Submitted:

21 October 2023

Posted:

23 October 2023

You are already at the latest version

Abstract

This article explores the relationship between green energy and cryptocurrencies in the sustainable energy finance sector. The research findings contribute to our understanding of the application of green economy practice, enabling investors in financial markets, policymakers, and stakeholders to make informed decisions and develop specific strategies. Adopting the green economy paradigm makes it possible to promote collaboration and innovation by integrating ethical and responsible principles that can improve the overall quality of processes and boost sustainable growth. Cryptocurrencies have been widely used as financial instruments over the last decade. Given the development of the cryptocurrency market and the growing awareness of greener and more energy-efficient tokens, the green economy has become a popular topic for understanding economic and political issues. However, the literature still lacks clear evidence on how cryptocurrencies interact with green energies. Therefore, this study examines the long- and short-term relationships between dirty cryptocurrencies such as Bitcoin (BTC), Ethereum (ETH), clean cryptocurrencies such as Cardano (ADA), Ripple (XRP), Stellar (XLM), and green energies such as ISE Clean Edge Global Wind Energy, S&P Global Clean Energy, S&P TSX Renewable Energy and Clean Technology, Solactive China Clean Energy, in the period from January 2020 to September 2023. The results show that diversification is key, with clean cryptocurrencies such as ADA, XLM and XRP offering diversification opportunities alongside "dirty" cryptocurrencies such as BTC and ETH. Although sustainable energy indices show mixed evidence in the long and short term, they remain relevant for those who focus on clean energy investments. It is also becoming increasingly relevant for investors in sustainable portfolios to assess their environmental impact, especially for energy-intensive cryptocurrencies, and it is advisable to explore sustainable blockchain technologies.

Keywords:

green economy

; sustainability

; cryptocurrency

; safe haven

; connectivity

1. Introduction

The vitality of energy and its sustainable advancement are imperative for the continuity of human civilisation. Energy is a vital and irreplaceable commodity that drives economic and social progress. However, existing energy reservoirs are inadequate to satisfy the growing appetite for energy in line with current technological standards. The extensive use of these resources has left an immense ecological footprint, contributing to issues such as global warming and environmental contamination. As a result, preserving resources and safeguarding the environment have gained unanimous support around the world, with sustainable energy development emerging as a common goal (Imbulana Arachchi and Managi 2021).

Sustainable energy refers to the practice of using energy in a way that meets current needs without reducing the ability of later generations to keep up with their demands. The future of energy systems is currently driven by three main trends: electrification, decarbonisation, and digitalisation. The widespread application of digital technology (DT) around the world has triggered the fourth industrial revolution and has been identified as a major driver of the economy’s business model (Xu et al. 2018,Banales 2020,Rotatori et al. 2021).

In recent years, the world has witnessed a dramatic increase in environmental risks, and one of the main drivers of this alarming trend is the rapid rise in carbon emissions. This growing environmental crisis poses a significant threat to ecosystems, human health and well-being in general (Zhang and Da 2015,Wang and Yang 2020).

In the absence of substantial reductions in carbon emissions, the 21st century is about to witness a temperature rise of almost 2 degrees Celsius. The latest report from the Intergovernmental Panel on Climate Change (IPCC), released in August 2021, emphasises the unprecedented importance of carbon dioxide (CO2) levels, a critical aspect not seen in hundreds of years. The excessive use of fossil fuels is responsible for increasing global CO2 emissions, leading to high temperatures and environmental deterioration. To tackle this crisis, the replacement of fossil fuels with emerging "clean" or "green" energy sources is an urgent necessity (Jardón et al. 2017,Dong et al. 2018,Olivera and Segarra 2021).

The emergence of the new green economy represents a significant and promising manifestation of sustainable development. This concept incorporates a harmonious synergy between economic growth, environmental protection and social welfare (Wang et al. 2021). This data is taken into account by investors, policymakers, state bodies, international organisations and researchers (Danino-Perraud 2020).

In recent years, growing environmental concerns have intensified the urgency of shifting towards a greener and more sustainable economy. Numerous organisations and nations have embarked on a worldwide redefinition, presenting a potential catalyst for profound transformations driven by sustainability (Wang and Yang 2020,Jardón et al. 2017,Xiong et al. 2022). In 2015, the European Commission developed the first Green Economy Action Plan to encourage Europe’s transition to sustainability (Santos et al. 2023). The United Nations therefore unveiled the Sustainable Development Goals (SDGs) as a response to this global issue. These 17 initiatives, set to be accomplished by 2030, encompass the expansion of renewable energy sources. Proactive nations are implementing support policies aimed at promoting innovation. For example, the United States has allocated an annual investment of 1.3 trillion dollars to the green economy, resulting in the creation of 9.5 million full-time jobs (Georgeson and Maslin 2019). The European Union has embarked on a bold and ambitious journey with the "Green Deal", a visionary plan outlined by the European Commission in 2022. The aim is to achieve carbon neutrality by the year 2050. This commitment represents a significant milestone in the global effort to combat climate change, setting a compelling example for nations around the world. However, this mission is not exclusive to the EU. As the world’s leading emitters of greenhouse gases (GHG), Asian countries are under increasing pressure to make the transition to a greener economy. The urgency of tackling climate change is a universal concern that transcends borders and continents. Asian nations, with their booming economies and rapidly growing populations, play a key role in defining the future trajectory of the planet’s environmental sustainability (Fekete et al. 2021).

Although there have been notable advances in the deployment of renewable energies over the last decade, numerous reports highlight a worrying reality: progress, as it stands, is insufficient to fulfil the SDGs and the objectives of the Paris Agreement. Achieving significant decarbonisation of the energy sector, which is key to tackling climate change, remains a challenge (Giglio et al. 2023). We have seen a number of national and global factors complicate the search for sustainable energy solutions. However, companies and investors are increasingly recognising that green investments not only align with social and environmental values but also offer the potential for superior financial returns. This realisation underlines the economic viability of sustainability initiatives (Baruník and Křehlík 2018,Arif et al. 2021,Sharma et al. 2022).

The search for financing instruments aligned with the SDGs is a crucial step towards promoting sustainability in various sectors of the economy. However, despite the growing interest in sustainable finance, there is a notable gap in research and understanding when it comes to evaluating the performance of green assets. This knowledge deficit poses challenges for investors and policymakers alike as they seek to make informed decisions that align with environmental and social objectives. A significant issue lies in the lack of standardised metrics and methodologies for assessing the performance of green assets. Traditional financial metrics are often insufficient when it comes to capturing the wider impact of sustainability investments. As a result, investors can struggle to accurately assess the environmental and social outcomes of their portfolios, making it difficult to allocate capital effectively to projects that support the SDGs. The green economic model aims to reconcile the goals of prosperity with carbon-neutral, efficient and sustainable development by utilising the potential brought by technology and innovation (Silva et al. 2021).

In the field of cryptocurrencies, the emergence of sustainable or green cryptocurrencies represents a new attempt to address the energy consumption concerns associated with conventional cryptocurrencies such as Bitcoin. These greener alternatives aim to use more energy-efficient consensus mechanisms or rely on renewable energy sources to power their networks (Gundaboina et al. 2022,Haq 2022,Bejan et al. 2023,Putri et al. 2021).

The rapid evolution of cryptocurrencies has led to an increase in demand. However, cryptocurrencies that use Proof of Work (PoW), such as Bitcoin (BTC) and Ethereum (ETH), are seen as "dirty" due to their high energy consumption. Furthermore, cryptocurrencies with PoW mechanisms have no plans to transition to more energy-efficient consensus mechanisms. On the other hand, cryptocurrencies that use PoS or other energy-efficient consensus mechanisms are often considered "clean" in terms of electricity consumption, for example, Cardano (ADA), Ripple (XRP), and Stellar (XLM). In addition, some cryptocurrency projects and organisations are actively working to offset or reduce their carbon footprint by investing in renewable energy sources, carbon credits or other sustainability measures. These efforts can help improve a cryptocurrency’s environmental image. In summary, cryptocurrencies can be categorised as "dirty" or "clean" based on their electricity consumption, with PoW-based cryptocurrencies generally considered less environmentally friendly compared to those that use more energy-efficient mechanisms, such as PoS. However, it is crucial to consider the wider context and the cryptocurrency industry’s ongoing efforts to address environmental concerns (O’Dwyert and Malone 2014,Ghosh and Bouri 2022,Merza 2023,Polemis and Tsionas 2023,Sarkodie et al. 2023).

With regard to studies and bearing in mind the existing literature, we believe that most empirical studies have so far failed to analyse the impact of shocks on green markets and cryptocurrencies. We believe that a good understanding of these relationships is essential for policymakers and environmental investors to be able to adjust investment portfolios and develop good hedging strategies. There is a need to better understand the interactions between different financial markets in order to better manage market turbulence. In this sense, cryptocurrencies have played a hedging role. This is why this study examines the bidirectional connectivity between dirty cryptocurrencies such as Bitcoin (BTC) and Ethereum (ETH), clean cryptocurrencies such as Cardano (ADA), Ripple (XRP) and Stellar (XLM), and sustainable energies such as ISE Clean Edge Global Wind Energy, S&P Global Clean Energy, S&P TSX Renewable Energy and Clean Technology and Solactive China Clean Energy, from January 2020 to September 2023.

