Submitted:

23 November 2023

Posted:

23 November 2023

You are already at the latest version

Abstract

In exploring the intricacies of financial analysis, this study delves into the efficacy of traditional financial ratios versus cash flow ratios in foreseeing a company's fiscal well-being. By harnessing the PRISMA 2020 framework, an exhaustive and systematic dissection of diverse scholarly articles was embarked upon. The quest was to unearth the more reliable predictor of financial stability among these two sets of ratios. With a methodical examination of academic writings, this inquiry juxtaposed various models, scrutinizing their foresight capabilities. The revelations were telling; cash flow ratios emerged as more potent forecasters compared to their traditional counterparts. Intriguingly, models that blend both ratio types showed a marked improvement in predictive accuracy, hinting at a synergistic effect. This underscores the insight that while traditional ratios are informative, their amalgamation with cash flow ratios yields a richer, more rounded grasp of a company’s fiscal state. Conclusively, for stakeholders, especially investors, adopting this dual-ratio approach is pivotal for enlightened decision-making. This research enriches the financial analysis domain by spotlighting the salience of cash flow ratios, advocating for their integration with conventional methods for a sharper financial health appraisal.

Keywords:

financial analysis

; Traditional Financial Ratios

; Cash Flow Ratios

; Redictive Efficacy

; Fiscal Health

; Systematic Review

; PRISMA 2020

; Financial Stability

1. Introduction

The assessment of a company's financial performance is a crucial aspect of business analysis, and ratio analysis is an essential tool in this regard. By analyzing different financial ratios, experts can obtain valuable insights into a company's liquidity, operational efficiency, profitability, and general financial well-being (Abualrob and Maswadeh 2020; DAHIYAT, WESHAH, and ALDAHIYAT 2021). Among the several ratios used, liquidity ratios, profitability ratios, solvency ratios, and efficiency ratios are the most common (Barua and Saha 2015; DAHIYAT, WESHAH, and ALDAHIYAT 2021; Rahman 2017). Each classification of ratios provides specific information that helps to understand the different aspects of a company's financial performance. Thus, a comprehensive analysis of such ratios can lead to deeper insights into a company's financial strengths and weaknesses.

Cash flow ratios are considered to be more trustworthy indicators of liquidity ratios compared to conventional liquidity ratios like the acid-test ratio or the current ratio. The latter ratios provide a static view of the liquidity status by measuring a single point in time, whereas the former ratios present a dynamic view of the company's liquidity by capturing the changes in the statements. Moreover, general liquidity figures may include arbitrary non-cash allocations, which can be misleading. In contrast, cash flow ratios concentrate on what shareholders value the most, i.e., cash available for operation and investment (Atieh 2014). Creditors and lenders prefer cash flow ratios to traditional ratios because they provide a more comprehensive understanding of the company's ability to meet its payment obligations. The traditional ratios, however, only reflect the cash availability at a specific date in the past (Agarwal and Taffler 2008; Yap, Yong, and Poon 2010). Cash flow ratios provide a more detailed understanding of a company's available resources for fulfilling its obligations by comparing the amount of cash generated within a specific time frame with its short-term liabilities. This allows for a clearer depiction of the company's financial standing (Mills and Yamamura 1998; Porwal and Jain 2013).

The purpose of this systematic review is to document the behavior of traditional ratios versus cash flow ratios, in predicting the future financial performance of businesses and as a tool in the hands of interested members to improve the quality of decision-making. The results of the study can be useful to investors and other stakeholders in making informed decisions about a company's financial performance.

2. Methodology

The objective of this investigation is to respond to the subsequent research inquiry:

How do traditional numerators behave compared to cash flow ratios as a tool in the hands of stakeholders to improve the quality of decision-making and predict the future financial performance of businesses?

