Submitted:

18 December 2023

Posted:

19 December 2023

You are already at the latest version

Preprints on COVID-19 and SARS-CoV-2

Abstract

The study investigated the changes that occurred in the Mexican power sector pre-, during, and post-COVID-19 pandemic and its repercussions on energy sustainability goals. The study is based on the variability of the installed capacity, consumption, generation, and demand of the National Electric System (SEN), covering the period from 2017 to 2021. The data were collected from the Development of the National Electric System (PRODESEN), the Ministry of Energy, the National Energy Balance, and the government's official website. The results indicated that in-stalled capacity and generation increased by 22.83% and 27.86%, respectively, despite the pan-demic. This growth was attributed to clean energy, mainly photovoltaic solar and wind sources. Another finding is that the gross domestic product (GDP), consumption, and demand were seri-ously affected by COVID-19. They had a fall of 8.2%, 2.2%, and 4.4%, respectively, which trans-lates into a significant economic lag and a slowdown in energy self-sufficiency and the Mexican Energy Transition (TEM). Moreover, the objective of generating 35% and 40% of electrical ener-gy through clean energy will be achieved by 2031 and 2035, instead of 2021 and 2035, respec-tively.

Keywords:

Consumption

; demand

; installed capacity

; SEN

1. Introduction

In March 2020, the WHO declared the SARS-COVID-2 virus outbreak, known as COVID-19, which had a profound impact on the lifestyles of each country [1]. Since its appearance, each country has taken a wide range of measures to stop its spread, some of which include social distancing, strict confinement, and the cessation of non-essential economic activities, among others [2,5]. As a consequence, there were serious repercussions not only on health but also on economic indicators, energy use, and CO2 emissions. From an economic point of view, the crisis caused by the pandemic produced a drop in the GDP [6,7,8], the impact on trade levels [9,10,11]; the loss of millions of jobs [12,13]; the increases in the levels of poverty and inequality in various scopes [14,15]. From the energy point of view, there was an imbalance in prices, investments, and patterns of generation, consumption, and demand for energy, mainly in oil, gas, and electricity [16,17,18]. Finally, from an environmental point of view, CO2 emissions were reduced, but climate targets were delayed in most countries [19,20].

The electricity sector, being one of the fundamental pillars of human activities, has been the focus of attention due to its rapid changes in generation, consumption, and demand as a result of the pandemic. Early attempts to track the evolution of electricity changes reported that electricity consumption decreased by 4.5% in 2020 and increased by 5% in 2021, in the context of the global pandemic. Countries like China presented an increase in electricity consumption of 2.2% and 5.2% in 2020 and 2021, respectively. However, India, the United States, Russia, and the European Union reduced electricity consumption by 5.6%, 8.6%, 4%, and 6.8% in 2020, and in 2021, they increased electricity consumption by 4.7%, 4.7% 9%, and 4.5%, respectively [20,21]. Electricity consumption also increased in many regions, except for the Middle East (-0.4%) and the Pacific (-2.5%). In relation to electricity demand, the International Energy Agency reported that Global electricity demand fell by around 1% in 2020, decreasing more markedly in the first months of 2020. Eliminating climatic variations, in 2020, China's demand fell more than 10% in February. In Germany, France, and the United Kingdom it fell by more than 15% and, in Spain and Italy, even more than 25%. Similarly, India presented a reduction of 20% in electricity demand during March and April. In Japan and Korea, where COVID-19 cases were lower than in Europe, demand fell by around 8% in May [22,23,24].

In the literature, there is a limited amount of research that addresses the effects of COVID-19 in the energy sector, especially in the electricity sector. However, these studies report electricity demand, electricity consumption patterns in the most affected countries such as China, Italy, USA, and the impact these had on gross domestic product pre- and during COVID-19 [25,30]. Therefore, the objective of this study is to analyse the impact of the generation, consumption, and demand of electric energy pre-, during, and after the COVID-19 pandemic in Mexico. The novelty of this study revolves around the variations of electrical energy from 2017-2021 in conventional and clean energies, as well as the different regions of the Mexican SEN. It also includes the discussion of implications for energy sustainability goals.

The remainder of the paper is organised as follows. In Section 2, the methods used to estimate the impact of installed capacity, generation, consumption, and demand are presented. In section 4, we showed a general description of the Mexican SEN in detail. Section 5 explains the main results of the statistical analysis in terms of installed capacity, generation, consumption, and demand for electrical energy. Finally, in sections 6 and 7 discussions of future directions and conclusions are provided, respectively.

2. Methodology

The main objective is to assess the changes of the COVID-19 pandemic in the electricity sector. For this study, we analysed data collected from the annual publication of the PRODESEN, which is published by the Secretary of Energy SENER, along with other databases such as the National Energy Balance, data belonging to CENACE, and the official government website. The analysis was based on the statistical variability from 2017 to 2021 in installed capacity, generation, consumption, and demand during the post-COVID period and then compared with the period before and after the pandemic. This research uses the conventional and clean sources in the analysis of installed capacity and generation, and nine control regions (Central, Eastern, Western, Northwest, North, Northeast, Baja California, Peninsular, Baja California Sur, and Mulegé System) in consumption and demand analysis. For a better readability, Table 1 lists the abbreviations used in this section.

3. Panorama of COVID-19 in Mexico

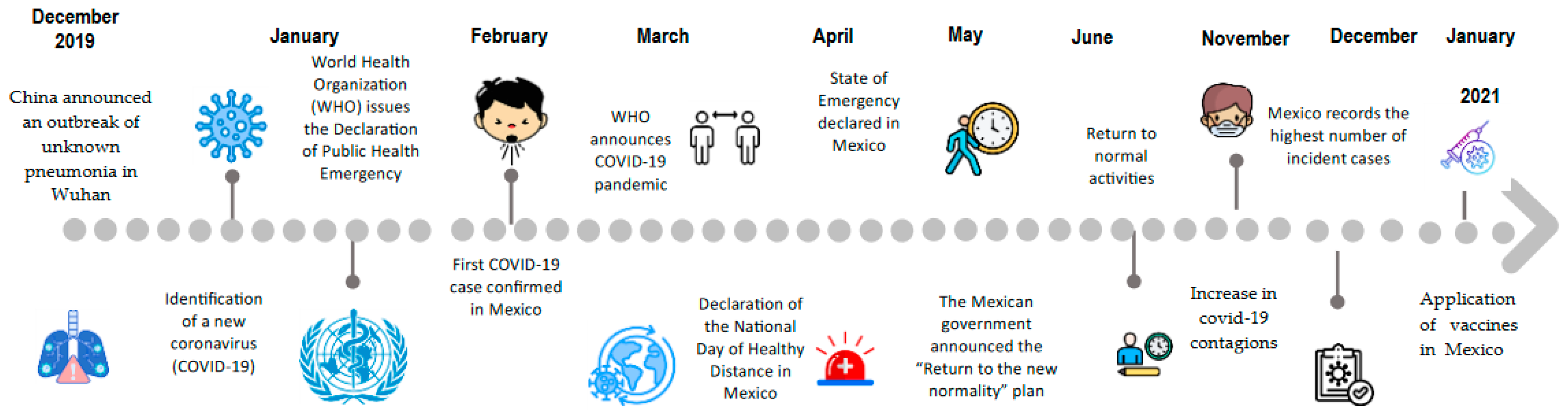

The first case of SARS-CoV2 was reported on February 27, 2020, in Mexico [31]. At the time, the virus had already been reported as a global threat, however, it was expected to take adequate control of the situation. Due to the levels of propagation and its severity, the WHO defined COVID-19 as a pandemic. The evolution of the epidemic in Mexico continued. Given the alert of a massive contagion, the “Sana Distancia” program was established in the country on March 23, which would help reduce contagion [32,33]. With this program, classes were suspended in schools nationwide and non-essential activities were suspended, as well as concerts and other events that could generate a crowd of people; except those related to security, health, energy, and cleaning.

The number of infections began to grow exponentially faster than expected, so a health emergency was declared in Mexico on April 1 [34]. This led to the establishment of additional measures like remaining at home to the general population, especially those over 60 years of age and people with a diagnosis of high blood pressure, diabetes, heart disease or pulmonary disease, induced or acquired immunosuppression, to women who are pregnant or postpartum immediately. On May 13, the Mexican government announced the “Return to the new normality” plan, and on June 1 the return of essential activities began. In this phase, Mexico begins its National Vaccination Day, with the arrival of the first batch of vaccines developed by Pfizer-BioNTech. It began immunising front-line medical personnel caring for COVID-19 patients [35,36]. Figure 1 shows a timeline of the COVID-19 in Mexico.

4. Mexican National Electric System (SEN)

The SEN is made up of transmission lines, general distribution networks, power plant equipment, and installation in Mexico. It is divided into nine control regions and an isolated electrical system [37]: 1) Central, 2) Eastern, 3) Western, 4) Northwest, 5) North, 6) Northeast, 7) Baja California, 8) Peninsular, 9) Baja California Sur and 10) Mulegé System, as shown in Figure 2. All these regions share resources and capacity reserves responding to the demands and operating situations of electricity. Most of these regions are interconnected, forming the SIN. Baja California is the only region that operates with the Western Interconnection of the United States overseen by WECC.

The SEN is controlled by CFE, and its technical operator is CENACE [38,39]. One of the functions of the CENACE is to monitor in real-time the generation, demand, and consumption of energy that is registered in the electrical system. Another function is to develop strategies, goals, and objectives for planning, retirement, expansion, distribution, and modernisation of the SEN through PRODESEN [40,41].