This paper contributes to the existing literature in different ways. Firstly, our study provides solid evidence of the relationship between cryptocurrencies and the green economy in regional markets such as the S&P TSX Renewable (Canada), Solactive China Clean Energy (China), S&P Global Clean (USA), and finally the ISE Clean Edge Global Wind Energy, also from the United States. Green economy market indices are designed to capture the performance of companies committed to a sustainable business model and are also useful for analysing the performance of green stock indices in the above-mentioned regions. They therefore allow us to examine the short- and long-term impact of cryptocurrencies on a given country’s green stock indices. Secondly, our study extends related research by measuring the herd behaviour of "black/dirty" versus "green/clean" cryptocurrencies, as suggested by recent studies by Ren and Lucey (2022a, 2022b). It is therefore a pioneering study, as far as we are aware, to empirically examine the safe harbour properties of a wide range of green energy indices. The study also analyses two types of cryptocurrencies in times of extreme instability and market turbulence. It is thus possible to indicate to investors when a particular type of green energy stock is shown to act as a safe harbour or a hedge against one or the other, or vice versa. It is possible to manage cryptocurrency declines with the help of green energy stocks or vice versa. In fact, everything depends on the currency. Therefore, any economic investment programme in green energy will conflict with the argument if only "dirty" currencies are used as a hedge or safe haven against green energy.

2. Literature Review

In recent years, there has been a notable increase in the global green energy market, driven by the imperative to combat climate change and the transition to sustainable energy sources. Renewable energy technologies such as solar, wind and hydroelectric power have gained substantial traction, with several countries setting ambitious targets for their adoption. However, in the midst of this transformative shift towards clean energy, there is a relatively unexplored but crucial link between cryptocurrencies and green energy markets. The convergence of the cryptocurrency and green energy markets presents a unique and multifaceted scenario that deserves closer examination.

Numerous studies have begun by examining these crypto assets from various perspectives: their role as hedges and safe havens. Bouri et al. (2018) studied the return spillovers and volatility between BTC and four asset classes (stocks, commodities, currencies, and bonds) in bearish and bullish market conditions. The authors find significant evidence that Bitcoin is connected to most of the assets under study, particularly commodities, therefore showing that Bitcoin is not completely isolated. We also verified the existence of several studies that evaluated the connectivity between cryptocurrencies with different assets during the COVID-19 crisis (Kakinuma 2022) and the diversification of traditional assets (Klein et al. 2018,Shahzad et al. 2019), and market efficiency and long-term memory (Dias et al. 2023,Dias et al. 2022).

Over the last decade, the financial landscape has witnessed a transformative change with the emergence of clean energy stock indices. These indices have revolutionised the way investors monitor and evaluate the performance of listed companies in the clean energy sector. They have become valuable tools for portfolio management, offering valuable information on the growth and potential of clean energy investments. The authors Gao et al. (2023) evaluated green assets from the perspective of a new environmental protection tool, green bonds have gained prominence, causing a shock in various markets, but also have a certain hedging role. Based on the relationship between the three green investment instruments (S&P green Bond, China Green Bond, and Climate Bond), the authors demonstrate a guiding significance for investors interested in environmental protection in asset allocation and hedge selection. Similarly, Lorente et al. (2023) investigated the connection between the climate change index, green financial assets, renewable energy markets and the geopolitical risk index. The authors show that the highest total connectivity index (TCI) decreases after the second wave of COVID-19 and increases during the first 100 days of the Russia-Ukraine conflict. In addition, the results show that geopolitical risk (GPR) is a net transmitter of the climate change index during the Russian invasion of Ukraine.

While previous research has often focused on the relationship between cryptocurrencies and traditional energy assets, a broader perspective is adopted by Jiang et al. (2022). Their study explores the role of various assets, including Bitcoin, gold, stocks, currencies, and energy commodities such as crude oil and natural gas, within the global network of volatility connections. Their findings shed light on the dynamic nature of asset interconnections, revealing that Bitcoin, gold, foreign exchange, and natural gas serve as volatility transmitters, signifying their impact on the transmission of market volatility. Understanding the intricate relationship between clean energy stock indices, cryptocurrencies and various other assets provides valuable information for investors looking to diversify their portfolios and capitalise on emerging opportunities. As noted by the authors Dias et al. (2023) who show that clean energy stock indices can offer a viable safe harbour for dirty energy cryptocurrencies. However, the precise associations differ depending on the cryptocurrency being analysed. The implications of the results of this study are significant for investment strategies, and this knowledge can inform decision-making procedures and facilitate the adoption of sustainable investment practices.

2.1. Related Studies

Several studies have explored the potential of clean energy as a safe harbour for dirty energy. Clean energy stocks represent a relatively new asset class to invest in and these assets can be very volatile. Given the recent evolution of green bonds as a hedging tool in the face of climate change and green energy transitions, as well as the popularity of cryptocurrencies as a portfolio diversifier, previous literature could focus on the potential impacts of environmental concerns in conjunction with cryptocurrencies on the performance of green financial assets. examined crude oil, US bonds, gold, VIX, OVX, and European carbon prices that can be used to hedge a clean energy investment. The results suggest that the VIX is the best hedging asset for clean energy stock indices, followed by crude oil and OVX. Author Kuang (2021) investigates whether diversification into clean energy stocks or green bonds could reduce portfolio downside risk for investors holding dirty energy stocks or international stock indices. The results show that both green bonds and clean energy stocks provide risk diversification benefits for investors holding dirty energy stocks. However, green bonds reduce risk, while clean energy stocks generally increase the risk of the international stock index portfolio.

In 2022, authors Ren and Lucey (2022a) investigated the hedging and safe-haven properties of a wide range of clean energy indices in relation to two distinct types of cryptocurrencies based on their energy consumption levels, labelled "dirty" and "clean". The results show a weak link between clean energy and cryptocurrencies, which implies the potential use of clean energy as a hedging and diversification tool for cryptocurrencies in the future. In a complementary way, Angelini et al. (2022) explored the dependence between sustainable energy, oil and Bitcoin between 2011 and 2019, showing the existence of spillovers influencing both the clean energy sector and oil prices. However, the authors show that the connectivity between clean energy and Bitcoin may have some characteristics of a possible substitution effect. In the same line of research, the authors Ozdurak et al. (2022) analysed the safe haven characteristics of Bitcoin (BTC) and Ethereum (ETH), in relation to the S&P Global Clean Energy (SPGCE) and Global Information Technology (MSCIWIT) indices. The authors show that digital currencies have weak hedging and safe harbour characteristics, which could jeopardise the rebalancing of sustainable portfolios by green investors. Kamal and Hassan (2022) analysed the impact of the cryptocurrency environmental index (CEI) on clean energy stocks and green bonds, showing that the CEI exerts positive effects on S&P500 stocks in bearish market conditions and on water stocks in normal to optimistic market conditions. Interestingly, clean energy stocks and green bonds have an insignificant relationship with ICEA.

In more recent studies, Arfaoui et al. (2023) examined the dependence on clean energy, green markets and cryptocurrencies, and showed that sustainable investments, especially the DJSI and ESGL indices, play a key role in the network system during the COVID-19 pandemic. The authors concluded that green bonds are the least integrated with other financial markets, suggesting their significant role in providing diversification benefits to investors. Sharif et al. (2023) studied the connectivity between green economy indices, dirty cryptocurrencies and clean cryptocurrencies in the US, European and Asian markets during the years 2017 to 2022. The authors show strong links between sustainable indices and clean cryptocurrencies compared to dirty cryptocurrencies, suggesting that green investors should not incorporate cryptocurrencies into their sustainable portfolios as safe haven assets. In a complementary way, the authors Naeem et al. (2023) investigated the dependence between cryptocurrencies and the sustainable energy market in the years 2018 to 2021. The authors found that clean alternative markets (SPGCE, ELEVHC & WILCE) and the ETH are net transmitters of risk to other markets and net contributors throughout the system. They also demonstrated how the SPGCE is essential for linking the various parts of the networks and provided convincing evidence of the time-varying dependency within the system, which calls into question the safe harbour properties when sustainable investors want to adjust the risk of their green portfolios. Anwer et al. (2023) studied the dynamic disturbances between digital assets and environmentally sustainable assets. The results suggest that environmentally sustainable indices and cryptocurrency indices show that there is commotion during the 2020 pandemic. However, in normal times, they remain mostly separate from each other. Therefore, it can be argued that both asset classes can serve as a hedge against each other. The findings have important implications for the investment industry and regulators, with a strong incentive for the green economy.

Bearing in mind the existing literature this study focuses on the importance of investigating whether clean energy indices can act as a hedge or safe harbour in comparison to cryptocurrencies classified as "dirty" and "clean". This research is motivated by concerns about the environmental impact of energy-consuming cryptocurrencies and the growing interest in sustainable investments. Investors want to understand whether clean energy stocks can help manage risks and promote sustainability. By analysing the relationships between clean energy stocks in various geographies, and energy-intensive cryptocurrencies, the researchers aim to determine whether clean energy stocks can provide protection or stability during periods of uncertainty in the global economy.

3. Methods and Data

The digital currencies used in the study are dirty cryptocurrencies such as Bitcoin (BTC) and Ethereum (ETH), clean cryptocurrencies such as Cardano (ADA), Ripple (XRP), Stellar (XLM), and green energies such as ISE Clean Edge Global Wind Energy, S&P Global Clean Energy, S&P TSX Renewable Energy and Clean Technology, Solactive China Clean Energy, in the period from January 2020 to September 2023.