The online databases Scholar and Scopus are used to find relevant studies. For this work, researchers are sought from the international literature, which makes comparisons between traditional indicators and cash flow indicators, in the databases of Scopus and Scholar. The algorithm used in the Scopus database is:

TITLE-ABS-KEY (traditional OR "traditional ratio*" OR accrual OR "financial ratio*") AND ("cash flow" OR "cash flow ratio*") AND (compar* OR analysis OR perform* OR predict*) AND PUBYEAR > 1999 AND PUBYEAR < 2024 AND PUBYEAR > 1999 AND PUBYEAR < 2024 AND PUBYEAR > 1999 AND PUBYEAR < 2024 AND PUBYEAR > 1999 AND PUBYEAR < 2024 AND (LIMIT-TO (OA, "all")) AND (LIMIT-TO (LANGUAGE, "English")) AND (LIMIT-TO (DOCTYPE, "ar"))

The choice of the English language is judged to be the most appropriate since it is the most popular among researchers (LIMIT-TO (LANGUAGE, "English")). In addition, the period 2000 – 2023 is set, as the time range of publication of the researches under consideration (PUBYEAR> 1999 AND PUBYEAR< 2024). Also, the search selects articles (DOCTYPE, "ar") as well as those from which access is available (LIMIT-TO (OA, "all"))