5. Results

5.1. Installed Capacity

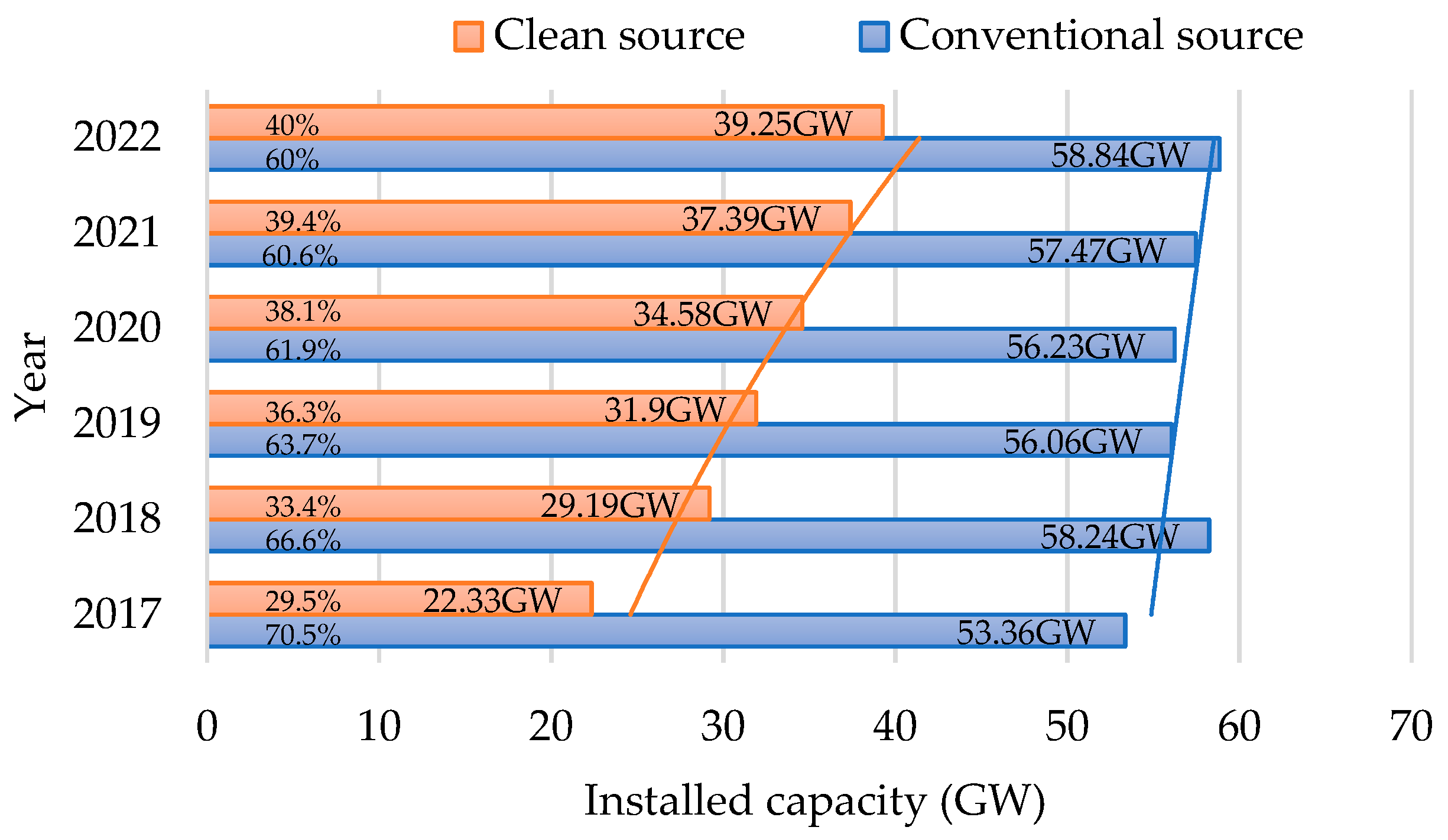

In the last five years, Mexico has increased its total installed capacity, from 75.7 GW to 98.1 GW, which is equivalent to 22.83% [42]. To achieve this, the government established short and medium-term goals to generate electricity from clean energy and promoted Structural Reforms, which allowed the modernisation of the electricity and oil industry [43]. In particular, the goals are focused on the participation of clean energies and it will reach 25%, 30%, and 35% in 2018, 2021, and 2024, respectively [44]. As a result, the installed capacity of clean sources increased from 22.33 GW to 29.25 GW (23.66%), from 2017 to 2021, while conventional sources have increased their capacity at a slow rate, going from 53.36 GW to 58.84 GW (9.31%), as shown in Figure 3.

In 2018, the installed capacity was 87.44 GW, presenting a strong growth of 13% compared to 2017 (75.7 GW), as shown in Table 2. In this year, the biggest change was seen in the clean sources, which presented an increase in the solar photovoltaic source and wind with 95.3% (0.21 GW to 4.43 GW), and 36.41% (from 4.19 GW to 6.59 GW), respectively (Figure 3). With less growth was reported hydroelectric and geothermal sources. Part of the growth was due to the Energy Transition Law and the three electricity auctions held to date. This has allowed 39 solar plants to operate in 11 states, including the largest plant in Latin America and the second largest in the world, located in Viesca, Coahuila [45,46]. In relation to the conventional sources, the major changes were seen in the combined cycle, which increased from 28.08 GW to 33.72 GW, corresponding to 16.73%, followed by coal-fired sources from 5.38 GW to 5.51 GW (2.4%), and internal combustion with 1.8%. While the thermoelectric source presented a reduction of 6.98%.

From 2018 to 2019, installed capacity kept increasing moderately (0.6%) implying a less rich growth than in 2018 due to the pandemic. According to PRODESEN 2018-2032 [47], conventional energy decreased by 3.7% and clean sources increased by 8.5% of the installed capacity. The major reduction came from thermoelectric sources by 12% due to the effects of the COVID-19 pandemic and the cancellation of four new power plant projects [48]. In relation to clean sources, the investment of installed capacity in photovoltaic sources passed wind power, to become the sixth-largest source of energy based on its capacity, after the combined cycle (34.28 GW), hydroelectric (12.67 GW), thermoelectric (8.23GW), wind (8.13 GW) and turbogas (5.75 GW). Photovoltaic energy had a growth of 21.31%, reaching 5.63 GW, while wind technology had an increase of 18.9% in installed capacity.

In 2020, the installed capacity presented an increment of 3.14% despite the contingency. The increase in installed capacity was mainly on clean sources by 7.7%, while conventional energy had a weak growth of 0.3%. In the case of conventional sources, thermoelectric energy had a reduction from 8.23 GW to 7.48 GW, representing 9.1%. This negative impact could be attributed to the three transient failures that occurred in the 400 kV network that caused the simultaneous disconnection of the 400 kV double circuit and the interruption of the electricity supply in Yucatan [49]. As a result, internal combustion and combined cycle technologies compensated for the supply of electrical energy, going from 1.66 GW to 1.77 GW (6.2%) and from 34.28 GW to 35.15 GW (2.4%), respectively. In the case of clean sources, photovoltaic sources added an increase in their installed capacity of 25.4% compared to 2019, followed by investments in wind resources with 8.2% and the bioenergy source with 3.8%.

In the post-pandemic (2020-2022), the installed capacity raised to 94.87 GW, which represented an increase of 4.27% with respect to 2020. According to Figure 3, both conventional and clean sources increased 2.2% and 7.5% from 2020-2021, and 2.3% and 4.7% from 2021-2022, respectively. During 2020 and 2021, the combined cycle increased its capacity by 4.7%. However, the thermoelectric industry continued to fall from 7.48 GW to 7.16 GW (-4.3%). Also, turbogas and internal combustion showed a decrease in installed capacity, going from 5.75 GW to 5.66 GW (-1.6%) for turbogas, and from 1.77 GW to 1.69 GW (-4.5%) for internal combustion. The wind, bioenergy, and photovoltaic industries had a slight increase in the installed capacity of 21.1%, 3.8%, and 2.6%, respectively. In 2022, the installed capacity of clean energy plants such as photovoltaic, wind, and bioenergy continued to grow by 3.7%, 9.6%, and 18.3%, respectively. Also, it was reported an increase in installed capacity for the combined cycle at 9.2% and internal combustion at 2.9%.

5.2. Generation

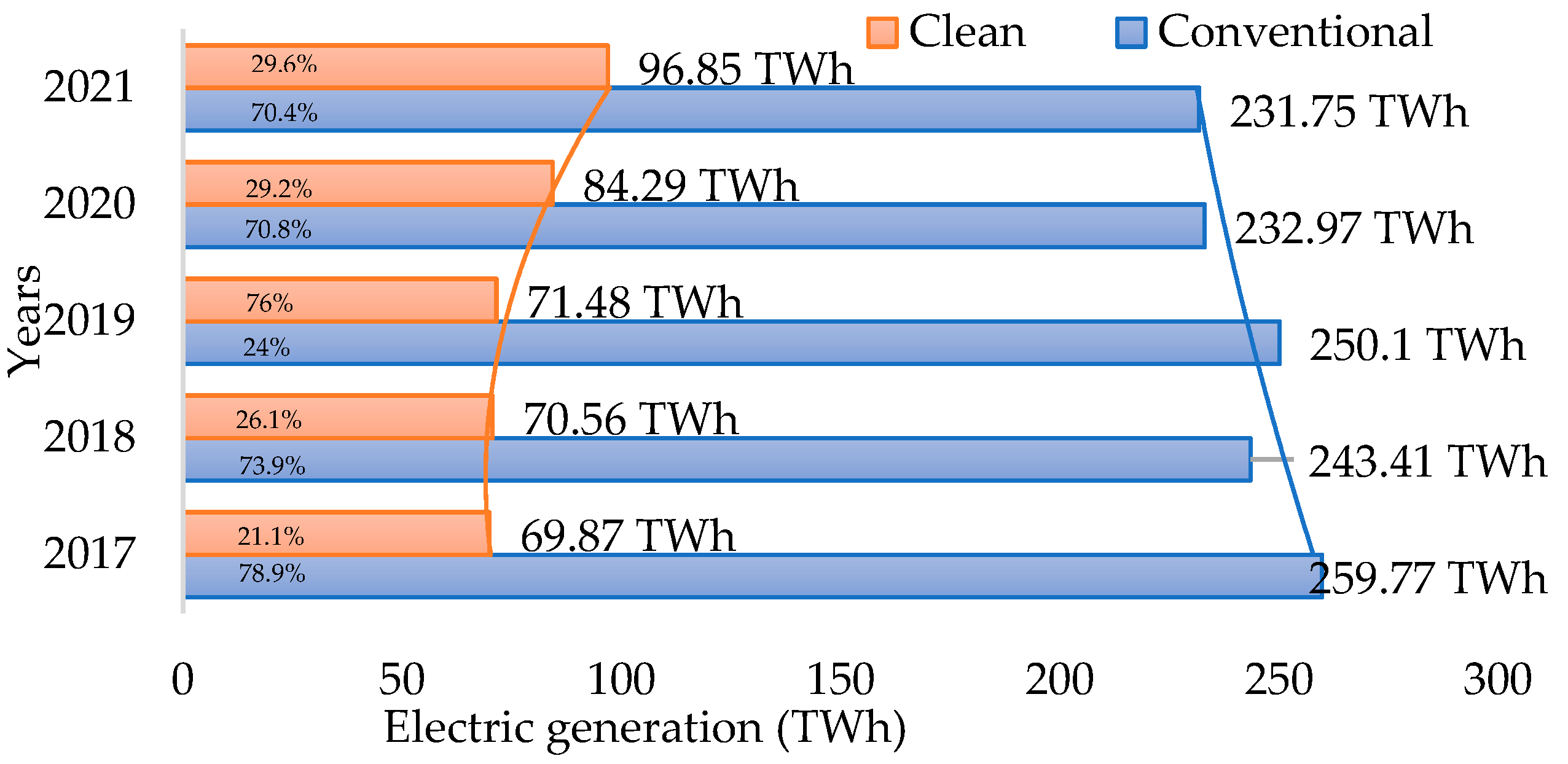

According to CENACE data, in the last six years, the electricity generation in Mexico grew 4.3%, going from 319.364 TWh in 2016 to 333.8 TWh in 2022 [50]. This growth is almost entirely attributed to the increase in electricity generation through clean technologies. As shown in Figure 4, between 2017 and 2021, the generation with clean sources increased 27.86%, from 69.87 TWh to 96.85 TWh, while power generated from fossil sources grew 20.9592%, going from 259.77 TWh to 328.59 TWh, due to pandemic.

During the pre-pandemic period (2017-2018), total power generation was 313.16 TWh in 2018, with a decrease of 4.6% compared to 2017 (329.16 TWh). The largest decreases in electricity generation were around conventional sources, which presented a reduction of 1.6% (from 259.77 TWh to 243.41 TWh). The energy generated in power plants operated by internal combustion registered the greatest drop, going from 4.01 TWh to 2.59 TWh (35.41%). In the same sense, turbogas sources presented a reduction of 26% (from 12.85 TWh to 9.51 TWh), followed by coal-fired sources with 10.47% (from 30.55 TWh to 27.35 TWh). Finally, the energy generated in thermal power plants and combined cycle fell 8.04% and 0.83%, respectively, as shown in Table 3. The decrease in generation from conventional resources is mainly attributed to the increasing availability of cleaner, more efficient, and cheaper plants [45].