The data used in the study covers the period from 2 January 2020 to 30 September 2023, and was obtained from the Thomson Reuters Eikon database. All prices in the study are quoted in local currency to mitigate exchange rate distortions, thus ensuring a consistent comparison between the different assets and indices.

To analyse the behaviour of dirty and clean cryptocurrencies, as well as regional sustainable energy indices, we will transform the original prices into logarithms of first differences. This transformation allows for more efficient analytical treatment, namely because the time data has homoscedastic characteristics instead of heteroscedasticity. For a better understanding, we will use the following equation:

where is the rate of return on day t, and and are the closing prices of the series at times t and , respectively.

This research will be carried out in different stages. Firstly, to characterise the sample, we will use the main measures of descriptive statistics and the Jarque and Bera (1980) adherence test, which postulates the normality of the data. In order to validate the assumption of stationarity of the time series, we will use the Breitung (2000) panel unit root test, a statistical test used in econometrics to assess whether time series data collected from multiple cross-sectional units has a unit root.

A unit root implies that a time series variable has a stochastic trend and is not stationary, which can complicate data analysis and lead to spurious regression results. To estimate structural breaks, the Clemente et al. (1998) test will be used, which allows the most significant crash to be identified, as well as the year of its occurrence. A structural break implies a significant change in the level and/or trend of a time series, which can be permanent or temporary. The methodology of Gregory and Hansen (1996) will be used to verify long-term connectivity.

This test is commonly used in the context of unit root tests and in analysing long-term links, in practical terms, this methodology is based on the likelihood ratio. The test statistic follows a specific distribution, usually a chi-squared distribution, under the null hypothesis. To check short-term connectivity, we will estimate the SVAR model. The SVAR model is an extension of the Vector Autoregressive (VAR) model, which tests a system of multiple time series variables that are modelled simultaneously in a system of linear equations. Each variable in the system is expressed as a linear combination of its own lagged values and the lagged values of all the other variables in the system. In addition, we use Cholesky decomposition, a popular method in which the order of the variables in the SVAR model is assumed to represent a causal hierarchy and the shocks are ordered according to.

4. Results

4.1. Descriptive Statistics

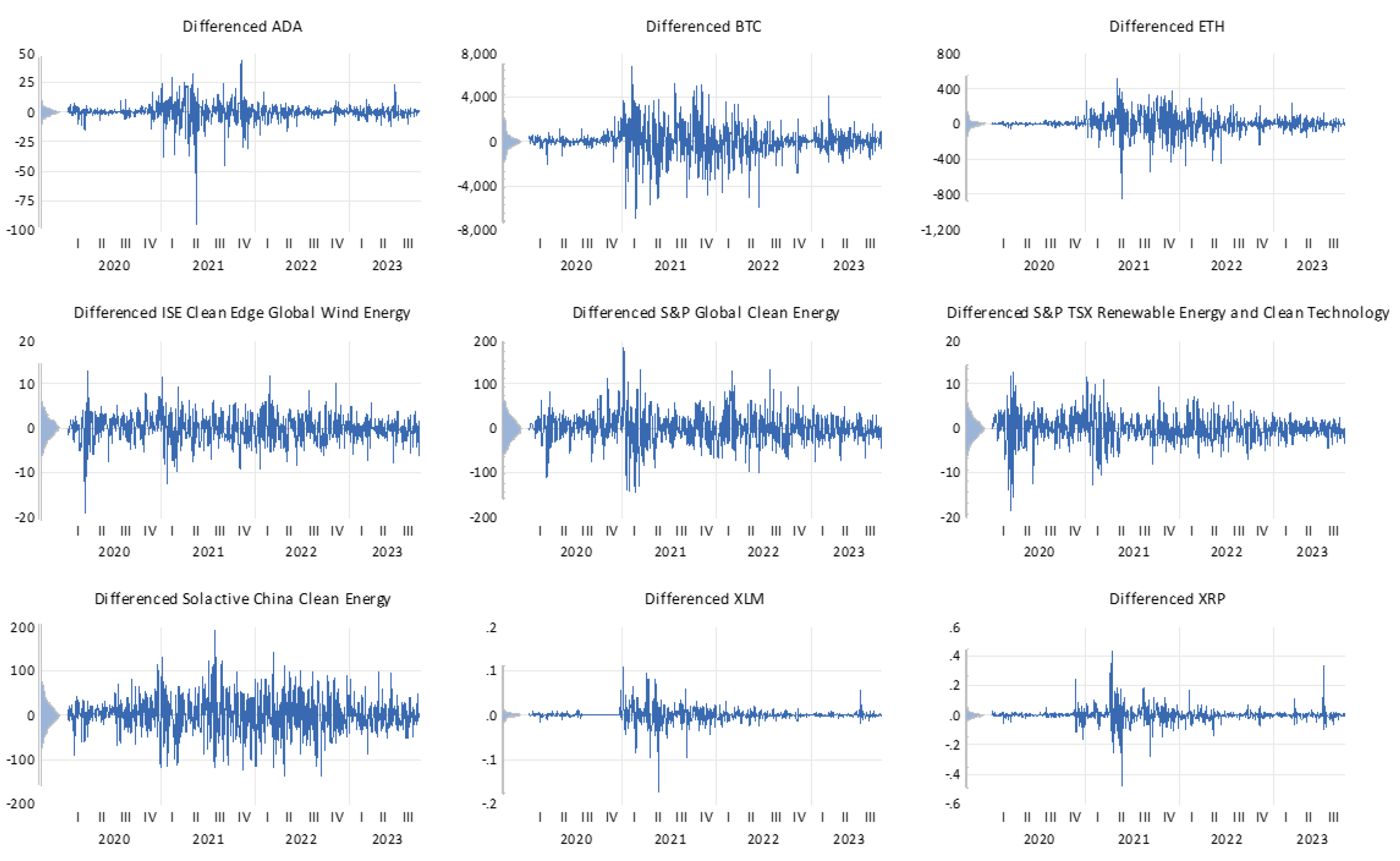

Figure 1 shows the evolution, in first differences, of dirty cryptocurrencies such as Bitcoin (BTC) and Ethereum (ETH), clean cryptocurrencies such as Cardano (ADA), Ripple (XRP), Stellar (XLM), and green energies such as ISE Clean Edge Global Wind Energy, S&P Global Clean Energy, S&P TSX Renewable Energy and Clean Technology, Solactive China Clean Energy, from January 2020 to September 2023. With regard to digital currencies, we can see extreme volatility from 2021 onwards. BTC reached an all-time high above $60,000 in April 2021, driven by increased institutional interest and growing acceptance among major financial institutions. Along with Bitcoin, many alternative cryptocurrencies have seen substantial price increases, namely Ethereum (ETH), Cardano (ADA), Ripple (XRP), and Stellar (XLM). With regard to sustainable energies, there was marked volatility from the first few months of 2020 onwards, which also increased in 2021. In 2022 there is a relative decrease in volatility, which we associate with clean energy systems being less susceptible to geopolitical turbulence.

Table 1 and Table 2 summarise the main measures of descriptive statistics, in daily returns, of the time series, referring to the cryptocurrencies Bitcoin (BTC), Ethereum (ETH), Cardano (ADA), Ripple (XRP), Stellar (XLM), and green energies such as ISE Clean Edge Global Wind Energy, S&P Global Clean Energy, S&P TSX Renewable Energy and Clean Technology, Solactive China Clean Energy, from January 2020 to September 2023.

Table 1 shows the summary statistics for the time data of the cryptocurrencies and shows that the average returns are positive, while the digital currency with the highest standard deviation is ETH (0.002610), i.e., a greater dispersion in relation to the average. When we evaluate the asymmetries, we realise that ADA, BTC and ETH have negative asymmetries (-0.962139, -0.679045, -0.661853, respectively), while XLM and XRP have positive asymmetries, but different from zero (reference value). In addition, we realise that all cryptocurrencies have values different from 3, such as ADA (9.719497), BTC (9.499837), ETH (10.65963), XLM (17.79364), XRP (19.44905). To corroborate the results, the Jarque and Bera (1980) test also shows the rejection of at a significance level of 1%. These results were to be expected due to the presence of fat tails, i.e., extreme values, resulting from uncertainty in the global economy.

Table 2 shows the summary statistics for the time data of sustainable energies, such as ISE Clean Edge Global Wind Energy, S&P Global Clean Energy, S&P TSX Renewable Energy and Clean Technology, and Solactive China Clean Energy, from January 2020 to September 2023. In terms of average returns, ISE CLEAN (-7.41E-05) and S&P TSX RENEWABLE ENERGY (-0.000391) have negative values, while the others have positive averages. With regard to the highest dispersion around the average, we see that S&P GLOBAL CLEAN (0.020064) has the highest value. With regard to asymmetry, the reference value is zero and we see that the energy indices have negative values, ISE CLEAN (-0.660691), S&P GLOBAL CLEAN (-0.380926), S&P TSX RENEWABLE ENERGY (-0.846904), SOLACTIVE CHINA CLEAN ENERGY (-0.097354). The shortness measures also show values other than 3, namely the S&P TSX RENEWABLE ENERGY (13.55373), ISE CLEAN (12.64018), S&P GLOBAL CLEAN (8.237000), SOLACTIVE CHINA CLEAN ENERGY (4.533476) indices. For validation, we also carried out the Jarque and Bera (1980) in which we verified that H0 was rejected at a significance level of 1%.