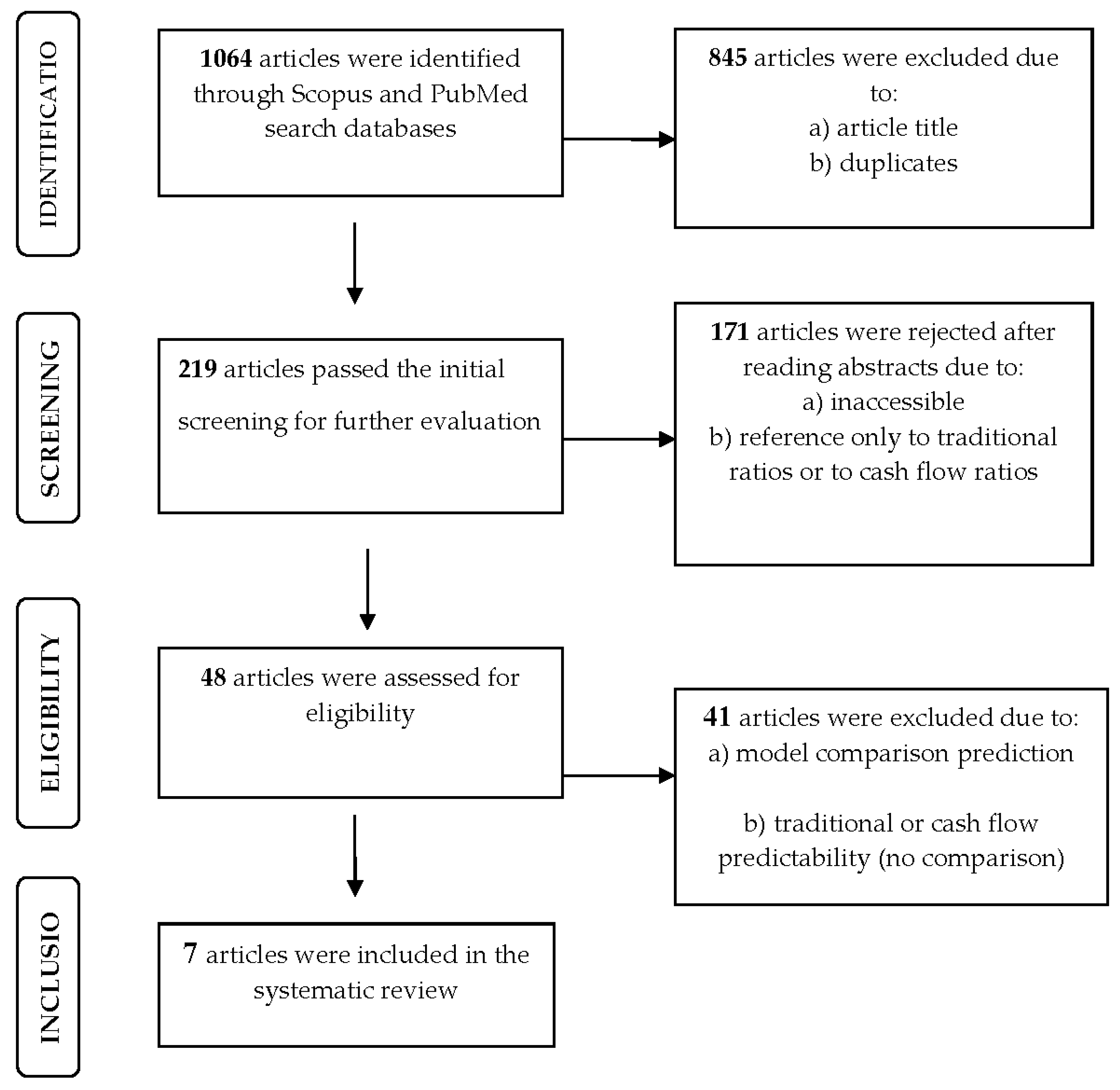

The same keywords are used for the Scholar database. Accordingly, the inclusion criteria are the same (language, timespan of the examinees, articles, etc.). The articles that meet the above criteria as well as the procedure followed for the collection of the studies that answer the research question are given in Figure 1. From each study relevant data are extracted such as: A) The study purpose B) the methodology followed C) the results obtained (through statistical analysis) from the comparison of traditional ratios with cash flow ratios. A systematic review is conducted in this study, following the steps of PRISMA 2020 (Page et al. 2021), as a guideline.

3. Results

Table 1.

Summary of systematic review studies

| Reference | Aim | Methodology | Results |

|---|---|---|---|

| (Bhandari, Showers, and Johnson-Snyder 2019) | Investigating the forecasting accuracy of six traditional ratios, six cash flow ratios, their combination (12 ratios), and a four-variable model containing two traditional and two cash flow-based ratios, based on financial data of companies during the period 2008- 2010. | The utilization of discriminant analysis (DA) involves the processing of a linear equation that is composed of numerous predictor variables. | a) Measures that focus on cash flow tend to be more effective in forecasting future outcomes. b) Models that employ both accrual-based and cash-flow-based ratios outperform other models in terms of their performance |

| (Waqas and Md-Rus 2018) | Identifying Financial Indicators Predictors of Financial Distress Affecting Pakistani Firms. | The variables used to measure the financial performance of a firm include financial ratios that assess profitability, liquidity, leverage, and cash flows. Additionally, two major market factors are taken into account: the size and idiosyncratic standard deviation of the stock returns for each company (SIG). To forecast financial distress, a logit regression is used on a sample of 290 firms spanning from 2007 to 2016. | a) Profitability, liquidity, leverage, cash flow ratios, and firm size have a notable impact in predicting financial distress. b) The SIG factor is insignificant in this regard. |

| (Barua and Saha 2015) | The exploration of the potential of traditional and cash flow ratios in the prediction of forthcoming cash flows in Bangladeshi companies is the main focus of this study. | To maintain uniformity and simplify comparisons, the same technique is employed when analyzing the Balance Sheet, Income Statement, and Cash Flow Statement. Additionally, calculations of cash flow ratios and income statement-based ratios are included. The cash flow data is directly sourced from cash flow statements. To highlight any noteworthy discrepancies between the traditional income statement-based ratios and cash flow-based ratios, percentage differences are computed. | Based on empirical evidence, it has been established that the cash flow and accrual components of earnings are reliable indicators for forecasting future cash flows of Bangladeshi companies listed on the stock market. It has also been concluded that cash flow ratios are more effective in predicting future cash flows compared to traditional ratios. Nevertheless, it should be noted that the accuracy of the financial picture offered by cash flow ratios is not always superior and may vary. |