On the contrary, the clean energies grew 1.6%, going from 69.87 TWh to 70.56 TWh. Specifically, clean sources (solar photovoltaic and wind) presented the highest growth rates in 2018. Between 2017 and 2018, the solar photovoltaic source increased 89.29%, going from 334 GWh to 3.211 TWh, while wind sources grew 17.09%, going from 10.620 TWh to 12.435 TWh. The increase in these two technologies responds to the development of the MEM, and, fundamentally, to the long-term electricity auctions held between 2015 and 2017, [51]. Similarly, bioenergy sources increased electricity generation by 5.58%.

During the COVID-19 pandemic (2019-2020), electricity generation achieved 321.58 TWh, increasing 2.36% with respect to 2018. The clean energies with the highest growth rates were photovoltaic and wind energy with 67.76% and 25.65%, respectively. Opposite, hydroelectric plants had a significant reduction of 26.77% from 32.23 TWh to 23.6 TWh, due to water scarcity and increased droughts in the country in this year [56]. In addition to this, nucleoelectric and bioenergy sources decreased by 15.58% and 6.17%, respectively. In the case of conventional sources, internal combustion increased by 18.78%, from 2.58 TWh to 3.18 TWh. Similarly, turbogas and the combined cycle had an increment of 12.8% and 6.6%, respectively. While coal-fired sources had a reduction of 20.97%, going from 27.35 TWh to 21.61TWh.

In addition, it can be noted generation fell 1.3% from 321.58 TWh to 317.27 TWh with respect to 2019, (Figure 4). According to the PRODESEN report [47], clean resources were the main source of electricity production in Mexico, generating 15.19% more energy than in 2019, while conventional energy had a reduction of 6.85%. Regarding conventional energy, the electric generation with combined cycle slightly increased by 5.5%, going from 175.51 TWh to 185.64 TWh, compensating for decreases in other energy sources. The energy generated in conventional thermal power and coal-fired plants registered the greatest decrease (about 42%). Turbogas also decreased from 10.90 TWh to 8.66 TWh (20.58%). internal combustion sources had a reduction of 10.86%, going from 3.19 TWh to 2.84 TWh. Despite the health emergency caused by the coronavirus, clean sources grew 15.2%, from 71.48 TWh to 84.29 TWh during this period. In special, the solar photovoltaic source registered an increase from 9.96 TWh to 15.84 TWh, corresponding to 37.1%. Wind and bioenergy sources increased about 15%, from 16.73 TWh to 19.7 TWh, and 1.87 TWh to 2.2 TWh, respectively. Similarly, hydroelectric sources increased by 11.99%, from 23.6 TWh to 26.82 TWh (Table 3).

After a 1.3% drop due to the COVID-19 pandemic in 2020, power generation rebounded by 3.44% in 2021, as shown in Figure 4. Specifically, hydraulic and solar photovoltaic sources presented the highest growth rates during the period analysed. Hydraulic sources grew 22.76%, going from 26.82TWh to 34.71 TWh, while photovoltaic energy grew 21.6%, going from 15.84 TWh to 20.19 TWh. Wind and nucleoelectric also increased by about 6.4%. However, bioenergy and geothermal sources fell 27.68% and 7.25%, going from 2.21 TWh to 1.59 TWh, and from 4.57 TWh to 4.24 TWh, respectively. On the other hand, conventional energy presented a slight reduction of 0.5%, from 232.97 TWh to 231.75 TWh. This decrease is mainly attributed to the coal-fired source, which has a reduction from 12.53 TWh to 8.7 TWh, equivalent to 30.6\%, and internal combustion from 2.84 TWh to 2.12 TWh (25.4%). Contrarily, turbogas sources increased by 22.3% from 8.67 TWh to 11.15 TWh.

5.3. Consumption

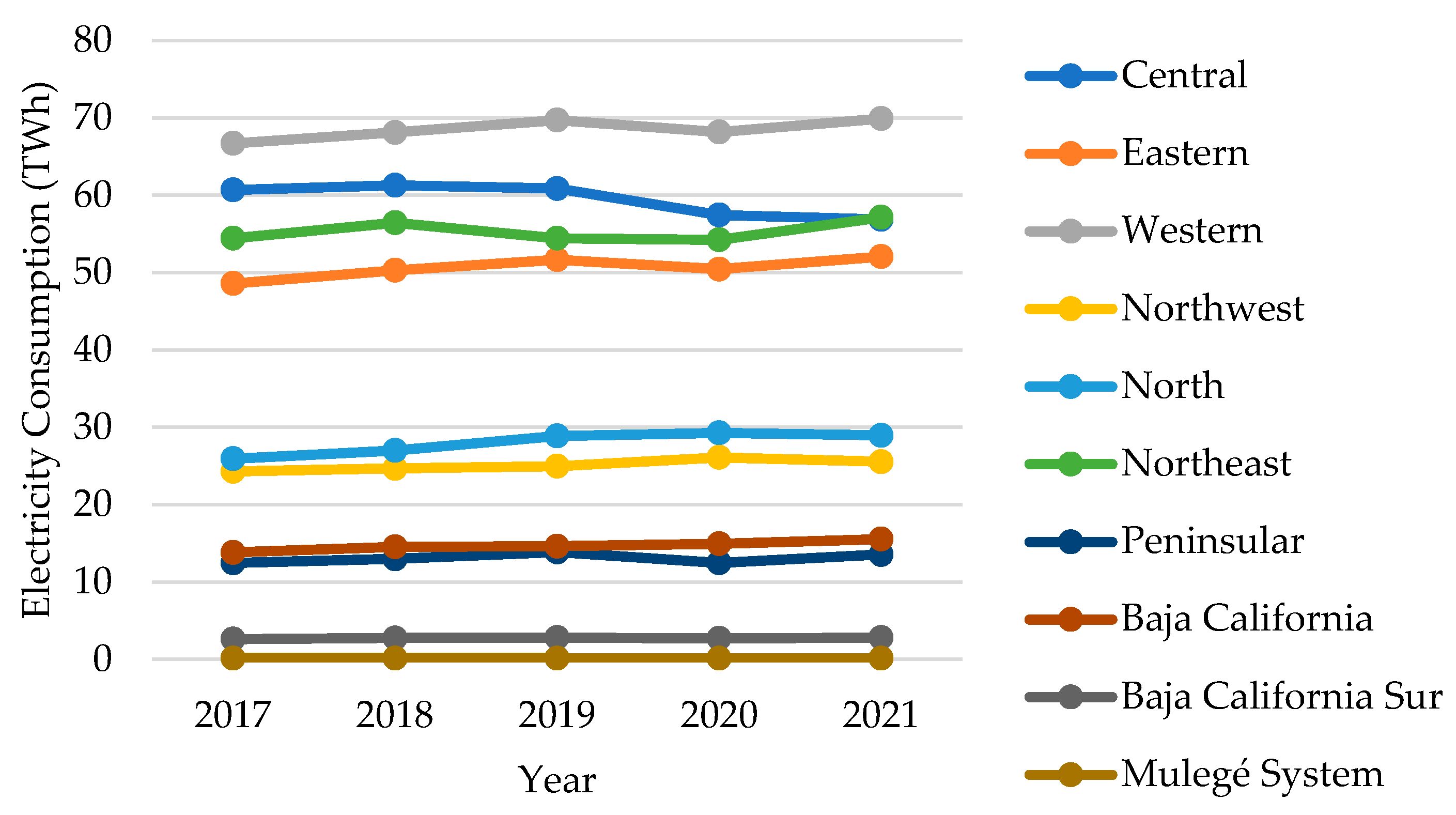

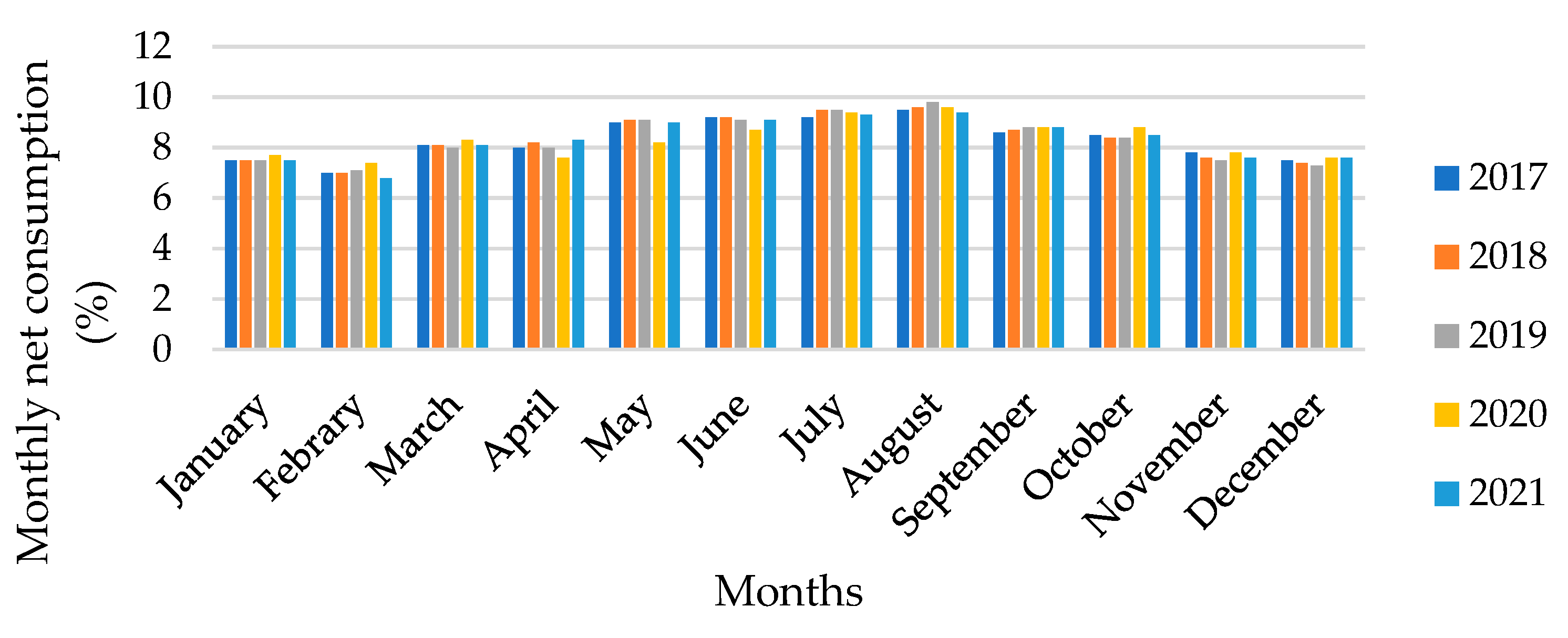

From 2017 to 2021, Mexico increased its total electricity consumption, from 309.73 TWh to 322.54 TWh, which is equivalent to 3.97% [52,53,54,55]. Figure 5 shows the evolution of the Annual Gross Consumption of Electricity by control area in the period 2017 to 2021, where it can be distinguished that the areas with the highest gross consumption of electric power in the country are the Western, Central, and Northeastern areas, while the regions with the lowest consumption are Baja California Sur, Peninsular and Baja California.

