the European Qualifications Framework, EQF, and the European credit system for VET, ECVET [23]. The LUs have a value of 5 ECTS (European Credit Transfer and Accumulation System) with 25 h (hours) duration each.

The six main topics of the course are including:

- 1)

- European and international legislation, and sustainability standards (introducing key elements of the EU Directive and global regulations, and the most important European and world standards for sustainability reporting of companies and financial market participants). Corporate sustainability reporting is the process by which companies communicate their ESG performance, and it is becoming increasingly important. Reporting involves disclosing information about a company's activities related to sustainability, reducing greenwashing and increasing transparency. Reports often include information about the company’s sustainability goals, strategies, performance indicators and how the company manages ESG risks and opportunities. Reporting on sustainability can help companies identify areas for improvement, enhance their reputation, and attract socially responsible investors and customers.

- 2)

- Sustainability management (characteristics, sustainability as strategy, business models for sustainability). Sustainability and environmental protection are already at the foreground of world economic and political debate, after spending decades on the periphery of public and corporate concerns. The capability to complete sustainability is increasingly regarded as a sign of a well-managed organization. As the private sector shifts toward more sustainable practices, humankind is getting closer to reaching a critical mass that can have a significant impact on the global economy. Sustainability management can also be defined as economic production and consumption that reduces environmental impact while increasing resource conservation and reuse.

- 3)

- Environmental dimension (use of resources, pollution, climate change). Companies are expected to provide detailed information on their environmental policies, strategies, targets, and performance, as well as any risks and opportunities related to environmental issues. This LU introduces basic knowledge regarding natural capital and its actual status, how to manage natural resources and biodiversity and why it is important; what are the key elements of climate change, businesses’ risks and opportunities in relation to climate change, how business can assess their GHG emissions, and plan for climate change mitigation and adaptation. Further, the overall business impact on the environment and how to measure it by using specific indicators, is presented. Finally, the unit presents the key requirements of environmental reporting and how to assess the overall environmental performance of the business.

- 4)

- Social dimension (diversity and equality, consumer protection, human rights). Human rights, cultural and other fundamental rights, and freedoms make a substantial part of the SDGs, the European Social Charter and EU sustainability legislation. Business enterprises can profoundly impact the human rights of employees, consumers, and communities wherever they operate. These impacts may be positive, such as increasing access to employment or improving public services, or negative, such as polluting the environment, underpaying workers, discriminating gender, racial or social groups, or forcibly evicting communities.

- 5)

- Corporate governance dimension (management structure, stakeholder relations). It refers to the relations between the company's management, its board, shareholders and broader stakeholders, the way in which the company's goals are achieved, the structure of its bodies and the guiding principles (internal policies) directing all its operations – from compensation, risk management, and employee treatment to financial results, reporting, and dealing with the impacts on climate, environment, human rights, etc. Corporate governance that calls for upstanding and transparent company behaviour leads a company to ethical decisions that benefit all its stakeholders.

- 6)

- Sustainability reporting (importance and benefits, legislative aspects, standards, tools and indicators of sustainable reporting). Standardization and digitization help to ensure that data is accurate, consistent, and reliable. Standardization establishes a common set of rules and guidelines for collecting, storing, and reporting data, while digitization helps to improve the efficiency and effectiveness of data management by converting data from physical to digital form. The approach to reporting can be centralized or distributed.

Many teaching and learning aids are available online, and are presented in the KR. Two user guides are available – one for students and another one for teachers. Two videos are introducing the course, the first one on the course contents, and the second one on the organization of the learning and certifications. A forum is available for discussions, and a list of abbreviations used is within reach, too.

3.4. Pilot Application

The objective of this action was to assess the resources created during development of the course (Knowledge Repository, curriculum content and training materials, and the e-learning platform). The feedback from participants closed the loop, facilitating further refinement of the products developed under the project. To test the developed VET course, demo trainings were carried out in the five partner countries.

Face to face teaching activities encompassed the content, case studies and exercises. To test the course content, the following steps were applied: Formative Evaluation was used to modify teaching and learning activities, improve student attainment and involve qualitative feedback for both learners and teachers. They focused on details of content and performance and were based on a small group evaluation. For testing the e-learning platform during the demo training, the Usability lab methodology was applied.

In all countries we reached a good balance of participants, between teachers, professionals from companies, managers, and consultants. Number of participants: Czech Republic 22, Poland 18, Romania 23, Slovenia 20, and Spain 20 – all together 103.