| (Mavengere 2015) | The examination of the significance of conventional ratios when compared to cash flow ratios in evaluating the liquidity of retail companies listed on the Zimbabwe Stock Exchange is a topic of great importance. This analysis is particularly relevant to investors who are seeking to make informed decisions. The emphasis of this examination is on the potential implications of these ratios for investor decision-making. | During a span of 5 years, from 2010 to 2014, an examination was conducted on businesses operating in the same industry. The financial data was gathered from the respective company websites. To determine the significance of statistical variations between conventional ratios and cash flow ratios, a non-parametric test known as the Mann-Whitney (U) test was employed. Traditional ratios used: Current ratio, Quick ratio, Interest coverage, and Operating income margin. Cash flow ratios used: Cash flow ratio, Critical needs cash coverage, Cash interest coverage, and Operating cash margin. |

a) When comparing the operating cash flow ratio and the critical needs ratio to the current ratios and quick ratios, substantial statistical disparities emerge. b) When comparing the ratios of interest coverage and operating margin to those of cash interest coverage and operating cash margin, there is no significant statistical variance. c) The utilization of traditional ratios, which combine current and quick ratios to evaluate a company's liquidity, can result in flawed decision-making on the part of investors. d) The use of cash flow ratios in liquidity analysis is notably more rigorous than traditional ratios. As a result, the quality of investment decisions is improved for investors. |

| (Atieh 2014) | Ιnvestigating the liquidity position of the Jordanian pharmaceutical sector using traditional ratios compared to cash flow ratios. | The research involved an examination of the financial ratios of both cash flow and traditional metrics for seven leading pharmaceutical businesses in Jordan. All of these companies were operating in the same industry, and their annual reports were the source of the data evaluated. This analysis was conducted over six years, from 2007 to 2012. | a) When comparing cash flow ratios and traditional ratios, such as the current ratio, notable disparities exist. b) It can be observed that there are no noteworthy distinctions between other ratios relating to cash flows and conventional ratios like cash interest coverage ratio and interest coverage ratio. c) Relying solely on conventional ratios to assess a company's liquidity can lead to erroneous conclusions. d) When evaluating a company's liquidity, cash flow ratios prove to be more productive measurements than traditional ratios. This is because cash flow ratios provide a more comprehensive understanding of the company's capacity to fulfill its obligations. |

| (Kirkham 2012) | Exploring the worth of scrutinizing a company's liquidity by comparing traditional ratios with cash flow ratios. | Over five-years, a study was conducted on twenty-five companies in the telecommunications sector to compare their traditional ratios and cash flow ratios. The Fin Analysis database provided the necessary data. The ratios analyzed included the current ratio, quick ratio, and interest coverage ratio, along with the cash flow ratio, critical needs cash coverage ratio, and cash interest coverage ratio. The primary objective of the comparative analysis was to identify and scrutinize trends and discrepancies between the traditional and cash flow ratios. | The study discovered that variances were present between the conventional liquidity ratios and the ratios concerning cash flow. If one were to base their conclusions solely on the traditional ratios, it could potentially result in an erroneous determination regarding the liquidity of various companies. In some cases, a company could be considered liquid despite facing issues with cash flow, or a company could be deemed illiquid even though it possessed adequate cash flow resources. |

| (Ryu and Jang 2004) | Investigating hotel and casino performance using cash flow ratios and traditional financial ratios. | The financial performance indicators that were used to measure liquidity, solvency, and operational efficiency consisted of five ratios. The study analyzed a period of five years, specifically from 1998 to 2002. To distinguish the variance in performance between two hotel segments, commercial and casino hotel companies, independent sample t-tests were conducted. | There are varying outcomes in liquidity when comparing the traditional ratio method to cash flow-based ratios. |

4. Discussion

The results of the review indicated that few case studies have been conducted, over more than twenty years, to compare traditional indicators and accepted cash flows, with statistical analysis methods, in predicting the future financial performance of products. This finding is consistent with recent research conducted by Bhandari Showers and Johnson-Snyder (2019), which emphasizes that most models for evaluating a company's financial situation rely on traditional numerical indicators rather than cash flows. Consequently, it is uncommon to find a comparison of both approaches using the same data set.