During the pre-pandemic period (2017-2018), the gross national consumption of the SEN registered an increase of 318.24 TWh, which meant a growth of 2.7% compared to the consumption of 2017 with 309.73 TWh, (Table 4). In general, all the regions showed moderate growth. The northern regions of the country (North, Northeast, and Northwest) grew 3.8%, 3.5%, and 1.6%, respectively, caused by high temperatures in the summer months. Eastern and Western regions had also a growth of 3.4% and 2.1%, and with less participation in electricity consumption was the Central region (1%). During the year in the months of May to October 54.5% of gross consumption was presented, while in the remaining months 45.5%.

In the COVID-19 pandemic (2019-2020), the national gross consumption of the SEN continued to rise to 324,927 TWh, which meant an increase of 2.1% compared to the consumption of 2018. Most of the regions showed growth in electricity consumption, except for the Central and Northeast regions. They had a fall of 0.72% and 5.6%, respectively. Opposite, the North and Peninsular regions registered an increase of about 6.4% in their electricity consumption. Eastern, Western, and Baja California Sur regions increased the national gross consumption between 2.1% and 2.7%. A slight growth in electricity generation was presented by Northeast (1.2%) and Baja California (0.5%). During the year in the months of May to October 54.6% of gross consumption was presented, while in the remaining months 45.4%.

In 2020, the national gross consumption was 315.97 TWh, which meant a decrease of 2.76% compared to the consumption of 2019. This decrease was caused by the health contingency caused by COVID-19, which caused the suspension of productive activities throughout the country. In this period, the Northwest region presented a positive growth rate of 4.6%, from 24.97 TWh to 26.1 TWh. Similarly, Mulegé, Baja California, and the North region increased electrical consumption by 2.6%, 2.2%, and 1.5%, despite the contingency. In Table 4, it is shown that the Peninsular regions reduced their energy consumption by 9.9%, followed by the Central (5.6%) and Northeast regions (5.5%). Similarly, Eastern and Western regions decreased their consumption by about 2.4%. As shown in Figure 6, in the first quarter of 2020 (from January to March), Mexico increased electricity consumption when the first case of COVID-19 was detected. After this first diagnosis, the number of patients increased exponentially. In response to this global outbreak, the Ministry of Health established the “Sana Distancia” program, with which sanitary and social distancing measures come into action to reduce contagion, Section 3. As a result, the electricity consumption was reduced from April to September. In the remaining months, energy consumption presented a slight rebound. This increase may be the result of greater use of energy in homes due to the decrease in temperature or the decision of some businesses to resume activities despite the pandemic.

In the post-pandemic period (2020-2021), the national consumption of the SEN amounted to 322.54 TWh, which means an increase of 3.5% compared to the consumption of 2020. This increase is a reflection of the rising recovery of the country's economy, after the ravages caused by the health contingency, which caused the suspension of some productive activities throughout the country. In this period, the Peninsular, Northeast, and Baja California and Baja California Sur were the zones that showed a higher recovery when presenting rates of 7.8%, 5.1%, 3.9%, and 3.9%, respectively. The Eastern zone showed moderate growth in the order of 3.1%, going from 50.44 TWh to 52.07 TWh. However, Northwest, North, and Central regions continued to decrease their consumption by 2.1%, 1.2%, and 1% respectively.

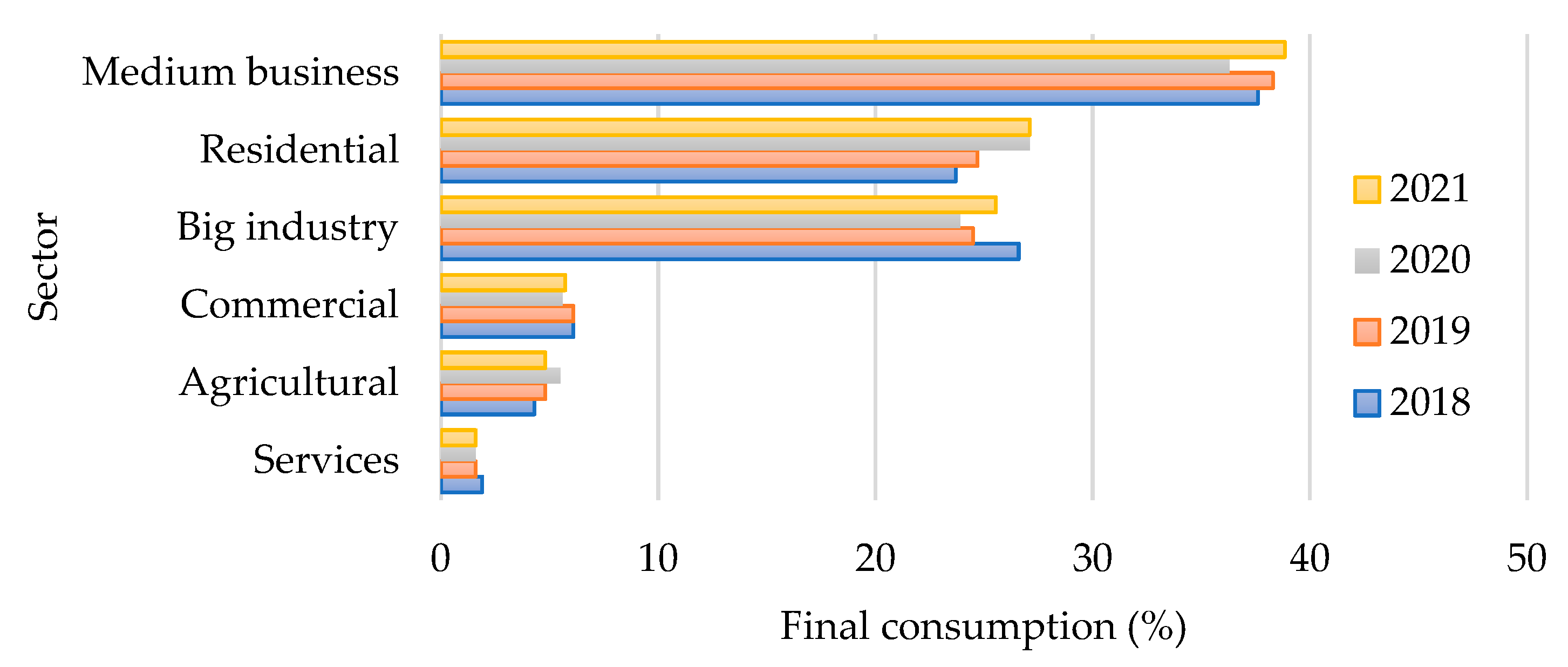

The sectors that reported the most changes in electricity consumption during the pandemic were medium business, residential, and big industry [55]. In 2018, the highest growth in electricity consumption was reported in medium business with 37.6%, followed by big industry with 26.6% and residential with 23.7%. The number of users with electricity services in 2018 amounted to 43.4 million. In 2019, the agricultural and services sectors increased by 10.4% and 15.8% their consumption, respectively, while big industry reduced its final consumption by 7.9%. In 2020, the agricultural sector presented the highest growth with 12.7%, followed by the residential sector with 8.9%. Derived from the strategies to contain the spread of COVID-19, the commercial and medium business sectors decreased their electricity consumption by 8.2% and 5.2%. In 2021, medium business and big industry presented the highest growth in electricity consumption with 6.5% and 6.4% compared to 2020, respectively. On the contrary, the agricultural sector had a fall of 12.7% this year, as shown in Figure 7.

5.3. Demand

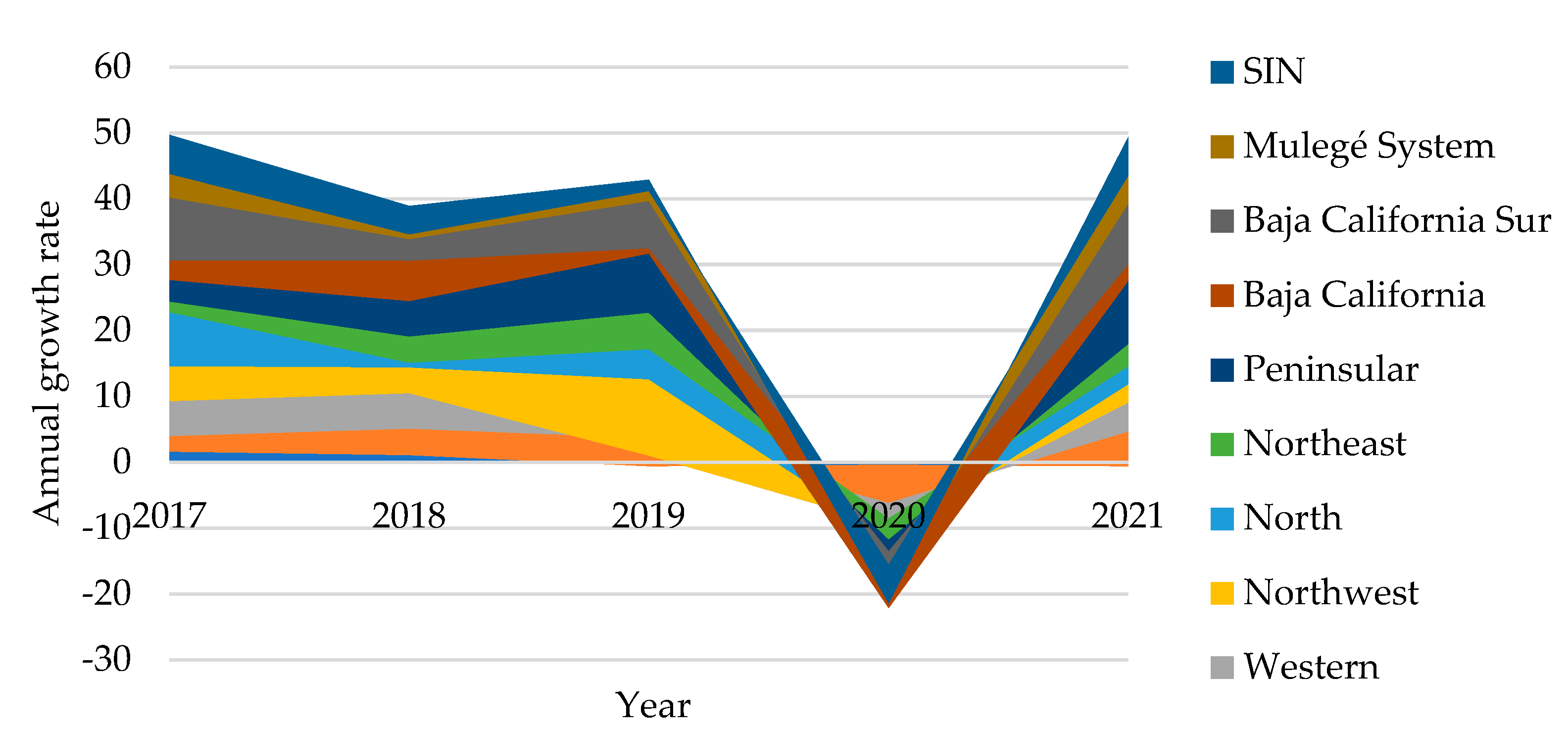

According to PRODESEN 2017-2032 [47], pre-pandemic period, the gross integrated demand of the SIN registered a value of 45.17 TWh/h, which is equivalent to a growth of 4.3% compared to the 43.32 MWh/h of 2017 (Table 5). In 2018, all the regions increased their electricity demand. Mainly, the Western and Peninsular regions had an increase of 5.4%, achieving 10.37 TWh/h and 2.25 TWh/h, respectively. The regions with the lowest demand were the Central and North regions with 1.1% (8.81 TWh/h) and 0.7% (4.64 TWh/h), respectively.