At the end of the day participants have been asked to provide feedback regarding the pilot course. Participants from all partner countries provided feedback to the following topics: evaluations of the Knowledge Hub, the course structure and content, the Online Platform usability, and evaluation of the training quality and procedure. The results were presented and discussed at an international conference, too [24].

The evaluation of the course across multiple countries highlighted a range of perspectives and feedback. Participants in the Czech Republic expressed concerns about practical challenges in the ESG implementation and reporting, as well as the need for more comprehensive coverage of broad ESG topics. Despite this, they appreciated the opportunity to learn about ESG, especially given the lack of available materials on the subject. In Slovenia, the course received praise for its preparation and quality content, with suggestions for enhancements such as including Life Cycle Assessment (LCA) analyses and providing practical examples. Feedback from Spain was generally positive, emphasizing the course's comprehensive and practical approach to sustainable management. In Romania, participants appreciated the course structure but criticized the online platform's functionality. Suggestions across all evaluations included the need for more practical examples, improvements in platform usability, and offering focused courses on specific topics. Overall, while there were areas for improvement, participants expressed interest in completing the course and participating in future related events.

Common themes across all evaluations included the desire for more practical examples and improvements in online platform usability. Despite some critiques, the course was generally well-received, with participants expressing interest in completing it.

The collected feedback from participants during the pilot courses facilitated further refinement of the learning products developed under the project. Some changes have been made in the course content, too.

3.5. Experimental Online Training

The objectives of the online course were to do a final test of the SECuRe e-Learning, evaluate the learning activities, assess the learners’ progress, the quality and effectiveness of the course, and collect feedback to improve future learning activities and content.

A standard methodology for e-Learning course development was followed, conducted by all partners in their countries:

- Pre-course learning activity – two introductory videos were prepared and are available on the platform, explaining the participants what the course is about, how it is structured, how to navigate in the platform, and the requirements for completing it.

- Cycle of learning events – the course consists of a series of learning activities that are scheduled on a weekly basis. However, students are free to go through the LUs according to their pace and preferences. The learning activities include self-study as well as a range of individual and collaborative activities, such as readings, self-study of different types of content, simple learning resources (documents and presentations), video and audio content, interactive exercises and individual assignments. Each LU ends with a test – achieving more than 70 % of the answers right enables student to proceed to the next LU.

- Final assessment – the assessment consists of a set of questions (assessment tests). The pass rate for the course is 70 %, too. A certificate of the achievement is issued to a successful student.

- Evaluation survey – participants were asked to fill in the evaluation survey that provides course designers and facilitators with feedback from participants.

The course is structured in the 6 training modules, each with activities or games (crossword puzzles, true or false questions, pair games, ...) where each student can test and evaluate the acquisition of knowledge. At the end of the course, and to obtain the certificate, the student had to complete a questionnaire for each module and answer at least a minimum number of questions. Until July 31, 2024, 333 people registered on the platform, of which 98 have completed the course and 54 are still in completing it; the remaining 181 users have not started the course tests, yet.