This systematic review used studies that compared traditional ratios with cash flow ratios. Economic indicators can vary; depending on the specific research question and the industry under investigation. For example, solvency ratios and profitability ratios were examined in a study conducted in the food industry sector(Rahman 2017). Other studies can include variables such as cash flows, historical data, and company-related events (Zhai and Zhang 2023). These case studies offer valuable insights into the impact of indicators on firm performance, with statistical analysis allowing researchers to identify significant predictors and quantify the strength and direction of relationships (Kundu, Tang, and Chatterjee 2019). However, it is worth noting that no comparisons between traditional ratios and cash flow ratios were included in the studies.

The findings of the review also reveal that both cash flow and traditional indicators could be used for forecasting (Barua and Saha 2015; Waqas and Md-Rus 2018). The forecasting of financial distress continues to be a crucial focus for researchers due to its significance for businesses and their stakeholders. These stakeholders include investors, lenders, and the general capital market. Financial distress is a costly occurrence that could result in the complete shutdown of a business. Financial distress models serve as helpful tools for business managers in such circumstances, enabling them to take corrective measures and potentially avoid bankruptcy (Waqas and Md-Rus 2018). A meta-analysis conducted by Adnan, Aziz, and Dar (2006) analyzed 98 financial distress forecasts and highlighted the importance of financial ratios, specifically profitability ratios, liquidity ratios, leverage ratios, and cash flow ratios, in predicting financial distress.

Another important finding of this paper is that a hybrid model of conventional and cash flow ratios displays superior efficacy in prediction compared to models that only utilize one type of ratio (Bhandari, Showers, and Johnson-Snyder 2019). Relying solely on traditional ratios when deciding a company's liquidity can often result in an erroneous evaluation, ultimately leading to faulty conclusions (Atieh 2014; Kirkham 2012).

The systematic review conducted has yielded noteworthy results. The findings reveal that cash flow indicators possess superior predictive potential compared to traditional indicators (Barua and Saha 2015; Bhandari, Showers, and Johnson-Snyder 2019). In a study conducted by Jooste (2007), it was discovered that cash flow ratios are capable of predicting financial distress, with the cash flow to total debt ratio being the most effective indicator of failure. Additionally, Fawzi, Kamaluddin, and Sanusi (2015) have affirmed that cash flow ratios can be relied upon as a dependable method for anticipating financial distress.

The review underscores the significance of cash flow ratios in providing an accurate assessment of a company's financial status. These ratios serve as a crucial warning system for potential financial difficulties and insolvency (Barua and Saha 2015). Additionally, cash flow ratios are indicative of a company's capacity to fulfill its obligations (Atieh 2014), thereby improving the quality of investor decision-making (Mavengere 2015). Porwal and Jain (2013) further argue that cash flow ratios overcome the limitations of traditional ratios by providing a more accurate representation of a company's true value, making them an invaluable aid to all stakeholders in their evaluation of a company's worth and in promoting meaningful corporate governance.

Business liquidity is often measured by various financial ratios. Previous studies (Agarwal and Taffler 2008; Yap, Yong, and Poon 2010) demonstrated that liquidity ratios play a significant role in forecasting financial difficulty. These studies argued that firms with higher liquidity are less prone to financial hardship. More recent studies (Arlov, Rankov, and Kotlica 2013; Biddle, Ma, and Song 2022; Jones and Peat 2014) have also emphasized the importance of cash flow ratios in predicting financial distress. These studies hypothesize that there is a negative correlation between cash flow and financial hardship.

The use of bankruptcy or risk prediction models based on cash flow ratios has not been extensively researched, but studies that have employed this method have proven the efficacy of forecasting with operating cash flows (Bellovary, Giacomino, and Akers 2007). Sharma and Iselin (2003) discovered strong evidence that the inclusion of cash flow data in credit-related measures enhances their predictive value when contrasted with traditional methods.

While identifying the factors that predict a firm's financial condition is crucial, it is equally important to select an appropriate statistical model to anticipate financial distress. Several statistical models have been presented in the literature for this purpose. Altman (1968) utilized the multiple discriminant analysis (MDA) technique to differentiate between healthy and unhealthy firms. Bauer & Agarwal (2014), on the other hand, utilized a probabilistic regression analysis to predict a firm's financial distress. Recursive partition analysis (decision tree), neural network model, and linear probability model are also commonly used to optimize company value (Pao 2008).