4.2. Time Series Stationarity

In order to validate the assumption of stationarity, we analysed the time data of sustainable energies, such as ISE Clean Edge Global Wind Energy, S&P Global Clean Energy, S&P TSX Renewable Energy and Clean Technology, Solactive China Clean Energy, as well as the cryptocurrencies Bitcoin (BTC), Ethereum (ETH), Cardano (ADA), Ripple (XRP), Stellar (XLM), from January 2020 to September 2023. To validate this assumption, we applied the Breitung (2000) panel unit root test (Table 3), in which we realised that the closing prices have unit roots. To this end, we carried out the logarithmic transformation in first differences, and this allows us to prove the rejection of the null hypothesis, and the confirmation of homoscedasticity in the time series, a basic assumption for the SVAR.

Unit Root Test with Structure Break

Table 4 shows the results of the Clemente et al. (1998) unit root test with structural breaks, applied to sustainable energy indices such as the ISE Clean Edge Global Wind Energy, S&P Global Clean Energy, S&P TSX Renewable Energy and Clean Technology, Solactive China Clean Energy, as well as the cryptocurrencies Bitcoin (BTC), Ethereum (ETH), Cardano (ADA), Ripple (XRP), Stellar (XLM), from January 2020 to September 2023.

As far as digital currencies are concerned, we can see a trend of crashes in 2021. Bitcoin, the most popular and valuable cryptocurrency, suffered a crash on 23 February 2021. The price of Bitcoin fell dramatically in a short period of time. Ripple’s XRP cryptocurrency also faced a significant drop on 13 April 2021. This event was significant because it was closely related to legal issues and regulatory challenges faced by Ripple Labs, the company behind XRP. The US Securities and Exchange Commission (SEC) filed a lawsuit against Ripple Labs, claiming that XRP was an unregistered security. Similarly, Cardano (ADA), Ethereum (ETH), and Stellar Lumens (XLM), suffered crashes on 19 May 2021. These cryptocurrencies are known for their smart contract capabilities and have many followers in the crypto community. This day’s falls were part of a wider market correction that affected many cryptocurrencies.

Energy indices such as the ISE Clean Edge Global Wind Energy, S&P Global Clean Energy, S&P TSX Renewable Energy and Clean Technology, Solactive China Clean Energy, mostly show sharp falls in 2021. ISE Clean Edge Global Wind Energy focuses on companies involved in the wind energy sector. The drop on 12 March 2020 can be attributed to the wider turmoil in the financial markets caused by the onset of the COVID-19 pandemic. The S&P Global Clean Energy Index, which includes companies from around the world involved in clean energy and renewable technologies, suffered a significant drop on 7 January 2021. This event may have been influenced by several factors: concerns about overvaluation in the clean energy sector and changes in investor sentiment at the start of the new year. The S&P TSX Renewable Energy and Clean Technology Index is specific to Canadian clean energy and renewable technology companies. Its breakdown on 8 February 2021 could be linked to regional economic factors, changes in government policies or market sentiment towards the clean energy sector in Canada. The Solactive China Clean Energy index tracks the performance of clean energy companies in China. The 29 July 2021 breach may have been influenced by several factors, such as regulatory changes in China’s energy sector, market volatility or concerns about the growth prospects of Chinese clean energy companies.

Table 5 shows the results of the Gregory and Hansen (1996) test for long-term connections, applied to sustainable energy indices such as the ISE Clean Edge Global Wind Energy, S&P Global Clean Energy, S&P TSX Renewable Energy and Clean Technology, Solactive China Clean Energy, as well as the cryptocurrencies Bitcoin (BTC), Ethereum (ETH), Cardano (ADA), Ripple (XRP), Stellar (XLM), from January 2020 to September 2023. Based on the analysis carried out, we found 34 significant long-term connections out of a possible 72.

With regard to the ADA cryptocurrency, we realise that it is connected to BTC, ETH, LTC, XLM, XRP, ISE Clean, S&P Global Clean, S&P TRX Clean, Solactive China Clean, meaning that this clean energy currency cannot be considered a safe haven for its peers in the long term. BTC, a digital currency classified as "dirty", is connected to the cryptocurrencies ADA, ETH, LTC and XRP, which can be seen as a long-term safe haven for the clean cryptocurrency XLM, and for the energy indices ISE Clean Edge Global Wind Energy, S&P Global Clean Energy, S&P TSX Renewable Energy and Clean Technology, Solactive China Clean Energy. Ethereum (ETH), also called dirty due to its excessive energy consumption, is connected to BTC and XRP, proving to be a hedge for the other digital currencies and for all the clean energy stock indices. Stellar (XLM) is connected to the ADA and BTC cryptocurrencies and is a safe haven for ETH, XRP, shows significant long-term connectivity with the ISE Clean Edge and Solactive China Clean Energy indices, and is a hedge for the S&P Global Clean Energy, S&P TSX Renewable energy indices. The cryptocurrency Ripple (XRP) has connections with all of its peers except Solactive China Clean, lacking the hedging properties of digital currencies and most clean energy indices.

When we analyse the sustainable energy indices, we see that the ISE Clean Edge can be considered a long-term hedge for digital currencies, with the exception of ADA, while clean energy can be considered a safe haven. With regard to the S&P Global Clean Energy, S&P TSX Renewable Energy and Clean Technology energy indices, we can see that they are a significant hedge for all cryptocurrencies and other sustainable energy stock indices, the exception being Solactive China Clean Energy. Finally, the Chinese solar energy index is a safe haven for all the cryptocurrencies analysed, but it does not have the characteristics of a safe haven for clean energy.

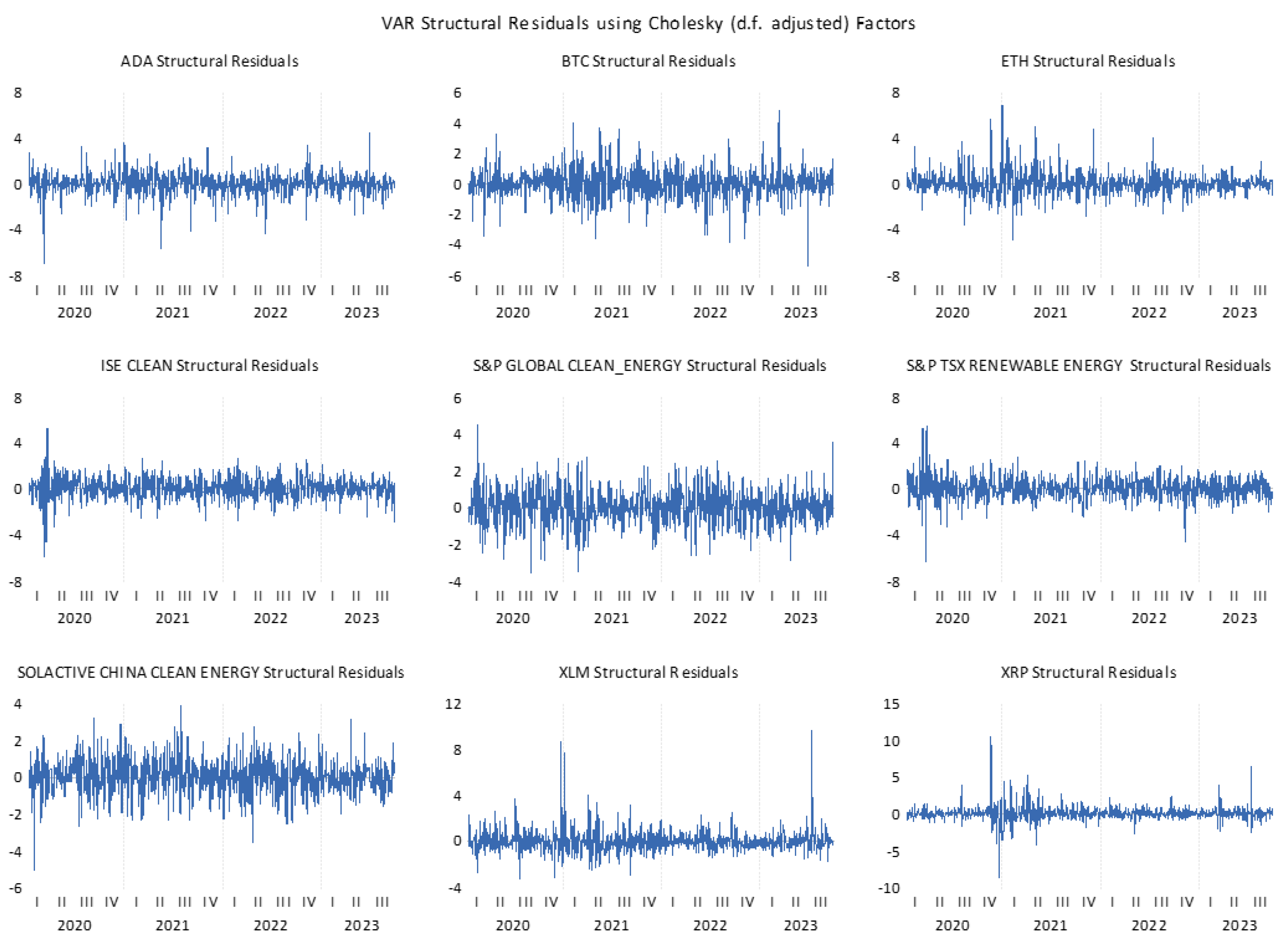

Figure 2 shows the residual structure of the VAR with Cholesky decomposition and shows that autocorrelation is absent for lag 8. To achieve the absence of autocorrelation in the residuals, we used the LR information criterion: sequential modified LR test statistic (each test at 5% level) for 7-day lags. Based on these results, we can see that the SVAR results are robust because the returns are stationary and there is no autocorrelation in the residuals.