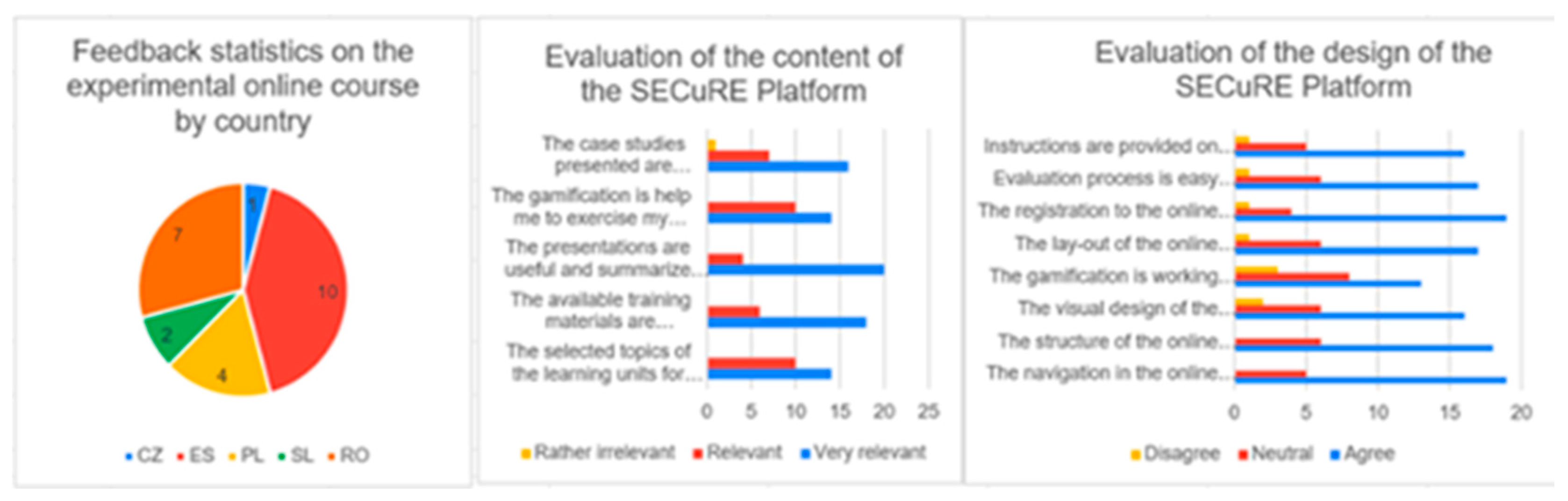

The overall success rate of those participants who have completed the course (certification quizzes) was 97,5 % with a range from 93,7 % for LU3 to 99,8 % for LU6. Using an online questionnaire, the collected feedback from 36 graduates indicates that the overall evaluation of the course is very positive – 100 % of responding participants would recommend the course and rated the course as a very good one. Figure 2 shows the statistics of the feedback questionnaires, including the breakdown by country of origin of the participants and the evaluation of the platform in terms of content and design.

The 36 evaluators were mainly environmental or sustainability consultants (41.7 %), professionals from public or private company (25.0 %), managers (8.3 %), and professors or VET teachers (5.6 %). The quality of the course was rated as very good by 33 out of 36 evaluators, as good by three, and as fair by one of them. As the most relevant the LU 6, Sustainability reporting (25/36) and the LU 3, Environmental dimension (24/36) were evaluated, followed by LU 5, Corporate governance dimension (20/36) and LU 4, Social dimension (18/36). The text together with general introduction embraces 357 pages; its presentation amounts to 189 PowerPoints.

The final course content and results of testing were presented and discussed at an international conference [25].

3.6. European Approach with Micro-Credentials for Lifelong Learning and Employability

Finally, the EU Recommendation to support the development, implementation and recognition of micro-credentials across institutions, businesses, sectors and borders was applied. Slovenian national programme on the Recovery and Resilience Plan (the RRP), financed by EU, was used to test the course and fill the gap between people formal education and training, and the needs of a fast-changing society and labour market [26]. The online course had a free access. It was not carried out in other partner countries.

In addition to the normal tests, described in section 3.5, the students had to prepare a seminar work dealing with sustainability report of a chosen company. The choice of the company was agreed between the student and the teacher. It included a comparison between the topics and key performance indicators of the company’s sustainability report and the suggestions presented in the LUs of the SECuRe course. The students prepared an outline of the suggested work, presented its draft in class, discussed it with the teacher and colleagues, and wrote the seminar report. Beside the PowerPoint presentation and seminar work, they had to prepare a written report on the homework duties required in the SECuRe LUs.

The participants have three possible choices during the course: a) they can just acknowledge themselves with the contents, b) they can study the content, make the tests and receive a Certificate of completion, or c) they make the tests and the homework, and deliver a seminar work to obtain a Professional certificate with micro credentials from the University of Maribor. The course started with 56 participants, but they gradually decreased during the five meetings to 40. At the application, 37 of them expressed a wish to make the tests and 18 of them planned to obtain the certificate with micro credentials. In fact, 14 participants finished the tests, 9 of them fulfilled the requirement for the certificate and received micro credentials.

4. Discussion

The project SECuRe started in May 2022 and finished (after two months of prolongation) at the end of June 2024. The period was well matched with the EU Commission which has published the CSRD in December 2022 [27]. It coincided well with the adoption of the ESRS in July 2023, and their publication in a consolidated version in December 2023 [28]. In May 2024 EFRAG published guidance on interoperability of ESRS and IFRS (the International Sustainability Standards Board) for companies that want to comply with both standards [29]. According to our research most European companies are using GRI framework at present; a cooperation between EFRAG and GRI exists, and a high degree of interoperability has been achieved between the ESRS and the widely used GRI Standards [30]. In August 2024, a draft of frequently asked questions on the implementation of the EU CSRD has also been published by the European Commission [31]. These coincidences helped the team to prepare a well-structured and updated course, and attractive LUs. Each LU is presented at the SECuRe portal in text (350 pages for the six LUs) and in the PowerPoint presentations. The course with gaming and the quizzes with training evaluations are available at the SECuRe platform for free.