The utilization of conventional financial ratios in studies that assess the financial state of a set of companies can lead to a range of statistical issues that undermine the validity of the results obtained. This is because of the nature of the mathematical framework employed, which results in asymmetries in financial indicators. Linares-Mustarós et al. (2022) conducted a study advocating for a new analytical methodology that includes the use of Compositional Data (CoDa) for evaluating the financial reports of a given industry. This new methodology enhances the analysis of conventional indicators by enabling the application of statistical techniques without encountering significant drawbacks such as extreme prices.

The aim of this systematic review was limited to examining the contrast between traditional ratios and cash flow ratios, with the sole application of statistical analysis. Researchers seldom make use of nonlinear models to explore determinants in search of a superior predictive model. In a study by Pao (2008), multiple linear regression and artificial neural network (ANN) models were utilized, and it was concluded that ANN models produced better fitting and predictions compared to regression models. The connection between the debt ratio and the independent variables is not linear, as noted by Pao (2008).

Conducting a systematic review identifying studies comparing traditional and cash flow ratios to predict the future financial performance of firms can be a contribution to the literature, however, it comes with its own set of limitations and challenges. The literature that is published may initially contain bias, favoring studies that yield positive or noteworthy results and disregarding those that produce neutral or negative results. This tendency can result in an overestimation of the efficacy of the methods being scrutinized (Bartolucci and Hillegass 2010).

Also, when conducting a systematic review valuable information may be lost from studies that were never published or were not accessed, leading to an incomplete picture of the subject. Also, the studies reviewed may use different methodologies, sample sizes, and statistical techniques, making direct comparisons difficult. Differences in the methods used to calculate and analyze ratios could affect the results (Jahan et al. 2016).

Moreover, the effectiveness of the indicators may vary depending on the industry, economic conditions, and the specific context of the businesses being analyzed. A ratio that performs well in one industry may not perform as well in another, so generalizing the findings across different industries would not be correct (Jahan et al. 2016).

5. Conclusions

The results of the present systematic review highlight:

- a)

- Cash flow ratios have better predictive power than traditional ratios.

- b)

- A mixed model consisting of traditional ratios and cash flow ratios performs better in forecasting than individual models.

- c)

- Cash flow ratios possess the capacity to provide the most precise and comprehensive depiction of a company's financial standing. It can also serve as an indicator of potential financial difficulties and bankruptcy. Additionally, it can provide insight into a company's capability to meet its financial obligations, thereby improving the quality of investor decision-making

- d)

- A conclusion based solely on the traditional indicators could lead to a wrong decision about the liquidity of some companies.

Author Contributions

Conceptualization D.S.; methodology, D.S; D.B. and A.S.; software, D.S.; validation, D.S. and D.B.; formal analysis, D.S.; investigation, D.S.; resources, D.S; writing—original draft preparation, D.S.; writing—review and editing, D.S., D.B.., and A.S.; visualization, D.S.; project administration, D.S. Supervision: A.S. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Conflict of Interest

The authors declare no conflict of interest.

References

- Abualrob, Laith Abdel Rahman, and Sanaa N. Maswadeh. 2020. “The Effect of Financial Ratios Derived From Operating Cash Flows on Jordanian Commercial Banks Earnings per Share.” International Journal of Financial Research 11 (1): 394–404. https://ideas.repec.org//a/jfr/ijfr11/v11y2020i1p394-404.html. [CrossRef]

- Adnan Aziz, M., and Humayon A. Dar. 2006. “Predicting Corporate Bankruptcy: Where We Stand?” Corporate Governance: The International Journal of Business in Society 6 (1): 18–33. [CrossRef]

- Agarwal, Vineet, and Richard Taffler. 2008. “Comparing the Performance of Market-Based and Accounting-Based Bankruptcy Prediction Models.” Journal of Banking & Finance 32 (8): 1541–51. [CrossRef]

- Altman, Edward I. 1968. “Financial Ratios, Discriminant Analysis and the Prediction of Corporate Bankruptcy.” The Journal of Finance 23 (4): 589–609. [CrossRef]

- Arlov, OGNJAN, SINISA Rankov, and SLOBODAN Kotlica. 2013. “Cash Flow in Predicting Financial Distress and Bankruptcy.” Advances in Environmental Science and Energy Planning 42 (2/3): 421–41.