Source: Own elaboration.

Table 6 shows the results of the SVAR test for short-term connections (7 days), applied to sustainable energy indices such as the ISE Clean Edge Global Wind Energy, S&P Global Clean Energy, S&P TSX Renewable Energy and Clean Technology, Solactive China Clean Energy, as well as the cryptocurrencies Bitcoin (BTC), Ethereum (ETH), Cardano (ADA), Ripple (XRP), Stellar (XLM), from January 2020 to September 2023. Based on the results, when we change the GH methodology, which measures long-term connectivity, we see the presence of 34 long-term relationships, but when we estimate in the short term (7 days) we realise that the relationships between the assets under analysis decrease to 25 shocks out of a possible 72.

With regard to cryptocurrencies, we found that the clean digital currency ADA only moves with XRP, which shows that it is a safe haven asset for the cryptos Bitcoin (BTC), Ethereum (ETH), Stellar (XLM), and for the clean energy indices ISE Clean, S&P Global, S&P TSX, Solactive China. The digital currency BTC has movements of ETH, XLM, XRP, and with the Chinese index (Solactive), it can be a safe haven asset for the digital currency ADA and for the Nasdaq (ISE Clean Edge Global Wind Energy), Dow Jones (S&P Global Clean Energy), and Canadian (S&P TSX Renewable Energy) indices. The Ethereum (ETH) cryptocurrency moves with the BTC, XLM and XRP digital currencies, and is a hedging asset for Cardano (ADA) and all the clean energy indices under analysis. The Ripple cryptocurrency (XRP) shows movements with the ADA and XLM digital currencies, presenting safe haven characteristics for the BTC and ETH cryptocurrencies, and for the sustainable energy indices under analysis. The digital currency Stellar (XLM) shows movements with BTC, XRP, and the China index (Solactive), showing evidence of a safe haven asset for the digital currencies ADA, ETH and the clean energy indices ISE Clean Edge Global Wind Energy, S&P Global Clean Energy, S&P TSX Renewable Energy and Clean Technology.

The sustainable energy stock indices also show short-term connections, namely the ISE Clean Edge shows movements with the digital currencies XLM and XRP, and with the S&P Global, S&P TSX Renewable and Solactive China Clean Energy indices showing hedging/safe haven characteristics only with the cryptocurrencies ADA, BTC and ETH, not proving to be a safe-haven asset for its energy peers. The S&P Global Clean Energy shows movements with the XRP cryptocurrency and with the ISE Clean Edge, S&P TSX Renewable, Solactive China indices, proving to be a hedging asset for the digital currencies ADA, BTC, ETH, XLM, but not for the energy indices. The S&P TSX Renewable index shows signs of movement with the clean energies ISE Clean Edge, S&P Global and Solactive China, proving to be a safe haven for the cryptocurrencies ADA, BTC, ETH, XRP and XLM, but not for its clean energy peers. The China index (Solactive China Clean Energy) has safe harbour properties for the digital currencies ADA, BTC, ETH, XRP and XLM, as well as for the ISE Clean Edge Global Wind Energy, S&P Global Clean Energy, S&P TSX Renewable Energy and Clean Technology indices.

5. Discussion

In this study we examine the long- and short-term relationships between dirty cryptocurrencies such as Bitcoin (BTC), Ethereum (ETH), clean cryptocurrencies such as Cardano (ADA), Ripple (XRP), Stellar (XLM), and green energies such as ISE Clean Edge Global Wind Energy, S&P Global Clean Energy, S&P TSX Renewable Energy and Clean Technology, Solactive China Clean Energy, in the period from January 2020 to September 2023.

With regard to long-term connections, we realised that the ADA digital currency is connected to several digital currencies and clean energy indices, however, it is not necessarily considered a long-term safe haven. BTC is considered a "dirty" cryptocurrency due to its energy consumption and is connected to the digital currencies ADA, ETH, LTC and XRP. It appears to serve as a long-term safe haven for the clean cryptocurrency XLM and the clean energy indices. ETH is another "dirty" cryptocurrency, linked to BTC and XRP. It seems to act as a hedge for other digital currencies and clean energy stock indices. XLM is connected to ADA and BTC, serving as a safe harbour for ETH and XRP. It also has long-term connectivity with certain clean energy indices (ISE Clean and Solactive China Clean). XRP is connected to most of its peers yet has no hedging properties for digital currencies and some clean energy indices.

With regard to indices, we realised that the ISE Clean Edge appears to be a long-term hedge for digital currencies, except for ADA, while other indices such as S&P Global Clean Energy, S&P TSX Renewable Energy and Clean Technology are significant hedges for cryptocurrencies and other sustainable energy stock indices. However, Solactive China Clean Energy does not offer the same hedge. The Chinese index (Solactive) is considered a safe haven for all the cryptocurrencies under analysis, but it does not work as a safe haven for clean energy.

In short, the relationship between cryptocurrencies and sustainable energy indices is complex. Bitcoin (BTC) and Ethereum (ETH), considered "dirty" cryptocurrencies, can serve as safe havens or long-term hedges for other assets. Clean cryptocurrencies such as ADA and XLM have varied connections. Clean energy indices generally provide hedges for cryptocurrencies, except for Solactive China Clean Energy. The Chinese Solar Energy Index is a safe haven for cryptocurrencies, but not necessarily for clean energy assets.

When analysing short-term connections (7 days), there are 25 significant relationships out of 72 possible, which is less than the 34 long-term relationships found using the GH methodology. ADA is mainly connected to the XRP crypto in the short term, indicating that it serves as a safe haven for XRP and other clean energy indices such as ISE Clean, S&P Global, S&P TSX and Solactive China. BTC is linked to ETH, XLM and XRP in the short term. It can act as a safe haven asset for the ADA, Nasdaq (ISE Clean Edge Global Wind Energy), Dow Jones (S&P Global Clean Energy) and Canadian (S&P TSX Renewable Energy) indices. ETH moves in the short term with BTC, XLM and XRP. It serves as a hedge asset for ADA and all the clean energy indices under analysis. XRP is connected to ADA and XLM. It appears to be a safe haven for BTC, ETH and the sustainable energy indices studied. Stellar (XLM) is connected to BTC, XRP and the China index (Solactive). It acts as a safe haven asset for ADA, ETH, and several clean energy indices, including ISE Clean Edge Global Wind Energy, S&P Global Clean Energy, S&P TSX Renewable Energy and Clean Technology.

The short-term connections between sustainable energy stock indices and cryptocurrencies reveal the following: ISE Clean Edge has short-term movements with XLM and XRP, but demonstrates hedging characteristics only with ADA, BTC and ETH, not serving as a safe haven for its energy peers. The S&P Global Clean Energy shows short-term links with XRP and other indices such as ISE Clean Edge, S&P TSX Renewable and Solactive China, but we realise that it acts as a hedge asset for the digital currencies ADA, BTC, ETH and XLM, rather than for energy indices. The S&P TSX Renewable displays short-term movements with clean energy indices such as ISE Clean Edge, S&P Global and Solactive China. It serves as a safe haven for ADA, BTC, ETH, XRP and XLM, but not for their clean energy peers. Finally, the Solactive China Clean Energy index demonstrates safe haven properties for the digital currencies ADA, BTC, ETH, XRP and XLM, as well as for clean energy indices such as ISE Clean Edge Global Wind Energy, S&P Global Clean Energy, S&P TSX Renewable Energy and Clean Technology.

6. Conclusions

In this study we examine the long- and short-term relationships between dirty cryptocurrencies such as Bitcoin (BTC), Ethereum (ETH), clean cryptocurrencies such as Cardano (ADA), Ripple (XRP), Stellar (XLM), and green energies such as ISE Clean Edge Global Wind Energy, S&P Global Clean Energy, S&P TSX Renewable Energy and Clean Technology, Solactive China Clean Energy, in the period from January 2020 to September 2023.

It is possible to see that investors looking to align their portfolios with sustainable and environmentally responsible goals should consider diversifying their holdings. While some cryptocurrencies, such as BTC and ETH, can offer safe haven or hedge properties, clean cryptocurrencies such as ADA, XLM and XRP can provide additional opportunities for diversification. This diversification can help reduce risk and promote a more balanced portfolio. It is essential that investors recognise the differences between long-term and short-term asset relationships. Long-term links can provide insights into the broader stability of assets, while short-term links can reveal more immediate trading opportunities. Balancing both perspectives can help in devising a complete investment strategy. Sustainable energy indices, despite their complex relationships with cryptocurrencies, continue to be relevant for investors focused on clean and green energy.

In conclusion, balancing sustainability goals with investment strategies in the cryptocurrency and clean energy space requires careful consideration of the unique characteristics and relationships of these assets. Diversification, from a long-term perspective, and keeping informed about changing dynamics are essential elements for investors committed to social and environmental responsibility.