Interest for the course was very high. This agrees with the growth of voluntary GRI Sustainability Reporting: starting with 11 reports in 1999, reaching 2 638 ones in 2010, 4,412 in 2015 and 9 980 in 2021 [32]. In 2022, 96 % of the G250 companies (world’s largest 250 companies by revenue), and 79 % of N100 companies (a worldwide sample of 4 900 companies comprising the top 100 companies by revenue in each of the 49 countries) reported their sustainability data – a huge increase from 1999, when 35 % of G250 and just 24 % of N100 companies reported them [33].

The SECuRe project ended, and partners do not have money to maintain the e-learning platform, update the course content and the KR. The team will propose another project (Erasmus+, RRP, national calls) or start a training business and apply for venture capital or crowdfunding.

5. Conclusions and Suggestions for Further Research

Corporations with their shareholders and companies with their owners are introducing and increasing sustainability approach in their everyday life. They have started it by using ISO standards: ISO 9000 series on Quality Management Principles, ISO 14000 on Environmental management systems (EMS), ISO 26000 on Social responsibility, ISO 51000 on Energy management system, and ISO 45001 builds on the success of earlier international standards in this area such as OHSAS 18000 (Occupational Health and Safety Assessment Series). The timeline corresponds to the timeline of these ISO standards appearance [34].

Later, they started with ESG reporting. Finally, SRSs (sustainability reporting standards) evolved and became mandatory in some parts of the World, e.g., ESRSs in EU with 50 000+ companies, CDP (formerly the Carbon Disclosure Project) on global environmental disclosure used by more than 23 000 companies, GRI with 10 000 ones, and ISSB (International Sustainability Standards Board) that started to create IFRS Sustainability Disclosure Standards in 2023. To use any standards efficiently, employees need modern courses and good teachers.

This research contributes to the education and training of professionals in sustainability practices, preparing them to navigate complex challenges within corporates’ sustainability settings. By enhancing understanding and skills related to sustainability reporting, the project empowers individuals to drive meaningful transformations towards more responsible business practices. The SECuRe project responds to evolving job market demands by equipping professionals with essential skills in sustainability reporting. This has economic implications as companies strive to comply with sustainability directives and standards. Enhanced reporting capabilities can lead to improved corporate governance, risk management, and strategic decision-making. Furthermore, the project aligns with broader economic initiatives such as the European Green Deal, which aims to transition towards a more sustainable and resource-efficient economy. Sustainable practices address environmental challenges such as climate change, resource depletion, and biodiversity loss. By educating professionals on sustainability management and reporting, the SECuRe project contributes to mitigating environmental impacts associated with corporate activities. Increased awareness and adoption of sustainability practices can drive reductions in carbon emissions, resource consumption, and overall environmental footprint.

By aligning with the CSRD and the ESRSs, the SECuRe project ensured relevance and compliance with regulatory frameworks. This integration added significant value by preparing professionals to navigate and implement these directives effectively within corporate contexts.

While the project made significant strides in sustainability education and reporting, several limitations and avenues for further research existed. Participants highlighted the need for broader coverage of sustainability aspects beyond reporting, such as sustainable development leadership and regenerative economy concepts. Feedback suggested a preference for including more practical examples and case studies into the course. Further research could focus on developing additional practical resources and real-world applications to enhance effectiveness of the course. Challenges related to marketing and awareness were noted. Further research could explore strategies for increasing the program's visibility and attracting participation from a broader audience, including SMEs and educational institutions.

The project has successfully developed a comprehensive vocational course on sustainability reporting aligned with EU directives and standards. Utilising the ADDIE methodology and innovative e-learning platform, the project is equipping professionals with the necessary skills and knowledge to navigate sustainability challenges within corporate settings. The research findings indicate strong positive feedback and effectiveness, with suggestions for further development to broaden course content and enhance market awareness. The SECuRe project represents a significant contribution to sustainability education and has the potential to drive meaningful change towards more sustainable and responsible business practices.

CSRD is considering companies, only. What about other fields of human endeavour? Political units and associations (local communities, cities, regions, states), social organizations (covering health care, education and learning, social care, army, police, courts, etc.), non-governmental organizations, all social units with more than 250 employees or members? Universities, hospitals shall take a lead. United Nations, USA and EU with state governments shall prepare directives for their sustainability reporting.