During the pandemic period (2019-2020), the demand continued to rise 1.7% with respect to 2018, going from 45.17 TWh/h to 45.95 TWh/h. The greatest recovery in electricity demand was in the Northwest region with 5.31 TWh/h, equivalent to 11.6%. Followed by the Northeast region with 5.5% (9.71 TWh/h) and the Eastern region with 4.3% (7.92 TWh/h). While the Western and Central regions had a reduction during the last week of April of 2.7% and 0.6%, respectively. In 2020, it was observed that most of the region decreased their electricity demand, due to social confinement and economic paralysis caused by the coronavirus, Figure 8. The Peninsular region demand fell 10.3%, achieving an electricity demand of 2.01 TWh/h, followed by the Eastern region with a decrease of 5.8%, going from 7.92 TWh/h to 7.45 TWh/h. The North region slightly increased its demand by 2.6% arriving at 4.98 TWh/h.

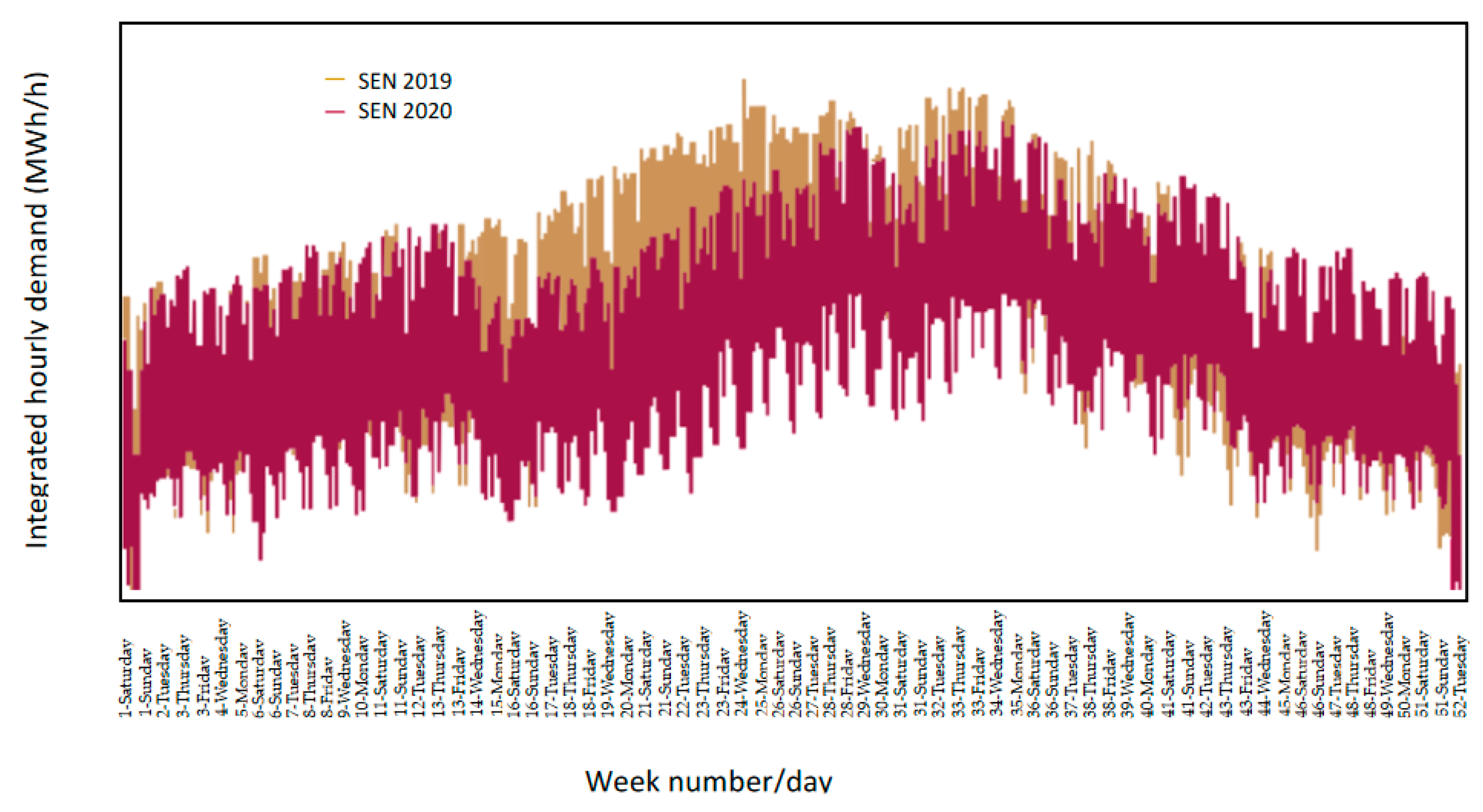

In relation to the hourly behaviour of the SEN demand, it can be seen that as of March 30, 2020 (week 14), the date that the immediate suspension of non-essential activities in Mexico was ordered, there is a significant drop in the peak of demand up to week 38 compared to 2019. Figure 9 shows the maximum demands on business days and on weekends decreased with respect to the usual pattern registered in previous years [54].

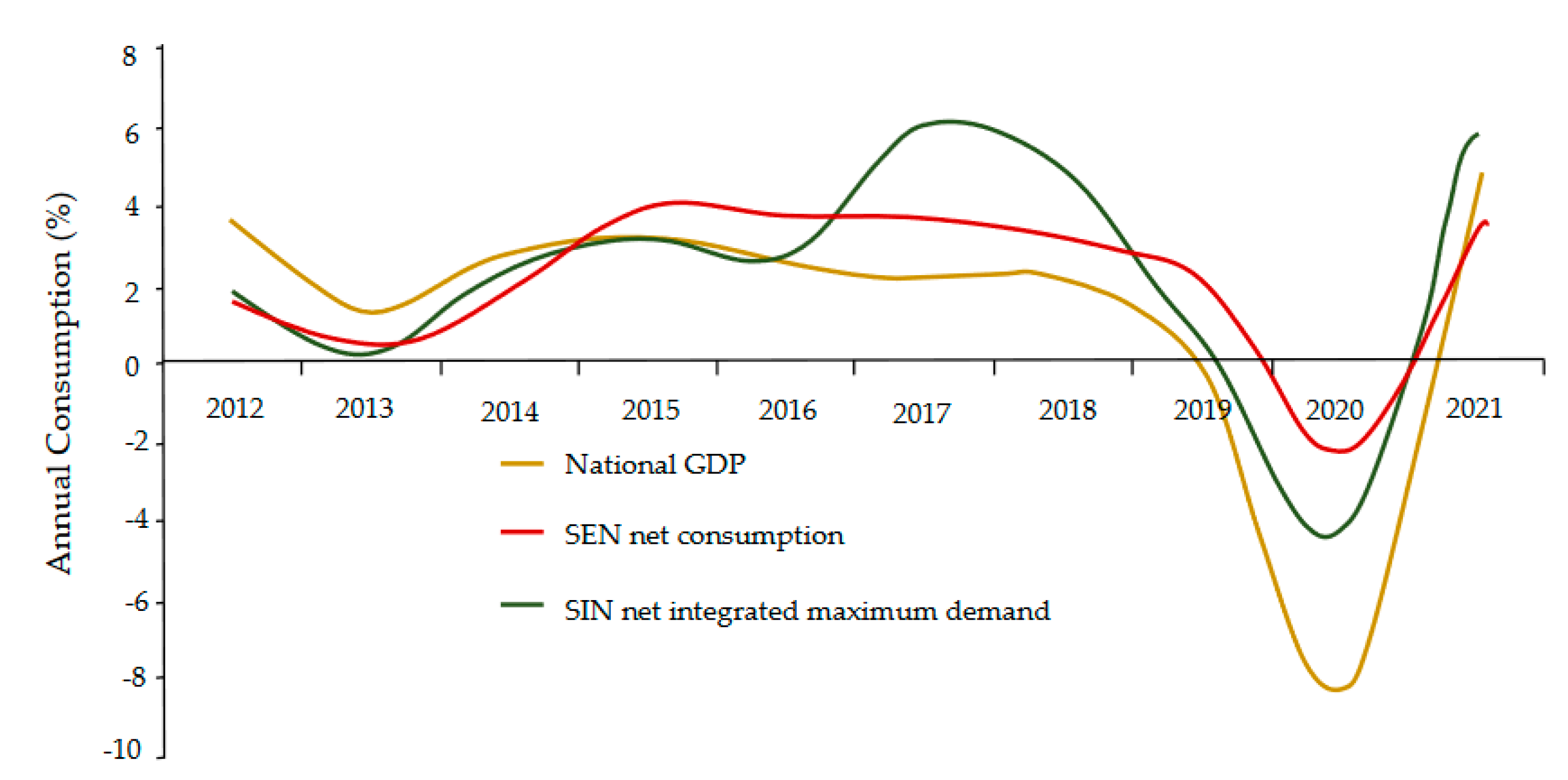

Mobility restrictions and the decrease in economic activities not only affected electricity demand but also GDP and SEN net consumption. The GDP in 2020 presented a lower annual variation than in 2019, with a decrease of the order of -8.2%, while gross consumption registered a decrease of -2.8%, a rate lower than that registered in 2019 of 2.1%, (Figure 10). This collapse is worrying because it is the deepest in almost ninety years. Its magnitude surpassed that of the global financial crisis of 2009, that of the debacles of 1995, 1986, and 1983, and is only surpassed by that of the Great Depression in 1932, when it was calculated that GDP fell 14.8% [54].

In the post-pandemic period, demand began to increase by up to 4%. The Peninsular and Eastern regions showed the highest increases with 9.6\% and 5.3% respectively and with less participation the Central region achieved 8.29 TWh/h (-0.6%), as shown in Table 5.