- Atieh, Sulayman H. 2014. “Liquidity Analysis Using Cash Flow Ratios as Compared to Traditional Ratios in the Pharmaceutical Sector in Jordan.” International Journal of Financial Research 5 (3): 146–58. https://ideas.repec.org/a/jfr/ijfr11/v5y2014i3p146-158.html. [CrossRef]

- Bartolucci, Alfred A., and William B. Hillegass. 2010. “Overview, Strengths, and Limitations of Systematic Reviews and Meta-Analyses.” In, edited by Francesco Chiappelli, 17–33. Berlin, Heidelberg: Springer Berlin Heidelberg. [CrossRef]

- Barua, Suborna, and Anup Kumar Saha. 2015. “Traditional Ratios vs. Cash Flow Based Ratios: Which One Is Better Performance Indicator?” Advances in Economics and Business 3 (6): 232–51. [CrossRef]

- Bauer, Julian, and Vineet Agarwal. 2014. “Are Hazard Models Superior to Traditional Bankruptcy Prediction Approaches? A Comprehensive Test.” Journal of Banking & Finance 40 (March): 432–42. [CrossRef]

- Bellovary, Jodi L., Don E. Giacomino, and Michael D. Akers. 2007. “A Review of Bankruptcy Prediction Studies: 1930 to Present.” Journal of Financial Education 33: 1–42. https://www.jstor.org/stable/41948574.

- Bhandari, Shyam, Vince Showers, and Anna J. Johnson-Snyder. 2019. “A Comparison: Accrual Versus Cash Flow Based Financial Measures’ Performance in Predicting Business Failure.” Journal of Accounting and Finance 19 (6). [CrossRef]

- Biddle, Gary C, Mary LZ Ma, and Frank M Song. 2022. “Accounting Conservatism and Bankruptcy Risk.” Journal of Accounting, Auditing & Finance 37 (2): 295–323. [CrossRef]

- DAHIYAT, Ahmad Abdelrahim, Sulaiman Raji WESHAH, and Mohammad ALDAHIYAT. 2021. “Liquidity and Solvency Management and Its Impact on Financial Performance: Empirical Evidence from Jordan.” The Journal of Asian Finance, Economics and Business 8 (5): 135–41. [CrossRef]

- Fawzi, Noor Salfizan, Amrizah Kamaluddin, and Zuraidah Mohd Sanusi. 2015. “Monitoring Distressed Companies through Cash Flow Analysis.” Procedia Economics and Finance, 7th INTERNATIONAL CONFERENCE ON FINANCIAL CRIMINOLOGY 2015, 7th ICFC 2015, 13-14 April 2015,Wadham College, Oxford University, United Kingdom, 28 (January): 136–44. [CrossRef]

- Jahan, Nusrat, Sadiq Naveed, Muhammad Zeshan, and Muhammad A Tahir. 2016. “How to Conduct a Systematic Review: A Narrative Literature Review.” Cureus 8 (11). [CrossRef]

- Jones, Stewart, and Maurice Peat. 2014. “Predicting Corporate Bankruptcy Risk in Australia: A Latent Class Analysis.” Journal of Applied Management Accounting Research 12 (1): 13.

- Jooste, Leonie. 2007. “An Evaluation of the Usefulness of Cash Flow Ratios to Predict Financial Distress.” Acta Commercii 7 (1): 1–13. [CrossRef]

- Kirkham, Ross1, rkirkham@usc.edu.au. 2012. “Liquidity Analysis Using Cash Flow Ratios and Traditional Ratios: The Telecommunications Sector in Australia.” Journal of New Business Ideas & Trends 10 (1): 1–13. http://search.ebscohost.com/login.aspx?direct=true&db=ofs&AN=78172370&site=ehost-live.