Author Contributions

Conceptualization, T.S. and P.G.; methodology, T.S.; software, T.S.; validation, A.S., I.Z. and P.R.; formal analysis, A.S. and H.L.; investigation, P.G., H.L., A.S., I.Z. and P.R.; resources, I.Z.; data curation, T.S.; writing—original draft preparation, P.G.; writing—review and editing, P.G.; visualization, V.H.; supervision, P.G.; project administration, M.R.; funding acquisition, T.S. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by EU’s ERASMUS+ funding program, grant number 2021-2-PLO1-KA220-VET-000050377, Smart Education for Corporate Sustainability Reporting.

Acknowledgments

the authors acknowledge the support given by Eugenia Atin (Prospektiker), Jarmila Bilikova, Vendula Hemzalová and Jiří Jeřábek (Enviros), Vesna Dragojlović (University of Maribor), and Aneta Lochno (Atmoterm) .

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Baumgartner, R.J. , Rauter, R. Strategic perspectives of corporate sustainability management to develop a sustainable organization. J. Clean. Prod. 2017, 140, 81–92. [Google Scholar] [CrossRef]

- Opferkuch, K. , Caeiro, S., Salomone, R., Ramos, T. B. Circular economy disclosure in corporate sustainability reports: The case of European companies in sustainability rankings. Sustain. Prod. and Consump. 2022, 32, 436–456. [Google Scholar]

- Kücükgül, E. , Cerin, P., Liu, Y. Enhancing the value of corporate sustainability: An approach for aligning multiple SDGs guides on reporting. J. Clean. Prod., 2022, 333, 130005. [Google Scholar] [CrossRef]

- Ioannou, I. , Serafeim, G. The Consequences of Mandatory Corporate Sustainability Reporting. Harvard Business School Research Working Paper, 2017, No. 11–100.

- Madaleno, M. , Vieira, E. Corporate performance and sustainability: Evidence from listed firms in Portugal and Spain. Energy Reports 2020, 6, 141–147. [Google Scholar] [CrossRef]

- Bovea, M.D. , Belis, V.P., Adell, L.T., Forés, V.I. How do organizations graphically communicate their sustainability? An exploratory analysis based on corporate reports. Sustain. Prod. and Consump. 2021, 28, 300–314. [Google Scholar]

- Shaer, H.A. , Hussainey, K. Sustainability reporting beyond the business case and its impact on sustainability performance: UK evidence. J. Environ. Manage 2022, 311, 114883. [Google Scholar] [CrossRef] [PubMed]

- Erlandsson, J. , Bergmark, P., Höjer, M. Establishing the planetary boundaries framework in the sustainability reporting of ICT companies – A proposal for proxy indicators. J. Environ. Manage 2023, 311, 2023329. [Google Scholar]

- Walińska, E. , Dobroszek, J. The Functional Controller for Sustainable and Value Chain Management: Fashion or Need? A Sample of Job Advertisements in the COVID-19 Period. Sustainability 2021, 13, 7139. [Google Scholar] [CrossRef]

- European Commission, The European Green Deal (EGD), Communication from the commission, COM(2019) 640 final. Available online: https://eur-lex.europa.eu/le.gal-content/EN/TXT/?uri=CELEX%3A52019DC0640 (accessed on 12 July 2024.

- United Nations, Transforming our world: the 2030 Agenda for Sustainable Development. https://sdgs.un.org/2030agenda. (accessed on 12 July 2024).

- European Parliament, 2021. Available online: https://www.europarl.europa.eu/RegData/etudes/BRIE/2021/654213/EPRS_BRI (accessed on day month year).

- European Commission, Corporate sustainability reporting. https://finance.ec.europa.eu/capital-markets-union-and-financial-markets/company-reporting-and-auditing/company-reporting/corporate-sustainability-reporting_en. (accessed on 9 August 2024).

- Posthuma, J., IDRN. Transparency in Action: The Corporate Sustainability Reporting Directive explained. Available online: https://idrn.eu/transparency-in-action-the-corporate-sustainability-reporting-directive-explained/ (accessed on 12 July 2024).

- European Commission, Guidelines on non-financial reporting. OJEU 2017, C 215, 1–20.

- European Commission, Guidelines on non-financial reporting: Supplement on reporting climate-related information. OJEU 2019, C 209, 1–30.