6. Discussion and Conclusion

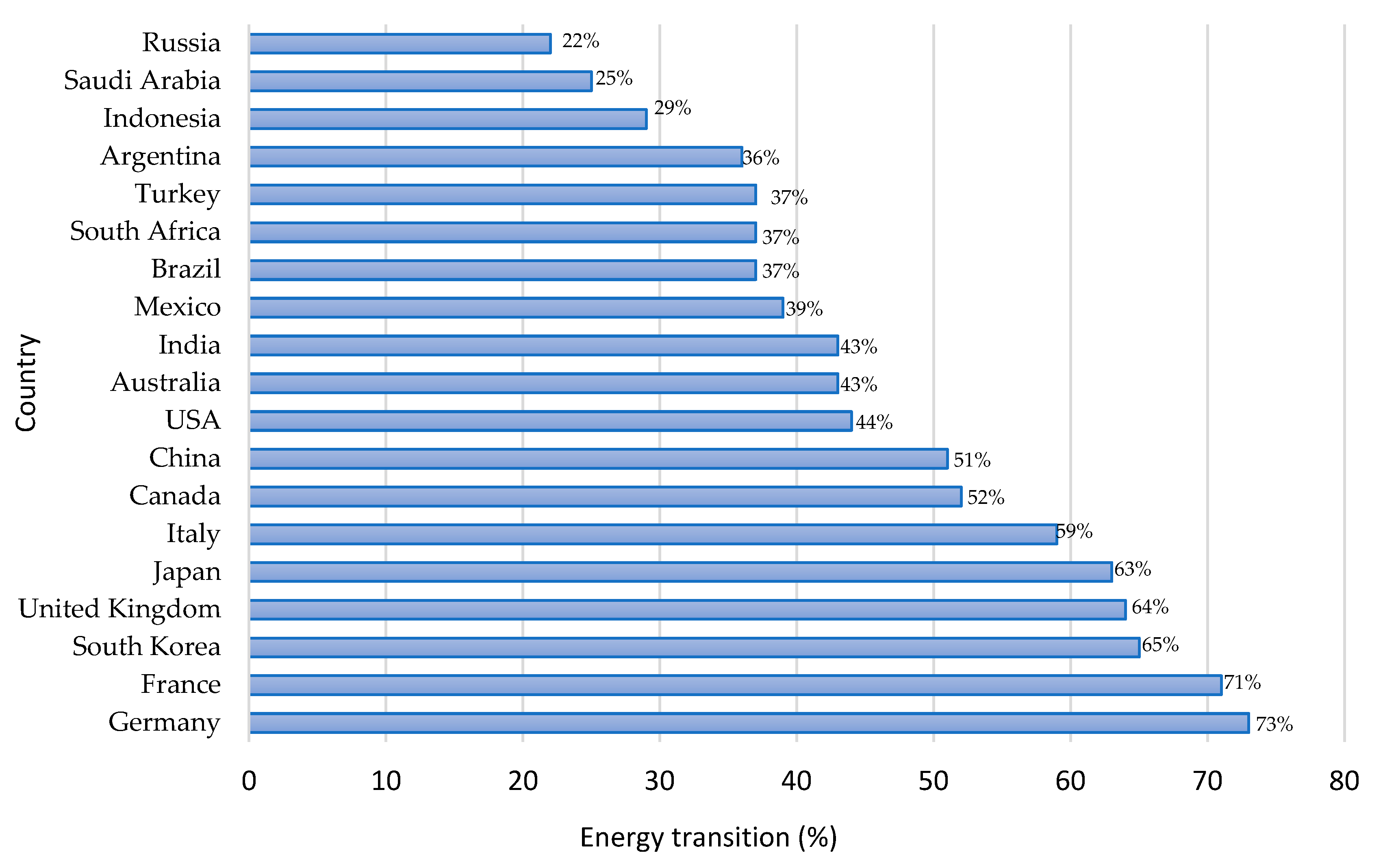

The purpose of this study was to gain a better understanding of the changes in electricity energy pre-, during, and post-COVID-19 pandemic in Mexico. The changes observed in the last five years have reflected a transformation in the matrix composition of electrical energy. Mexico has strongly promoted the development of renewable energies, especially electricity generated from the sun and wind. As a result, Mexico is among the top 12 countries in the world with the highest investment in clean sources, as shown in Figure 11.

Since 2017, Mexico has begun to make efforts to reform its energy sector, which has allowed a renewed dynamism in the national solar and wind industry. From the results, it is clear that Mexico has increased its total capacity by 22.83% from 2017-2021, despite the pandemic. During this period, the clean sources had a noteworthy increase of 43.1% of installed capacity, while the conventional sources have gradually grown by 9.31%.

In relation to electricity generation, it grew 4.3% in the last six years, going from 319.4 TWh in 2017 to 333.8 TWh in 2022. The clean sources grew 27.86% of electricity generation after three years of the energy policy promoted by the present administration. This growth is almost entirely attributed to the increase in electricity generation through clean technologies, with a slight stagnation in 2019, while conventional energies have had a reduction of 10% in electricity generation. Between 2019 and 2020, both conventional energy and clean energy had a slight stagnation or reduction in electricity generation. The results showed that conventional energies have had a reduction of 10% in electricity generation. The most affected technology was thermoelectric with 41.1% and coal-fired with 42%. While combined cycle, wind source, and solar photovoltaic increased by 11.8%, 49.59%, and 98.3% of electricity generation in this period, respectively.

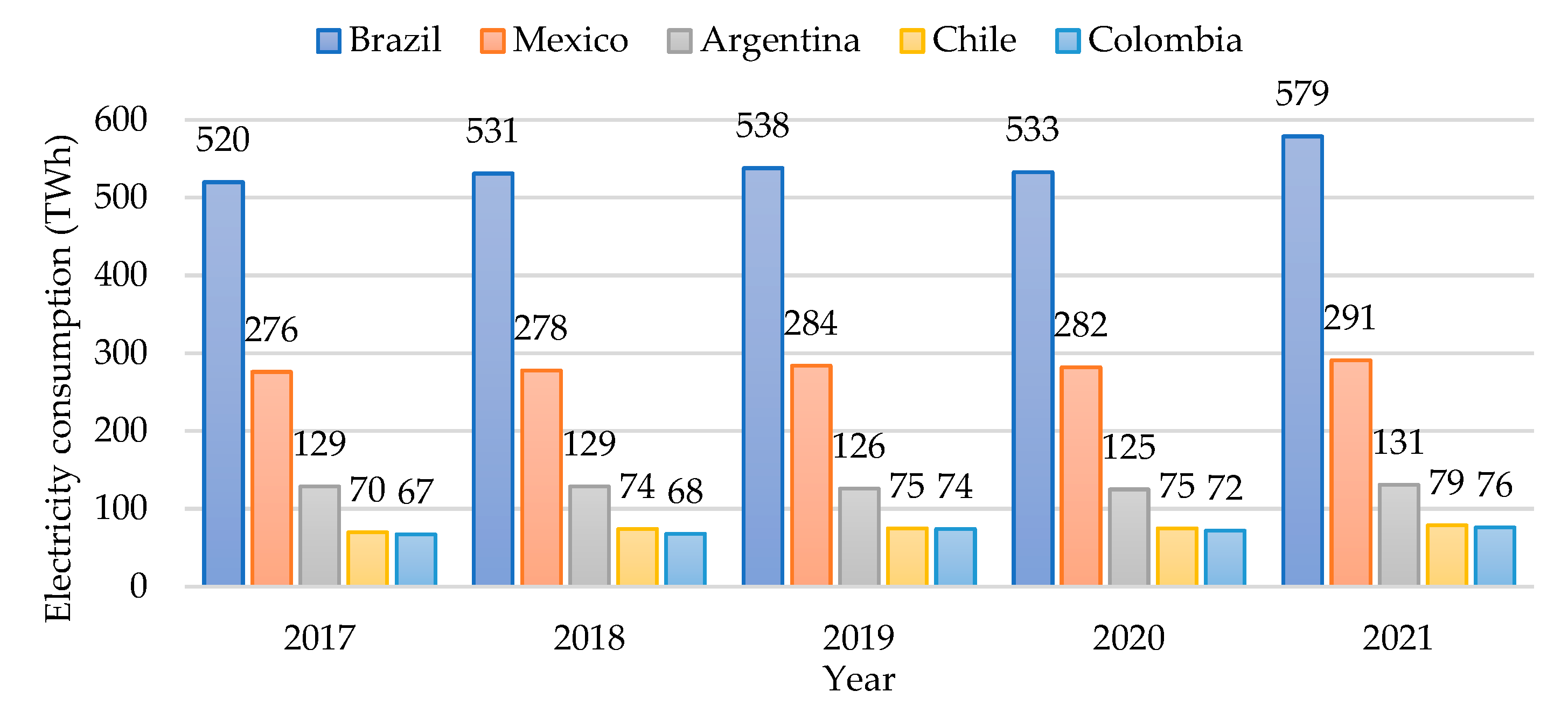

Another finding is that the gross national consumption had a gradual rise of 3.979%, passing from 309.73 TWh to 322.54 TWh. However, electricity consumption had a 2.7% decline due to the COVID-19 crisis and grew 2% in 2021, which translates into an economic recovery. Electricity consumption recovered 6.1% in Latin America, with growth of 8.6% in Brazil, 3.1 in Mexico, 4.6% in Argentina, 5% in Chile, and 5.3% in Colombia [58], as shown in Figure 12. The sectors with the greatest recovery were the medium business and big industry from the ravages of the pandemic. One interesting finding is the residential sector kept electricity consumption during 2020 and 2021. In this sense, a decrease was expected due to the return to industrial and daily activities.

The economic recovery also revived electricity demand. In Mexico, GDP, net consumption, and maximum net integrated demand were seriously affected during the year 2020. GDP fell 8.2% in 2020, the consumption and demand decreased by 2.2% and 4.4%, respectively. The most affected region was the Peninsular region demand with a drop of 10.3%, followed by the Eastern region with a decrease of 5.8%. It suggested a significant reduction in the generation of new jobs and an economic setback.

The results above show that Mexico is going through a gradual transition towards the de-carbonization of economic activities with the goal that the energy consumed comes from clean energy. It is noteworthy that the actions of the energy policy to eliminate competition in the energy market and strengthen PEMEX and CFE, as well as the goals of CO2 reduction by 2024 have delayed. The projections of the SENER affirm that the objective of generating 35% of its energy through clean technologies in 2024 will not be reached until 2031 and that 40% of the energy through clean technologies in 2032 will be reached by 2035 [59].

According to PRODESEN 2022-2036 projections, it is estimated that in a period of four years, the installed capacity of the SEN will increase by 20.425 GW, going from 89.89 GW in 2022 to 110.315 GW in 2026, which implies a growth average of 5.106 GW additional per year [60]. This annual average, however, is equivalent to 3.4 times the new capacity that was installed in 2022 (1,483 GW). If the new installed capacity contemplated in PRODESEN 2023-2037 is compared with the previous year's edition, the increase is considerable. The reports presented by IMCO [61] mention that CFE, which is solely responsible for expanding renewable generation capacity, currently does not have specific renewable generation projects in its project portfolio to expand the installed capacity at the rate that the country requires. Therefore, Mexico cannot successfully address the challenge of the energy transition that has been established.

Moreover, it is projected that distributed generation will grow 338% between 2022 and 2037, which will increase the installed capacity of distributed generation by 8,829 GW, going from 2,613 GW in 2022 to 11,442 GW in 2037 under a baseline scenario. This implies that in 2037 distributed generation will contribute around 15.54 TWh of electrical energy, a figure that is equivalent to 3.1% of the estimated total net consumption in 2023 (479,987 TWh). However, the preliminary draft of DACG on distributed generation threatens to limit the growth of this modality [62].

Although there is a framework of uncertainty, there are opportunities in different areas to support the country's energy transition, some of which involve the manufacturing and distribution of wind and photovoltaic equipment in the country. In the photovoltaic sector, Mexico has a large maquila industry where it exports photovoltaic cells, mainly to the United States and the Netherlands, however, the wind sector is limited only to exports to the United States. For this reason, the opportunity could be opened to include wind equipment manufacturers in the projects proposed by the Mexican government. On the other hand, the public administration could resume projects related to the public sector. An example would be the eight renewable energy projects, of which five are from the photovoltaic area, mentioned by PRODESEN 2019-2033. As well as projects derived from long-term auctions, which represent a total of 7.56 MW of installed capacity and which are stopped or in the process of being built [52].