Author Contributions

The two authors, R.D. and A.F.S., contributed equally to this work. All authors have read and agreed to the published version of the manuscript.

Funding

This paper is financed by the Instituto Politécnico de Setúbal.

Data Availability Statement

The authors confirm that the data supporting the findings of this study are available within this article.

Acknowledgments

This work would not have been possible without the financial support of the Instituto Politécnico de Setúbal.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Imbulana Arachchi, J.; Managi, S. Preferences for energy sustainability: Different effects of gender on knowledge and importance. Renewable and Sustainable Energy Reviews 2021, 141. [CrossRef]

- Xu, M.; David, J.M.; Kim, S.H. The fourth industrial revolution: Opportunities and challenges. International Journal of Financial Research 2018, 9, 90–95. [CrossRef]

- Bañales, S. The enabling impact of digital technologies on distributed energy resources integration. Journal of Renewable and Sustainable Energy 2020, 12. [CrossRef]

- Rotatori, D.; Lee, E.J.; Sleeva, S. The evolution of the workforce during the fourth industrial revolution. Human Resource Development International 2021, 24, 92–103. [CrossRef]

- Zhang, Y.J.; Da, Y.B. The decomposition of energy-related carbon emission and its decoupling with economic growth in China, 2015. [CrossRef]

- Wang, J.; Yang, Y. A regional-scale decomposition of energy-related carbon emission and its decoupling from economic growth in China. Environmental Science and Pollution Research 2020, 27, 20889–20903. [CrossRef]

- Jardón, A.; Kuik, O.; Tol, R.S. Economic growth and carbon dioxide emissions: An analysis of Latin America and the Caribbean. Atmosfera 2017, 30, 87–100. [CrossRef]

- Dong, K.; Hochman, G.; Zhang, Y.; Sun, R.; Li, H.; Liao, H. CO2 emissions, economic and population growth, and renewable energy: Empirical evidence across regions. Energy Economics 2018, 75, 180–192. [CrossRef]

- Olivera, M.; Segarra, V. Environmental quality and economic growth: Dynamic analysis for Latin America and the Caribbean. Revista de Economia del Rosario 2021, 24, 1–40. [CrossRef]

- Wang, P.; Zhang, H.; Yang, C.; Guo, Y. Time and frequency dynamics of connectedness and hedging performance in global stock markets: Bitcoin versus conventional hedges. Research in International Business and Finance 2021, 58. [CrossRef]

- Danino-Perraud, R. The Recycling of liThium-ion BaTTeRies A Strategic Pillar for the European Battery Alliance études de l’Ifri Raphaël Danino-PeRRauD Center for Energy; Number March, 2020.

- Xiong, G.; Deng, J.; Ding, B. Characteristics, decoupling effect, and driving factors of regional tourism’s carbon emissions in China. Environmental Science and Pollution Research 2022, 29, 47082–47093. [CrossRef]

- Santos, M.R.; Rolo, A.; Matos, D.; Carvalho, L. The Circular Economy in Corporate Reporting: Text Mining of Energy Companies’ Management Reports. Energies 2023, 16, 1–16. [CrossRef]

- Georgeson, L.; Maslin, M. Estimating the scale of the US green economy within the global context. Palgrave Communications 2019, 5. [CrossRef]

- Fekete, H.; Kuramochi, T.; Roelfsema, M.; den Elzen, M.; Forsell, N.; Höhne, N.; Luna, L.; Hans, F.; Sterl, S.; Olivier, J.; van Soest, H.; Frank, S.; Gusti, M. A review of successful climate change mitigation policies in major emitting economies and the potential of global replication. Renewable and Sustainable Energy Reviews 2021, 137. [CrossRef]

- Giglio, E.; Pedro, F.; Cagica, L.; Xara, D. The governance of E-waste recycling networks: Insights from São Paulo City. Waste Management 2023, 161, 10–16. [CrossRef]

- Baruník, J.; Křehlík, T. Measuring the frequency dynamics of financial connectedness and systemic risk. Journal of Financial Econometrics 2018, 16, 271–296, [1507.01729]. [CrossRef]

- Arif, M.; Hasan, M.; Alawi, S.M.; Naeem, M.A. COVID-19 and time-frequency connectedness between green and conventional financial markets. Global Finance Journal 2021, 49. [CrossRef]

- Sharma, G.D.; Sarker, T.; Rao, A.; Talan, G.; Jain, M. Revisting conventional and green finance spillover in post-COVID world: Evidence from robust econometric models. Global Finance Journal 2022, 51. [CrossRef]

- Silva, A.F.; Carvalho, L.; Sánchez-Hernández, M.I., Social Innovation: Insights in the Fourth Sector in Portugal. In Studies on Entrepreneurship, Structural Change and Industrial Dynamics; Sánchez-Hernández, M.I.; Carvalho, L.; Rego, C.; Lucas, M.R.; Noronha, A., Eds.; Springer International Publishing: Cham, 2021; pp. 255–281. [CrossRef]

- Silva, A.F.; Carvalho, L.; Sánchez-Hernández, M.I., Social Innovation: Insights in the Fourth Sector in Portugal. In Studies on Entrepreneurship, Structural Change and Industrial Dynamics; Sánchez-Hernández, M.I.; Carvalho, L.; Rego, C.; Lucas, M.R.; Noronha, A., Eds.; Springer International Publishing: Cham, 2021; pp. 255–281. [CrossRef]

- Haq, I.U. Cryptocurrency Environmental Attention, Green Financial Assets, and Information Transmission: Evidence From the COVID-19 Pandemic. Energy Research Letters 2022, 4, 1–6.

- Bejan, C.A.; Bucerzan, D.; Crăciun, M.D. Bitcoin price evolution versus energy consumption; trend analysis. Applied Economics 2023, 55, 1497–1511. [CrossRef]

- Putri, D.E.; Ilham, R.N.; Sinurat, M.; Lilinesia, L.; Saragih, M.M.S. Analysis of Potential and Risks Investing in Financial Instruments and Digital Cryptocurrency Assets during the Covid-19 Pandemic. Jurnal SEKURITAS (Saham, Ekonomi, Keuangan dan Investasi) 2021, 5, 1. [CrossRef]

- O’Dwyert, K.J.; Malone, D. Bitcoin mining and its energy footprint. IET Conference Publications, 2014, Vol. 2014, pp. 280–285. [CrossRef]

- Ghosh, B.; Bouri, E. Is Bitcoin’s Carbon Footprint Persistent? Multifractal Evidence and Policy Implications. Entropy 2022, 24, 5. [CrossRef]

- Merza, S.A. Economic Risks Associated with Bit Coin: A Comprehensive Analysis. Journal of Corporate Finance Management and Banking System 2023, pp. 1–12. [CrossRef]

- Polemis, M.L.; Tsionas, M.G. The environmental consequences of blockchain technology: A Bayesian quantile cointegration analysis for Bitcoin. International Journal of Finance and Economics 2023, 28, 1602–1621. [CrossRef]

- Sarkodie, S.A.; Amani, M.A.; Ahmed, M.Y.; Owusu, P.A. Assessment of Bitcoin carbon footprint. Sustainable Horizons 2023, 7. [CrossRef]

- Ren, B.; Lucey, B. A clean, green haven?—Examining the relationship between clean energy, clean and dirty cryptocurrencies. Energy Economics 2022, 109. [CrossRef]

- Ren, B.; Lucey, B. Do clean and dirty cryptocurrency markets herd differently? Finance Research Letters 2022, 47. [CrossRef]

- Bouri, E.; Das, M.; Gupta, R.; Roubaud, D. Spillovers between Bitcoin and other assets during bear and bull markets. Applied Economics 2018, 50, 5935–5949. [CrossRef]

- Kakinuma, Y. Nexus between Southeast Asian stock markets, bitcoin and gold: spillover effect before and during the COVID-19 pandemic. Journal of Asia Business Studies 2022, 16, 693–711. [CrossRef]

- Klein, T.; Pham Thu, H.; Walther, T. Bitcoin is not the New Gold – A comparison of volatility, correlation, and portfolio performance. International Review of Financial Analysis 2018, 59, 105–116. [CrossRef]

- Shahzad, S.J.H.; Bouri, E.; Roubaud, D.; Kristoufek, L.; Lucey, B. Is Bitcoin a better safe-haven investment than gold and commodities? International Review of Financial Analysis 2019, 63, 322–330. [CrossRef]

- Dias, R.; Alexandre, P.; Teixeira, N.; Chambino, M. Clean Energy Stocks: Resilient Safe Havens in the Volatility of Dirty Cryptocurrencies. Energies 2023, 16. [CrossRef]

- Dias, R.; Horta, N.; Revez, C.; Heliodoro, P.; Alexandre, P. The Evolution of the Cryptocurrency Market Is Trending toward Efficiency? 8th International Scientific ERAZ Conference – ERAZ 2022 – Conference Proceedings 2022, pp. 87–94. [CrossRef]

- Gao, L.; Guo, K.; Wei, X. Dynamic relationship between green bonds and major financial asset markets from the perspective of climate change. Frontiers in Environmental Science 2023, 10. [CrossRef]

- Lorente, D.B.; Mohammed, K.S.; Cifuentes-Faura, J.; Shahzad, U. Dynamic connectedness among climate change index, green financial assets and renewable energy markets: Novel evidence from sustainable development perspective. Renewable Energy 2023, 204, 94–105. [CrossRef]