- EFRAG, ESRS workstreams. https://www.efrag.org/en/sustainability-reporting/esrs-workstreams. (accessed on 9 August 2024).

- GRI – Global Reporting Initiative, GRI Academy. (n.d.). https://www.globalreporting.org/reporting-support/gri-academy/. (accessed on 9 August 2024).

- UN DESA (United Nations, Department of Economic and Social Affairs). SDG Actions Platform. Available online: https://sdgs.un.org/partnerships (accessed on 12 July 2024).

- Educational Technology, ADDIE Model: Instructional Design. https://educationaltechnology.net/the-addie-model-instructional-design/. (accessed on 9 August 2024).

- QuestionPro, Usability Lab: What Is It, When, and How It Is Used. https://www.questionpro.com/blog/usability-lab/#How_to_Set_Up_a_Usability_Lab. (accessed on 9 August 2024).

- TCFD, Task Force on Climate-related Financial Disclosures. https://www.fsb-tcfd.org/. (accessed on 18 July 2024).

- ECVET (2009). Cedefop, European credit system for vocational education and training: https://www.cedefop.europa.eu/en/projects/european-credit-system-vocational-education-and-training-ecvet. (accessed on 21 July 2024).

- Glavič, P.; Levičnik, H.; Szilagyi, A.; Schönfelder, T.; Bilikova, J.; Ruzicka, P.; Atin, E.; Zugasti, I. Education for Corporate Sustainability Reporting, Proceedings of the 18th IRDO International Conference Innovative Sustainable and Socially Responsible Society 2023: Empowering Society, Environment and Economy for Sustainability, Slovenia, 8–9 June 2023, Conference Proceedings, 8 pp., ISBN 978-961-7141-03-0 (HTML).

- Glavič, P.; Levičnik, H.; Szilagyi, A.; Hajna, V.; Zugasti, I. Smart Course for Corporate Sustainability Reporting, Proceedings of the 19th IRDO International Conference Innovative Sustainable and Socially Responsible Society 2024: ESG (environmental, social, governance) aspects in theory and practice, Slovenia, 12–13 June 2024, Conference Proceedings, 8 pp., ISBN 978-961-7141-10-8 (HTML).

- EU Council Recommendation on a European approach to micro-credentials for lifelong learning and employability, OJEU 2022, C 243, 10.

- European parliament and the Council of the EU, Corporate Sustainability Reporting Directive (CSRD), OJEU 2022, L 322, 15.

- European Commission, European Sustainability Reporting Standards (ESRS), OJEU 2023, L 2772.

- EFRAG, IFRS. ESRS–ISSB Standards, Interoperability Guidance. https://www.efrag.org/sites/default/files/sites/webpublishing/SiteAssets/ESRS-ISSB%20Standards%20Interoperability%20Guidance.pdf. (accessed on 2 November 2024).

- Global Reporting Initiative, GRI and sustainability reporting in the EU – Frequently asked questions by GRI reporters and information users. https://www.globalreporting.org/media/d4faazel/gri-and-the-esrs-qa-final.pdf. (accessed on 2 November 2024).

- European Commission, Directorate-General for Financial Stability, Financial Services and Capital Markets Union, Frequently asked questions (FAQs) on the implementation of EU CSRD. https://finance.ec.europa.eu/document/download/c4e40e92-8633-4bda-97cf-0af13e70bc3f_en?filename=240807-faqs-corporate-sustainability-reporting_en.pdf. (accessed on 2 November 2024).

- Brightest, The Top 7 Sustainability Reporting Standards in 2024. https://www.brightest.io/sustainability-reporting-standards#csrd. (accessed on 3 November 2024).

- McCalla-Leacy, J.; Shulman, J.; Threlfall, R. (KPMG), Big shifts, small steps, Survey of Sustainability Reporting 2022. https://assets.kpmg.com/content/dam/kpmg/se/pdf/komm/2022/Global-Survey-of-Sustainability-Reporting-2022.pdf. (accessed on 3 November 2024).

- Lancien, I. (Nexio Projects), The ISO Standards for Sustainability. https://blog.nexioprojects.com/the-iso-standards-for-sustainability. (accessed on 5 November 2024).

Figure 1.

The Phased Implementation of the EU CSRD Regulation based on previous year's financial data [14].

Figure 1.

The Phased Implementation of the EU CSRD Regulation based on previous year's financial data [14].

Figure 2.

Evaluation statistics of the Experimental online training.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.