- Kundu, Prosenjit, Runlong Tang, and Nilanjan Chatterjee. 2019. “Generalized Meta-Analysis for Multiple Regression Models across Studies with Disparate Covariate Information.” Biometrika 106 (3): 567–85. [CrossRef]

- Linares-Mustarós, Salvador, Maria Àngels Farreras-Noguer, Núria Arimany-Serrat, and Germà Coenders. 2022. “New Financial Ratios Based on the Compositional Data Methodology.” Axioms 11 (12): 694. [CrossRef]

- Mavengere, Kudakwashe. 2015. “Liquidity Analysis of Zimbabwe Stock Exchange (ZSE) Listed Retail Companies Using Traditional Ratios and Cash Flow Ratios.” International Journal of Management Sciences and Business Research 4 (7).

- Mills, John, and Jeanne H. Yamamura. 1998. “The Power of Cash Flow Ratios.” Journal of Accountancy; New York 186 (4): 53,55+. http://search.proquest.com/docview/206784897/abstract/7CED98DB61B64DA6PQ/1.

- Page, Matthew J, Joanne E McKenzie, Patrick M Bossuyt, Isabelle Boutron, Tammy C Hoffmann, Cynthia D Mulrow, Larissa Shamseer, Jennifer M Tetzlaff, Elie A Akl, and Sue E Brennan. 2021. “The PRISMA 2020 Statement: An Updated Guideline for Reporting Systematic Reviews.” International Journal of Surgery 88: 105906.

- Pao, Hsiao-Tien. 2008. “A Comparison of Neural Network and Multiple Regression Analysis in Modeling Capital Structure.” Expert Systems with Applications 35 (3): 720–27. [CrossRef]

- Porwal, Hamendra Kumar, and Shashank Jain. 2013. “Cash Flow Ratios to Predict Investment’s Soundness.” Asia-Pacific Finance and Accounting Review 1 (4): 55.

- Rahman, Abdul Aziz A Abdul. 2017. “The Relationship between Solvency Ratios and Profitability Ratios: Analytical Study in Food Industrial Companies Listed in Amman Bursa.” International Journal of Economics and Financial Issues 7 (2): 86–93.

- Ryu, Kisang, and Shawn Jang. 2004. “Performance Measurement Through Cash Flow Ratios and Traditional Ratios: A Comparison of Commercial and Casino Hotel Companies.” The Journal of Hospitality Financial Management 12 (1): 15–25. [CrossRef]

- Sharma, Divesh S, and Errol R Iselin. 2003. “The Relative Relevance of Cash Flow and Accrual Information for Solvency Assessments: A Multi-Method Approach.” Journal of Business Finance & Accounting 30 (7-8): 1115–40. [CrossRef]

- Waqas, Hamid, and Rohani Md-Rus. 2018. “Predicting Financial Distress: Importance of Accounting and Firm-Specific Market Variables for Pakistan’s Listed Firms.” Edited by Mohammed M Elgammal. Cogent Economics & Finance 6 (1): 1545739. [CrossRef]

- Yap, Ben Chin-Fook, David Gun-Fie Yong, and Wai-Ching Poon. 2010. “How Well Do Financial Ratios and Multiple Discriminant Analysis Predict Company Failures in Malaysia.” International Research Journal of Finance and Economics 54 (13): 166–75.

- Zhai, Shuang, and Zhu Zhang. 2023. “Read the News, Not the Books: Forecasting Firms’ Long-Term Financial Performance via Deep Text Mining.” ACM Transactions on Management Information Systems 14 (1): 1–37.

Figure 1.

Flowchart of the process followed to identify the articles included in the systematic review (Page et al. 2021)

Figure 1.

Flowchart of the process followed to identify the articles included in the systematic review (Page et al. 2021)

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.