- Jiang, S.; Li, Y.; Lu, Q.; Wang, S.; Wei, Y. Volatility communicator or receiver? Investigating volatility spillover mechanisms among Bitcoin and other financial markets. Research in International Business and Finance 2022, 59. [CrossRef]

- Kuang, W. Are clean energy assets a safe haven for international equity markets? Journal of Cleaner Production 2021, 302. [CrossRef]

- Angelini, E.; Birindelli, G.; Chiappini, H.; Foglia, M. Clean energy indices and brown assets: an analysis of tail risk spillovers through the VAR for VaR model. Journal of Sustainable Finance and Investment 2022. [CrossRef]

- Ozdurak, C.; Umut, A.; Ozay, T. The Interaction of Major Crypto-assets, Clean Energy, and Technology Indices in Diversified Portfolios. International Journal of Energy Economics and Policy 2022, 12, 480–490. [CrossRef]

- Kamal, J.B.; Hassan, M.K. Asymmetric connectedness between cryptocurrency environment attention index and green assets. Journal of Economic Asymmetries 2022, 25. [CrossRef]

- Arfaoui, N.; Naeem, M.A.; Boubaker, S.; Mirza, N.; Karim, S. Interdependence of clean energy and green markets with cryptocurrencies. Energy Economics 2023, 120. [CrossRef]

- Sharif, A.; Brahim, M.; Dogan, E.; Tzeremes, P. Analysis of the spillover effects between green economy, clean and dirty cryptocurrencies. Energy Economics 2023, 120. [CrossRef]

- Naeem, M.A.; Gul, R.; Farid, S.; Karim, S.; Lucey, B.M. Assessing linkages between alternative energy markets and cryptocurrencies. Journal of Economic Behavior and Organization 2023, 211, 513–529. [CrossRef]

- Anwer, Z.; Farid, S.; Khan, A.; Benlagha, N. Cryptocurrencies versus environmentally sustainable assets: Does a perfect hedge exist? International Review of Economics and Finance 2023, 85, 418–431. [CrossRef]

- Jarque, C.M.; Bera, A.K. Efficient tests for normality, homoscedasticity and serial independence of regression residuals. Economics Letters 1980, 6, 255–259. [CrossRef]

- Breitung, J. The local power of some unit root tests for panel data. Advances in Econometrics 2000, 15, 161–177. [CrossRef]

- Clemente, J.; Montañés, A.; Reyes, M. Testing for a unit root in variables with a double change in the mean. Economics Letters 1998, 59, 175–182. [CrossRef]

- Gregory, A.W.; Hansen, B.E. Residual-based tests for cointegration in models with regime shifts. Journal of Econometrics 1996, 70, 99–126. [CrossRef]

Figure 1.

Evolution, in first differences, of sustainable energy stock indices, dirty cryptocurrencies and clean cryptocurrencies, from January 2020 to September 2023.

Figure 1.

Evolution, in first differences, of sustainable energy stock indices, dirty cryptocurrencies and clean cryptocurrencies, from January 2020 to September 2023.

Figure 2.

VAR Structural Residuals using Cholesky Factors, from January 2020 to September 2023.

Table 1.

Summary table of the main statistics, in terms of returns, for cryptocurrencies from January 2020 to September 2023.

Table 1.

Summary table of the main statistics, in terms of returns, for cryptocurrencies from January 2020 to September 2023.

| ADA | BTC | ETH | XLM | XRP | |

|---|---|---|---|---|---|

| Mean | 0.000514 | 0.001397 | 0.002610 | 0.000918 | 0.001020 |

| Std. Dev. | 0.057312 | 0.040735 | 0.053197 | 0.057453 | 0.067312 |

| Skewness | -0.962139 | -0.679045 | -0.661853 | 1.175606 | 0.723799 |

| Kurtosis | 9.719497 | 9.499837 | 10.65963 | 17.79364 | 19.44905 |

| Jarque-Bera | 1990.820 | 1796.761 | 2462.201 | 9143.484 | 11111.17 |

| Probability | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 |

| Observations | 978 | 978 | 978 | 978 | 978 |

Source: Own elaboration.

Table 2.

Summary table of the main statistics, in returns, relating to the sustainable energy indices, for the period from January 2020 to September 2023.

Table 2.

Summary table of the main statistics, in returns, relating to the sustainable energy indices, for the period from January 2020 to September 2023.

| ISE CLEAN | S&P GLOBAL CLEAN | S&P TSX RENEWABLE ENERGY | SOLACTIVE CHINA CLEAN ENERGY | |

|---|---|---|---|---|

| Mean | -7.41E-05 | 0.000228 | -0.000391 | 0.000517 |

| Std. Dev. | 0.014401 | 0.020064 | 0.017327 | 0.017442 |

| Skewness | -0.660691 | -0.380926 | -0.846904 | -0.097354 |

| Kurtosis | 12.64018 | 8.237000 | 13.55373 | 4.533476 |

| Jarque-Bera | 3862.119 | 1142.436 | 4660.460 | 97.47009 |

| Probability | 0.000000 | 0.000000 | 0.000000 | 0.000000 |

| Observations | 978 | 978 | 978 | 978 |

Source: Own elaboration.

Table 3.

Breitung (2000) panel unit root test for the energy and cryptocurrency data series from January 2020 to September 2023.

| Null Hypothesis: Unit root (common unit root process) | ||||

|---|---|---|---|---|

| Method | Statistic | Prob.** | ||

| Breitung t-stat | -59.2910 | 0.0000 | ||

| Intermediate regression results on D(UNTITLED) | ||||

| Series | S. E. of Regression | Lag | Max Lag | Obs |

| D(ADA) | 8.51370 | 3 | 21 | 974 |

| D(BTC) | 1875.57 | 0 | 21 | 977 |

| D(ETH) | 112.877 | 3 | 21 | 974 |

| D(ISE CLEAN) | 3.96089 | 0 | 21 | 977 |

| D(S&P GLOBAL CLEAN) | 43.3593 | 0 | 21 | 977 |

| D(S&P TSX) | 3.62919 | 1 | 21 | 976 |

| D(SOLACTIVE CHINA) | 56.1901 | 0 | 21 | 977 |

| D(XLM) | 0.02157 | 0 | 21 | 977 |

| D(XRP) | 0.06707 | 0 | 21 | 977 |

| Coefficient | t-Stat | SE Reg | Obs | |

| Pooled | -0.69822 | -59.291 | 0.012 | 8777 |

Source: Own elaboration.

Table 4.

Summary table of the Crashes of dirty cryptocurrencies, clean cryptocurrencies, and sustainable energies, from January 2020 to September 2023.

Table 4.

Summary table of the Crashes of dirty cryptocurrencies, clean cryptocurrencies, and sustainable energies, from January 2020 to September 2023.

| Market | t-stat | Crash |

|---|---|---|

| ADA | -34.10615 (0)*** | 19/05/2021 |

| BTC | -31.85679 (0)*** | 23/02/2021 |

| ETH | -33.47025 (0)*** | 19/05/2021 |

| XLM | -32.94326 (0)*** | 19/05/2021 |

| XRP | -33.19744 (0)*** | 13/04/2021 |

| ISE Clean | -27.32536 (0)*** | 12/03/2020 |

| S&P Global Clean | -27.75393 (0)*** | 07/01/2021 |

| S&P TRX Clean | -31.27196 (0)*** | 08/02/2021 |

| Solactive China Clean | -31.97915 (0)*** | 29/07/2021 |

Source: Own elaboration. Note: Lag Length (Automatic Length based on SIC). Break Selection: Minimise Dickey-Fuller t-statistic. Side values in brackets refer to lags. The asterisks ***, **, and * represent the significance of the statistic at 1%, 5% and 10% respectively.

Table 5.

Summary table of long-term shocks between dirty cryptocurrencies, clean cryptocurrencies, and sustainable energies, from January 2020 to September 2023.

Table 5.