Author Contributions

Lizbeth Salgado: Writing – original draft, Methodology, Formal analysis, Software, Investigation, Formal analysis, Carlos Álvarez: Writing – review & editing, Supervision, Investigation, Laura-Andrea Pérez – Information search, figure & table editing, Rodrigo Loera - review & editing.

Acknowledgments

The authors acknowledge financial support from CONAHCYT (México), TecNM projects, Cátedras CONAHCYT; and PRODEP through ITLAG-CA-10.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Daemi, Hakimeh Baghaei, et al. Progression and trends in virus from influenza A to COVID-19: an overview of recent studies. J. J. Viruses 2021, 13, 1145. [CrossRef] [PubMed]

- Yezli, Saber, and Anas Khan. COVID-19 social distancing in the Kingdom of Saudi Arabia: Bold measures in the face of political, economic, social and religious challenges. Travel Med Infect Dis. 2020, 37, 101692. [Google Scholar] [CrossRef]

- Acuña-Zegarra, Manuel Adrian, Mario Santana-Cibrian, and Jorge X. Velasco-Hernandez. Modeling behavioral change and COVID-19 containment in Mexico: A trade-off between lockdown and compliance. Math. Biosci. 2020, 325, 108370. [Google Scholar] [CrossRef]

- 4. Fana, Marta, et al. The COVID confinement measures and EU labour markets. Luxembourg: Publications office of the European Union, 2020.

- Sun, Kai Sing, et al. Effectiveness of different types and levels of social distancing measures: a scoping review of global evidence from earlier stage of COVID-19 pandemic. BMJ open 2022, 12, e053938. [CrossRef]

- Maliszewska, Maryla, Aaditya Mattoo, and Dominique Van Der Mensbrugghe. The potential impact of COVID-19 on GDP and trade: A preliminary assessment. World Bank policy res. Work. 2020, 9211.

- Wang, Bowen, et al. Crises and opportunities in terms of energy and AI technologies during the COVID-19 pandemic. Energy and AI 2020, 1, 100013. [Google Scholar] [CrossRef]

- Basak, Palash, et al. A global study on the correlates of gross domestic product (GDP) and COVID-19 vaccine distribution. Vaccines 2022, 10, 266. [CrossRef]

- Baldwin, Richard E., and Eiichi Tomiura. Thinking ahead about the trade impact of COVID-19. 2020.

- Barbero, Javier, Juan José de Lucio, and Ernesto Rodríguez-Crespo. Effects of COVID-19 on trade flows: Measuring their impact through government policy responses. PloS one 2021, 16, e0258356.

- Kooli, Chokri. COVID-19: Challenges and opportunities. Avicenna Editorial 2021, 1, 10-5339. [CrossRef]

- Palomino, Juan C., Juan G. Rodríguez, and Raquel Sebastian. The COVID-19 shock on the labour market: Poverty and inequality effects across Spanish regions. Reg. Stud. 2023, 57, 814–828. [CrossRef]

- Sonfield, Adam, et al. COVID-19 job losses threaten insurance coverage and access to reproductive health care for millions. Health Affairs Forefront 2020.

- Ahmed, Faheem, et al. Why inequality could spread COVID-19. The Lancet Public Health 2020, 5, e240. [CrossRef]

- Wiwad, Dylan, et al. Recognizing the impact of COVID-19 on the poor alters attitudes towards poverty and inequality. J. Exp. Soc. Psychol. 2021, 93, 104083. [Google Scholar] [CrossRef]

- Gollakota, Anjani RK, and Chi-Min Shu. COVID-19 and energy sector: Unique opportunity for switching to clean energy. Gondwana Res. 2023, 114, 93–116. [Google Scholar] [CrossRef]

- Elavarasan, Rajvikram Madurai, et al. COVID-19: Impact analysis and recommendations for power sector operation. Appl. energy 2020, 279, 115739. [CrossRef]

- Zhong, Haiwang, et al. Implications of COVID-19 for the electricity industry: A comprehensive review. CSEE J. Power and Energy Syst. 2020, 6, 489–495. [CrossRef]

- Saadat, Saeida, Deepak Rawtani, and Chaudhery Mustansar Hussain. Environmental perspective of COVID-19. Sci. of the Total Environment 2020, 728, 138870. [Google Scholar] [CrossRef] [PubMed]

- Sikarwar, Vineet Singh, et al. COVID-19 pandemic and global carbon dioxide emissions: A first assessment. Sci. of the Total Environment 2021, 794, 148770. [Google Scholar] [CrossRef] [PubMed]

- Mastoi, Muhammad Shahid, et al. A critical analysis of the impact of pandemic on China’s electricity usage patterns and the global development of renewable energy. IJERPH 2022, 19, 4608. [CrossRef]

- Wang, Qiang, Shuyu Li, and Feng Jiang. Uncovering the impact of the COVID-19 pandemic on energy consumption: New insight from difference between pandemic-free scenario and actual electricity consumption in China. J. Clean. Prod. 2021, 313, 127897. [CrossRef] [PubMed]

- Bhattacharya, Subhadip, et al. Analysing the impact of lockdown due to the COVID-19 pandemic on the Indian electricity sector. Int. J. Electric. Power Energy Syst. 2022, 141, 108097. [Google Scholar] [CrossRef]

- World Energy Primary Production https://yearbook.enerdata.net/total-energy/world-energy-production.html (accessed on 28 June 2023). (accessed on 28 June 2023).

- Abu-Rayash, Azzam, and Ibrahim Dincer. Analysis of the electricity demand trends amidst the COVID-19 coronavirus pandemic. ERSS 68 (2020) 101682. [CrossRef]

- Alasali, Feras, et al. Impact of the COVID-19 pandemic on electricity demand and load forecasting. Sustainability 2021, 13, 1435. [CrossRef]

- Narajewski, Michał, and Florian Ziel. Changes in electricity demand pattern in Europe due to COVID-19 shutdowns. arXiv, 2020; arXiv:2004.14864.

- Agdas, Duzgun, and Prabir Barooah. Impact of the COVID-19 pandemic on the US electricity demand and supply: An early view from data. Ieee Access 2020, 8, 151523–151534. [CrossRef] [PubMed]

- Wu, Jinran, et al. An evaluation of the impact of COVID-19 lockdowns on electricity demand. Electr. Power Syst. Res. 2023, 216, 109015. [CrossRef]

- Aktar, Most Asikha, Md Mahmudul Alam, and Abul Quasem Al-Amin. Global economic crisis, energy use, CO2 emissions, and policy roadmap amid COVID-19. Sustain. Prod. Consum. 2021, 26, 770–781. [CrossRef] [PubMed]

- López-Sosa, Luis Bernardo, et al. COVID-19 pandemic effect on energy consumption in state universities: Michoacan, Mexico case study. Energies, 2021; 14, 7642. [CrossRef]

- Escudero, Xavier, et al. The SARS-CoV-2 (COVID-19) coronavirus pandemic: Current situation and implications for Mexico. Archivos de cardiología de México 2020, 90, 7–14. [CrossRef] [PubMed]

- Public Media Service https://www.capital21.cdmx.gob.mx/noticias/?p=12574 (accessed on 16 March, 2023).

- IBERO 2020 Breve cronología de la pandemia 2020 https://revistas.ibero.mx/ibero/uploads/volumenes/55/pdf/breve-cronologia-de-la-pandemia.pdf (accessed on 16 March 2023). (accessed on 16 March 2023).

- COVID-19 Timeline in Mexico -INAI https://micrositios.inai.org.mx/conferenciascovid-19tp/?page_id=8432 (accessed on 16 March 2023). (accessed on 16 March 2023).

- Timeline – Coronavirus Contingency -CVOED -IMSS https://cvoed.imss.gob.mx/cronologia-contingencia-por-coronavirus/ (accessed on 18 March 2023). (accessed on 18 March 2023).

- Sistema Electrico Nacional, SEN https://www.cenace.gob.mx/Paginas/SIM/OperacionSEN.aspx#:~:text=El%20SEN%20est%C3%A1%20integrado%20por,la%20RNT%20o%20a%20las%20RGD (accessed on March 21, 2023).

- CENACE https://www.cenace.gob.mx/CENACE.aspx (accessed on March 21, 2023).

- Vásquez, P. K. Vásquez, P. K., et al. Diagnóstico Situacional para la implementación de un proceso de Gestión de Conocimiento en el Operador Nacional de Electricidad CENACE. Revista Técnica energía 2017, 13, 222–232. [Google Scholar] [CrossRef]

- National Program for Sustainable Use https://dof.gob.mx/nota detalle.php?codigo=5679748&fecha=16/02/2023 (accessed on March 21, 2023).

- Zenón, Eric, and Juan Rosellón. Optimal transmission planning under the Mexican new electricity market. Energy Policy 2017, 104, 349–360. [Google Scholar] [CrossRef]

- National Energy Balance 2018-2025. https://sie.energia.gob.mx/bdiController.do?action=cuadro&cvecua=DIPS SE C33 ESP (Accessed on April 4, 2023).

- Energetic Reform 2017 https://www.asf.gob.mx/uploads/61 Publicacionestecnicas/16 Reforma energetica 2017.pdf (accessed on May 8, 2023).

- Sector program derived from the National Development Plan 2019-2024 https://www.dof.gob.mx/nota detalle.php?codigo=5596374&fecha=08/07/2020 (accessed on May 24th, 2023).

- Progress in Clean Energies 2017 https://www.gob.mx/cms/uploads/attachment/file/354379/Reporte_de_Avance_de_Energ_as_Limpias_Cierre_2017.pdf (Accessed on May 8, 2023).

- Energías alternativas, retos y oportunidades en México https://realestatemarket.com.mx/articulos/infraestructura-y-construccion/27581-energias-alternativas-retos-y-oportunidades-en-mexico\#:~:text=El\%202018%20fue%20el%20mayor,capacidad%20instalada%20respecto%20a%202017 (Accessed on May 8, 2023).

- PRODESEN 2018-2032 https://www.cenace.gob.mx/Docs/16\_MARCO\\REGULATORIO/Prodecen//08%202018-2032%20Cap%C3%ADtulos%201%20al%206.pdf (Accessed on May 15, 2023).

- Annual Report 2019 CFE https://www.cfe.mx/finanzas/reportes-financieros/Informe%20Anual%20Documentos/Informe%20Anual%202019%20V12%20a%20portal.pdf (Accessed on May 15, 2023).

- CENACE, fallas del Sistema Nacional https://www.cenace.gob.mx/Docs/16\_MARCOREGULATORIO/SENyMEM/(Acuerdo%202020-05-01%20CENACE)%20Acuerdo%20para%20garantizar%20la%20eficiencia,%20Calidad,%20Confiabilidad,%20Continuidad%20y%20seguridad.pdf (Accessed on May 8, 2023).

- CENACE, Report of the energy generated by type https://www.cenace.gob.mx/Paginas/SIM/Reportes/EnergiaGeneradaTipoTec.aspx (Accessed on June 17, 2023).

- Secretaria de Energía, Informe pormenorizado sobre el desempeño y las tendencias de la industria eléctrica nacional 2017 Informe sobre la participación de las energías renovables en la generación de electricidad en México, al 31 de diciembre de 2013 (www.gob.mx) (Accessed on June 14, 2023).