Summary table of long-term shocks between dirty cryptocurrencies, clean cryptocurrencies, and sustainable energies, from January 2020 to September 2023.

| Market | t-stat | Results |

| ADA | BTC | -5.45** | Shock L/ Time |

| ADA | ETH | -5.95*** | Shock L/ Time |

| ADA | XLM | -5.59*** | Shock L/ Time |

| ADA | XRP | -5.43** | Shock L/ Time |

| ADA | ISE Clean | -5.71*** | Shock L/ Time |

| ADA | S&P Global Clean | -4.87* | Shock L/ Time |

| ADA | S&P TRX Clean | -4.85* | Shock L/ Time |

| ADA | Solactive China Clean | -4.73* | Shock L/ Time |

| Market | t-stat | Results |

| BTC | ADA | -4.91* | Shock L/ Time |

| BTC | ETH | -4.92* | Shock L/ Time |

| BTC | XLM | -4.50 | Non-existent |

| BTC | XRP | -4.85* | Shock L/ Time |

| BTC | ISE Clean | -4.07 | Non-existent |

| BTC | S&P Global Clean | -3.68 | Non-existent |

| BTC | S&P TRX Clean | -3.61 | Non-existent |

| BTC | Solactive China Clean | -3.33 | Non-existent |

| Market | t-stat | Results |

| ETH | ADA | -4.55 | Non-existent |

| ETH | BTC | -5.71*** | Shock L/ Time |

| ETH | XLM | -4.37 | Non-existent |

| ETH | XRP | -5.18** | Shock L/ Time |

| ETH | ISE Clean | -4.31 | Non-existent |

| ETH | S&P Global Clean | -4.04 | Non-existent |

| ETH | S&P TRX Clean | -4.18 | Non-existent |

| ETH | Solactive China Clean | -4.70 | Non-existent |

| Market | t-stat | Results |

| XLM | ADA | -5.18** | Shock L/ Time |

| XLM | BTC | -4.82* | Shock L/ Time |

| XLM | ETH | -4.29 | Non-existent |

| XLM | XRP | -4.56 | Non-existent |

| XLM | ISE Clean | -4.79* | Shock L/ Time |

| XLM | S&P Global Clean | -4.59 | Non-existent |

| XLM | S&P TRX Clean | -4.61 | Non-existent |

| XLM | Solactive China Clean | -4.89* | Shock L/ Time |

| Market | t-stat | Results |

| XRP | ADA | -6.29*** | Shock L/ Time |

| XRP | BTC | -5.69*** | Shock L/ Time |

| XRP | ETH | -5.60*** | Shock L/ Time |

| XRP | XLM | -4.81* | Shock L/ Time |

| XRP | ISE Clean | -5.12** | Shock L/ Time |

| XRP | S&P Global Clean | -4.82* | Shock L/ Time |

| XRP | S&P TRX Clean | -4.86* | Shock L/ Time |

| XRP | Solactive China Clean | -4.37 | Non-existent |

| Market | t-stat | Results |

| ISE Clean | ADA | -5.16** | Shock L/ Time |

| ISE Clean | BTC | -4.38 | Non-existent |

| ISE Clean | ETH | -4.04 | Non-existent |

| ISE Clean | XLM | -4.49 | Non-existent |

| ISE Clean | XRP | -4.42 | Non-existent |

| ISE Clean | S&P Global Clean | -3.72 | Non-existent |

| ISE Clean | S&P TRX Clean | -3.64 | Non-existent |

| ISE Clean | Solactive China Clean | -4.34 | Non-existent |

| Market | t-stat | Results |

| S&P Global Clean | ADA | -4.03 | Non-existent |

| S&P Global Clean | BTC | -4.26 | Non-existent |

| S&P Global Clean | ETH | -4.41 | Non-existent |

| S&P Global Clean | LTC | -4.37 | Non-existent |

| S&P Global Clean | XLM | -4.24 | Non-existent |

| S&P Global Clean | XRP | -4.49 | Non-existent |

| S&P Global Clean | ISE Clean | -3.39 | Non-existent |

| S&P Global Clean | S&P TRX Clean | -4.26 | Non-existent |

| S&P Global Clean | Solactive China Clean | -5.21** | Shock L/ Time |

| Market | t-stat | Results |

| S&P TRX Clean | ADA | -4.40 | Non-existent |

| S&P TRX Clean | BTC | -4.09 | Non-existent |

| S&P TRX Clean | ETH | -4.31 | Non-existent |

| S&P TRX Clean | LTC | -4.28 | Non-existent |

| S&P TRX Clean | XLM | -4.30 | Non-existent |

| S&P TRX Clean | XRP | -4.33 | Non-existent |

| S&P TRX Clean | ISE Clean | -3.81 | Non-existent |

| S&P TRX Clean | S&P Global Clean | -4.68 | Non-existent |

| S&P TRX Clean | Solactive China Clean | -5.27** | Shock L/ Time |

| Market | t-stat | Results |

| Solactive China Clean | ADA | -3.30 | Non-existent |

| Solactive China Clean | BTC | -3.21 | Non-existent |

| Solactive China Clean | ETH | -3.40 | Non-existent |

| Solactive China Clean | LTC | -3.30 | Non-existent |

| Solactive China Clean | XLM | -4.44 | Non-existent |

| Solactive China Clean | XRP | -3.19 | Non-existent |

| Solactive China Clean | ISE Clean | -4.79* | Shock L/ Time |

| Solactive China Clean | S&P Global Clean | -5.57*** | Shock L/ Time |

| Solactive China Clean | S&P TRX Clean | -5.52*** | Shock L/ Time |

Source: Own elaboration. Notes: ***, **, and * significant at 1%, 5%, and 10%, respectively.

Table 6.

Summary table of short-term clashes between dirty cryptocurrencies, clean cryptocurrencies, and sustainable energies.

Table 6.

Summary table of short-term clashes between dirty cryptocurrencies, clean cryptocurrencies, and sustainable energies.

| Market | F-Statistic | Results |

| BTC | ADA | 1.58 | Non-existent |

| ADA | BTC | 1.46 | Non-existent |

| ETH | ADA | 0.99 | Non-existent |

| ADA | ETH | 1.08 | Non-existent |

| ISE CLEAN | ADA | 1.35 | Non-existent |

| ADA | ISE CLEAN | 0.94 | Non-existent |

| S&P Global Clean | ADA | 1.08 | Non-existent |

| ADA | S&P Global Clean | 1.68 | Non-existent |

| S&P TRX Clean | ADA | 1.42 | Non-existent |

| ADA | S&P TRX Clean | 1.57 | Non-existent |

| Solactive China Clean | ADA | 0.46 | Non-existent |

| ADA | Solactive China Clean | 1.37 | Non-existent |

| XLM | ADA | 1.29 | Non-existent |

| ADA | XLM | 1.07 | Non-existent |

| XRP |ADA | 2.68*** | Shock |

| ADA | XRP | 3.36*** | Shock |

| ETH | BTC | 1.82* | Shock |

| BTC | ETH | 1.89* | Shock |

| ISE CLEAN | BTC | 1.60 | Non-existent |

| BTC | ISE CLEAN | 0.80 | Non-existent |

| S&P Global Clean | BTC | 0.68 | Non-existent |

| BTC | S&P Global Clean | 1.29 | Non-existent |

| S&P TRX Clean | BTC | 1.04 | Non-existent |

| BTC | S&P TRX Clean | 1.51 | Non-existent |

| Solactive China Clean | BTC | 0.41 | Non-existent |

| BTC | Solactive China Clean | 1.74* | Shock |

| XLM | BTC | 2.01** | Shock |

| BTC | XLM | 2.30** | Shock |

| XRP | BTC | 1.24 | Non-existent |

| BTC | XRP | 1.77* | Shock |

| ISE CLEAN | ETH | 1.49 | Non-existent |

| ETH | ISE CLEAN | 0.86 | Non-existent |

| S&P Global Clean | ETH | 0.64 | Non-existent |

| ETH | S&P Global Clean | 0.64 | Non-existent |

| S&P TRX Clean | ETH | 1.12 | Non-existent |

| ETH | S&P TRX Clean | 1.51 | Non-existent |

| Solactive China Clean | ETH | 0.28 | Non-existent |

| ETH | Solactive China Clean | 1.17 | Non-existent |

| XLM | ETH | 0.66 | Non-existent |

| ETH | XLM | 1.90* | Shock |

| XRP | ETH | 1.58 | Non-existent |

| ETH | XRP | 2.42** | Shock |

| S&P Global Clean | ISE CLEAN | 5.66*** | Shock |

| ISE CLEAN | S&P Global Clean | 1.84* | Shock |

| S&P TRX Clean | ISE CLEAN | 3.43*** | Shock |

| ISE CLEAN | S&P TRX Clean | 3.82*** | Shock |

| Solactive China Clean | ISE CLEAN | 0.65 | Non-existent |

| ISE CLEAN | Solactive China Clean | 3.92*** | Shock |

| XLM | ISE CLEAN | 0.17 | Non-existent |

| ISE CLEAN | XLM | 2.40** | Shock |

| XRP | ISE CLEAN | 0.19 | Non-existent |

| ISE CLEAN | XRP | 2.42** | Shock |

| S&P TRX Clean | S&P Global Clean | 2.18** | Shock |

| S&P Global Clean | S&P TRX Clean | 3.77*** | Shock |

| Solactive China Clean | S&P Global Clean | 0.42 | Non-existent |

| S&P Global Clean | Solactive China Clean | 5.33*** | Shock |

| XLM | S&P Global Clean | 0.62 | Non-existent |

| S&P Global Clean | XLM | 1.64 | Non-existent |

| XRP | S&P Global Clean | 0.50 | Non-existent |

| S&P Global Clean | XRP | 1.72* | Shock |

| Solactive China Clean | S&P TRX Clean | 0.68 | Non-existent |

| S&P TRX Clean | Solactive China Clean | 3.96*** | Shock |

| XLM | S&P TRX Clean | 0.61 | Non-existent |

| S&P TRX Clean | XLM | 1.23 | Non-existent |

| XRP | S&P TRX Clean | 0.34 | Non-existent |

| S&P TRX Clean | XRP | 1.46 | Non-existent |

| XLM | Solactive China Clean | 2.82*** | Shock |

| Solactive China Clean | XLM | 0.76 | Non-existent |

| XRP | Solactive China Clean | 1.60 | Non-existent |

| Solactive China Clean | XRP | 0.65 | Non-existent |

| XRP | XLM | 3.13*** | Shock |

| XLM | XRP | 2.04** | Shock |

Source: Own elaboration. Notes: ***, **, and * significant at 1%, 5%, and 10%, respectively.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.