- PRODESEN 2019-2033 https://www.cenace.gob.mx/Docs/16_MARCOREGULATORIO/Prodecen//10%202019-2033%20Cap%C3%ADtulos%201%20al%206.pdf (Accessed on June 12, 2023).

- PRODESEN 2020-2034 https://www.cenace.gob.mx/Docs/16_MARCOREGULATORIO/Prodecen//12%202020-2034%20Cap%C3%ADitulos%201%20al%206.pdf (Accessed on June 12, 2023).

- PRODESEN 2021-2035 https://www.cenace.gob.mx/Docs/16\_MARCOREGULATORIO/Prodecen//14%202021-2035%20Cap%C3%ADtulos%201%20al%206.pdf (Accessed on June 12, 2023).

- PRODESEN 2022-2036 https://www.cenace.gob.mx/Docs/16_MARCOREGULATORIO/Prodecen//15%202022-2036%20Cap%C3%ADtulos%207%20al%209%20y%20Anexos.pdf (Accessed on June 12, 2023).

- Instituto Mexicano de la Competitividad https://imco.org.mx/wp-content/uploads/2023/02/Situacion-del-agua-en-Mexico (Accessed on June 19, 2023).

- Public Policy Research Center IMCO 2022a https://imco.org.mx/wp-content/uploads/2022/09/La-energia-que-queremos\_Documento.pdf (Accessed on July 11, 2023).

- Statistical Yearbook 2023 ENERDATA https://datos.enerdata.net/electricidad/datos-consumo-electricidad-hogar.html (Accessed on July 11, 2023).

- Public Policy Research Center IMCO https://imco.org.mx/prodesen-refleja-una-falta-de-compromiso-del-estado-mexicano-con-el-medio-ambiente/ (Accessed on July 7, 2023).

- Mexican Institute of Competitiveness https://imco.org.mx/wp-content/uploads/2022/06/Nota-informativa\_Prodesen\_22010603.pdf (Accessed on July 7, 2023).

- Public Policy Research Center IMCO 2022 https://imco.org.mx/prodesen-refleja-una-falta-de-compromiso-del-estado-mexicano-con-el-medio-ambiente/ (Accessed on July 11, 2023).

- Prodesen 2023-2037 https://imco.org.mx/el-prodesen-2023-2037-incrementa-artificialmente-las-cifras-de-generacion-de-energia-limpia-en-mexico/ (Accessed on July 11, 2023).

Figure 1.

Timeline of the COVID-19 in Mexico.

Figure 2.

Regions of the National Electrical System: 1) Central, 2) Eastern, 3) Western, 4) Northwest, 5) North, 6) Northeast, 7) Baja California, 8) Peninsular, 9) Baja California Sur and 10) Mulegé System [37].

Figure 2.

Regions of the National Electrical System: 1) Central, 2) Eastern, 3) Western, 4) Northwest, 5) North, 6) Northeast, 7) Baja California, 8) Peninsular, 9) Baja California Sur and 10) Mulegé System [37].

Figure 3.

Installed capacity from 2018 to 2022.

Figure 4.

Electricity generation from 2017 to 2021 in Mexico.

Figure 5.

Evolution of electricity consumption from 2017 to 2021 in Mexico.

Figure 6.

Monthly consumption from 2017 to 2021 in Mexico.

Figure 7.

Electricity consumption by sectors [55].

Figure 7.

Electricity consumption by sectors [55].

Figure 8.

Annual growth rate of demand from 2017-2021.

Figure 9.

Hourly profile of demand of the SEN from 2019 to 2020 [54].

Figure 9.

Hourly profile of demand of the SEN from 2019 to 2020 [54].

Figure 10.

Evolution of national GDP, consumption and net maximum integrated demand from 2017 to 2021 [54].

Figure 10.

Evolution of national GDP, consumption and net maximum integrated demand from 2017 to 2021 [54].

Figure 11.

Monitoring of G20 policies in energy transition 2021 [57].

Figure 11.

Monitoring of G20 policies in energy transition 2021 [57].

Figure 12.

Electricity consumption in Latin America from 2017 to 2021 [58].

Figure 12.

Electricity consumption in Latin America from 2017 to 2021 [58].

Table 1.

List of abbreviations.

| Acronyms | Description (Spanish) | Description (English) |

|---|---|---|

| CENACE | Centro Nacional de Control de Energía | National Centre of Energy Control |

| CFE | Comisión Federal de Electricidad | Federal Electricity Commission |

| DACG | Disposiciones administrativas generales | General Administrative Provisions |

| GSP | Producto Interno Bruto | Gross Domestic Product |

| IMCO | Centro de Investigación de Políticas Públicas | Public Policy Research Center |

| MEM | Mercado Eléctrico Mayorista | Wholesale Electricity Market |

| PEMEX | Petróleos Mexicanos | Mexican oil |

| PRODESEN | Programa para el Desarrollo del Sistema Eléctrico Nacional | Development of the National Electric System |

| SEN | Sistema Eléctrico Nacional | National Electric System |

| SENER | Secretaría de Energía | Mexican Ministry of Energy |

| SIN | Sistema Interconectado Nacional | National Interconnected System |

| TEM | Transición Energética Mexicana | Mexican Energy Transition |

| WHO | Organización Mundial de la Salud | World Health Organisation |

Table 2.

Evolution of installed capacity from 2017-2022 [42].

Table 2.

Evolution of installed capacity from 2017-2022 [42].

| Technology | Pre-COVID-19 | COVID-19 | Post-COVID-19 | |||

|---|---|---|---|---|---|---|

| Year | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

| Combined cycle | 28.08 | 33.72 | 34.28 | 35.15 | 36.87 | 40.59 |

| Thermoelectric | 12.59 | 11.71 | 8.23 | 7.48 | 7.16 | 5.12 |

| Coal-fired | 5.38 | 5.51 | 5.51 | 5.51 | 5.51 | 5.51 |

| Turbogas | 5.14 | 5.06 | 5.75 | 5.75 | 5.66 | 5.31 |

| Internal combustion | 1.63 | 1.66 | 1.66 | 1.77 | 1.69 | 1.74 |

| Fluidized bed | 0.58 | 0.58 | 0.58 | 0.58 | 0.58 | 0.58 |

| Hydroelectric | 12.64 | 12.67 | 12.67 | 12.67 | 12.67 | 12.67 |

| Wind | 4.19 | 6.59 | 8.13 | 8.86 | 11.23 | 12.42 |

| Geothermal | 0.93 | 0.94 | 0.91 | 0.89 | 0.89 | 0.89 |

| Solar Photovoltaic | 0.21 | 4.43 | 5.63 | 7.55 | 7.75 | 8.05 |

| Nucleoelectric | 1.61 | 1.61 | 1.61 | 1.61 | 1.61 | 1.61 |

| Bioenergy | 1.01 | 1.01 | 1.01 | 1.05 | 1.29 | 1.58 |

| Efficient cogeneration | 1.23 | 1.93 | 1.93 | 1.93 | 1.93 | 2.01 |

| Regenerative brakes | 0.007 | 0.007 | 0.07 | 0.07 | 0.07 | 0.07 |

| Total (GW) | 75.7 | 87.44 | 87.97 | 90.82 | 94.87 | 98.1 |

| Technology | Pre-COVID-19 | COVID-19 | Post-COVID-19 | ||

|---|---|---|---|---|---|

| Year | 2017 | 2018 | 2019 | 2020 | 2021 |

| Combined cycle | 165.25 | 163.88 | 175.51 | 185.64 | 186.72 |

| Thermoelectric | 42.78 | 39.34 | 38.02 | 22.41 | 22.19 |

| Coal-fired | 30.55 | 27.35 | 21.61 | 12.53 | 8.70 |

| Turbogas | 12.85 | 9.51 | 10.90 | 8.66 | 11.15 |

| Internal combustion | 4.01 | 2.59 | 3.19 | 2.84 | 2.12 |

| Hydroelectric | 31.85 | 32.23 | 23.20 | 26.82 | 34.72 |

| Wind | 10.62 | 12.44 | 16.73 | 19.70 | 21.07 |

| Geothermal | 6.04 | 5.06 | 5.06 | 4.57 | 4.24 |

| Solar Photovoltaic | 0.344 | 3.211 | 9.96 | 15.84 | 20.19 |

| Bioenergy | 1.88 | 1.99 | 1.87 | 2.21 | 1.59 |

| Nucleoelectric | 10.88 | 13.2 | 10.88 | 10.86 | 11.61 |

| Efficient cogeneration | 6.93 | 2.42 | 3.38 | 4.29 | 3.42 |

| Regenerative brakes | 0.004 | 0.004 | 0.004 | 0.004 | 0.004 |

| Total (TWh) | 329.16 | 313.98 | 321.58 | 317.27 | 328.59 |

| Technology | Pre-COVID-19 | COVID-19 | Post-COVID-19 | ||

|---|---|---|---|---|---|

| 2017 | 2018 | 2019 | 2020 | 2021 | |

| Central 1 | 60.68 | 61.29 | 60.85 | 57.43 | 56.87 |

| Eastern | 48.58 | 50.28 | 51.66 | 50.44 | 52.07 |

| Western | 66.69 | 68.11 | 69.69 | 68.15 | 69.89 |

| Northwest | 24.29 | 24.68 | 24.97 | 26.1 | 25.55 |

| North | 25.95 | 27 | 28.87 | 29.29 | 28.95 |

| Northeast | 54.42 | 56.43 | 54.42 | 54.24 | 57.15 |

| Peninsular | 12.49 | 12.98 | 13.87 | 12.49 | 13.55 |

| SIN | 282.66 | 300.79 | 307.33 | 298.15 | 304.02 |

| Baja California | 13.83 | 14.54 | 14.62 | 14.94 | 15.54 |

| Baja California Sur | 2.62 | 2.76 | 2.82 | 2.72 | 2.83 |

| Mulegé System | 0.152 | 0.155 | 0.155 | 0.159 | 0.15 |

| SEN (TWh) | 309.73 | 318.24 | 324.93 | 315.97 | 322.54 |

| Technology | Pre-COVID-19 | COVID-19 | Post-COVID-19 | ||

|---|---|---|---|---|---|

| Year | 2017 | 2018 | 2019 | 2020 | 2021 |

| Central | 8.71 | 8.81 | 8.75 | 8.72 | 8.29 |

| Eastern | 7.29 | 7.59 | 7.92 | 7.45 | 7.74 |

| Western | 9.84 | 10.37 | 10.09 | 9.76 | 10.17 |

| Northwest | 4.58 | 4.76 | 5.31 | 5.31 | 5.31 |

| North | 4.61 | 4.64 | 4.85 | 4.98 | 4.98 |

| Northeast | 8.85 | 9.2 | 9.71 | 9.39 | 9.53 |

| Peninsular | 1.96 | 2.06 | 2.25 | 2.01 | 2.19 |

| Baja California | 2.69 | 2.86 | 2.89 | 3.12 | 3.15 |

| Baja California Sur | 0.48 | 0.5 | 0.54 | 0.51 | 0.54 |

| Mulegé System | 0.03 | 0.03 | 0.03 | 0.03 | 0.03 |

| SIN (TWh) | 43.32 | 45.17 | 45.95 | 43.27 | 45.24 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.